- Domestic flats strengthen on rising nickel prices

- Indonesian NPI prices rise on supply curbs

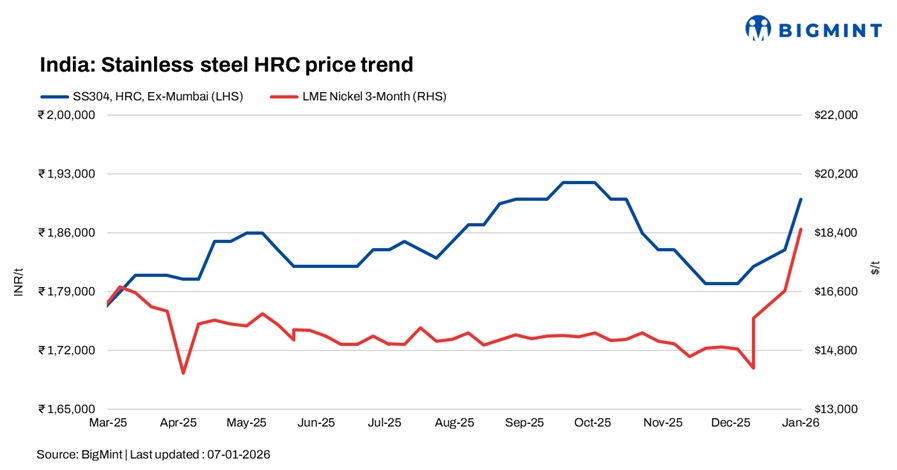

India’s stainless steel market remained firm across both flats and longs during the week ended 7 January, supported by sharply higher raw material costs, a stronger dollar, and firm global cues. Rising nickel prices, driven by Indonesian supply-side measures, continued to lift cost pressure across the value chain, prompting mills to revise prices upward.

Finished flats remained firm

The finished flats market remained firm, underpinned by improving domestic demand and elevated international prices. Market participants attributed the upward momentum primarily to higher nickel prices following Indonesia’s production curbs, which tightened supply and pushed up production costs globally and increasing ferro molybdenum prices.

A leading stainless steel coil manufacturer has announced its second price increase in early Jan’26, effective 7 Jan, citing sustained cost-side pressures. The company raised prices of 304-grade coils by INR 4,000/t and 316-grade coils by INR 7,000/t. The revision comes amid elevated nickel prices and improving domestic demand. At the time of reporting, LME nickel prices stood at $18,480/t.

BigMint’s benchmark assessment for 304 HRC stood at INR 190,000/t ex-Mumbai, up INR 6,000/t w-o-w, while 316 HRC stood at INR 336,000/t, up INR 5,000/t w-o-w.

Finished longs gain support from cost pressures

The stainless steel longs market also moved higher during the week, supported by improving sentiment and rising raw material prices. According to mill sources, higher nickel prices and expectations of further cost escalation prompted mills to raise their purchase offers to secure adequate volumes at current market levels.

BigMint’s benchmark assessments for stainless steel 304L (25 to 100 mm) black round bars was INR 158,000/t ex-Mumbai, up by INR 5,000/t. Meanwhile, SS 316L black round bars were at INR 275,000/t ex-Mumbai, up INR 6,000/t over the week.

On the export front, indicative FOB offers for Indian stainless steel longs were heard at $2,050-2,100/t for 304-grade bright bars and $3,550-3,570/t for 316-grade bright bars. European markets largely remained closed due to New Year holidays, resulting in limited fresh enquiries and no major new bookings. Mills were primarily focused on executing and clearing previously committed export orders during the period.

Chinese stainless steel and NPI prices

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,400/t ($1,916/t) exw, while FOB tags of 304-grade CRCs were firm at $1,920/t. Indonesian FOB prices of nickel pig iron (NPI) (8-12%) were at $120/t and NPI (10-14%) stood at $121/t.

Raw material market overview

Ferro Molybdenum: Indian ferro molybdenum prices rose by INR 165,000/t ($1,834/t), about 6%, w-o-w to INR 2,890,000/t ($32,126/t) exw as of 7 January, according to BigMint’s assessment. The prices are hovering at two-month high as such levels were seen in early Nov’25. The increase was driven by a rise in global market trends, particularly in China, along with higher molybdenum oxide prices and stronger LME molybdenum futures.

Ferro chrome: Indian high-carbon ferro chrome (HC60%) prices remained steady at INR 106,000/t ($1,181/t) exw-Jajpur.

Ferro silicon: Indian ferro silicon (70%) prices witnessed a decline of INR 2,500/t ($28/t) as compared to the assessment on 29 Dec’25. Prices fell post Bhutan’s announcement of January 2026 offers, which stood at INR 94,000/t ($1,043/t) exw.

As per BigMint’s assessment on 5 January, ferro silicon prices in India were INR 94,000/t ($1,043/t) exw Guwahati. Prices have fallen to an over 1-month low as similar levels were last seen in mid-Nov’25.

Ferrous scrap: India’s imported scrap market stayed firm, although buying remained cautious due to year-end holidays and a conservative mill approach. European shredded scrap was offered at $350-355/t CFR, while UK HMS 80:20 was quoted at $325-330/t CFR. Bids, however, stayed $5–10/t lower, limiting deal closures despite steady inflows of mixed scrap grades. Australian HMS 80:20 was heard at $318–320/t CFR. Market sentiment improved slightly on better steel demand cues, though containerised trade activity remained limited.

Outlook

India’s stainless steel market is expected to remain firm in the near term, supported by elevated nickel prices, strong global cues, and sustained cost-side pressures. Flat products are likely to retain upward bias as mills continue to pass on higher raw material costs. Overall, volatility in nickel prices and developments around Indonesian supply policies will remain key market drivers in the coming weeks.

Leave a Reply