- Imports of SS flats edge up by 2% y-o-y in H1CY’25

- Indonesia top supplier of flats, China’s share falls sharply

- SS scrap imports surge 40% in H1 as arrivals of semis drop

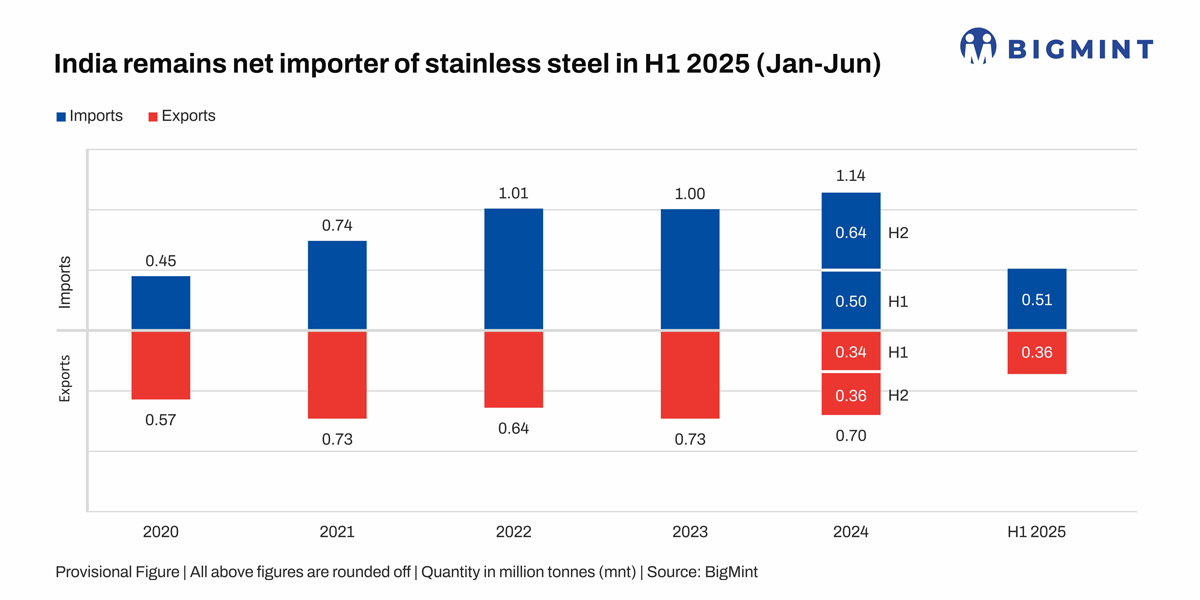

Morning Brief: India’s imports of finished stainless steel edged up in the first half of calendar year 2025, totaling 515,157 tonnes (t), a slight 1% rise from 507,942 t in H1CY’24. Flat product imports increased 2% y-o-y to 501,472 t, while inflows of long products slipped 9% to 13,685 t, as per latest BigMint data.

The growth in flats imports was supported by strong demand from infrastructure, urbanisation, and manufacturing, along with competitive supplies from ASEAN nations leveraging Free Trade Agreements (FTAs). Lower duties, pricing advantages, and strategic trade ties have boosted ASEAN’s share, challenging domestic producers despite India’s significant stainless steel capacity.

Despite annual stainless steel production of 3.7 million tonnes (mnt), India remains a net importer, with demand surpassing supply. India’s apparent stainless steel consumption jumped 35% y-o-y to 2.21 mnt in H1CY’25 compared to 1.64 million tonnes in H1CY’24.

India’s stainless steel production grew by 26% in H1 to 2.06 mnt, up from 1.63 mnt in H1CY’24. Production of finished flats and longs increased by 24% and 28% y-o-y, respectively. This boost in domestic output also increased the need for imported scrap.

Stainless steel exports down 2% in H1CY’25

India’s stainless steel exports were recorded at 353,800 t in H1, including finished longs at 218,000 t, down slightly by 1% against H1CY’24, while finished flat exports stood at 135,900 t, down 4% against 141,500 t in same period last year.

Impact of Trump’s tariffs on stainless steel industry

In 2025, Trump’s tariffs on steel and aluminum reshaped global trade, indirectly pressuring India’s stainless steel sector. Though India’s direct exposure to the US market was limited, the tariffs disrupted supply chains and intensified regional competition. Strong domestic demand, the government’s infrastructure push, and GST reforms helped provide resilience against global tariff-driven challenges.

Reaction to rising imports

Local producers have urged the Directorate General of Trade Remedies (DGTR) to impose anti-dumping measures on cheaper imports from China, Vietnam, and Indonesia, citing risks to domestic competitiveness and the need for policy support to safeguard India’s expanding stainless steel market.

Product-wise imports

Flats imports in H1CY’25 reached 501,500 t, with 300-series contributing 50% (216,300 t), followed by 400-series at 25% (99,500 t), and 200-series at ~3%. Long product imports stood at 13,700 t, where 300-series dominated with 45% (6,300 t) and 400-series contributed 13%.

Country-wise imports

Indonesia was the top supplier of stainless steel flats, shipping 130,900 t to India in H1—an 849% spike from 13,787 t last year. In contrast, China’s shipments fell 54% y-o-y to 99,775 t. Vietnam recorded shipments at 74,342 t, up 25%. South Korean imports stood at 58,892 t, up 61%, and both of these countries expanded their share in India’s imports.

In the longs segment, Taiwan supplied 3,598 t (down 21%), while South Korean imports increased 53% to 1,662 t. Shipments from China dropped 55% to 1,703 t, underscoring shifting dynamics in the segment.

Stainless scrap imports surge

India’s stainless scrap imports climbed 40% y-o-y to 729,500 t in H1 from 519,800 t in H1CY’24. 300-series led with 520,000 t (up 53%), while200-series rose 10% to 56,000 t and 400-series inched up 5% to 94,800 t.

This sharp rise in scrap imports coincided with a decline in arrivals of semi-finished products like slabs and billets, prompting greater use of scrap to support production. Notably, Indonesia, a key supplier, saw its exports of semi-finished products and ferro nickel to India decline during this period.

Outlook

Imports are likely to stay elevated in H2CY’25 amid robust infrastructure-led demand. However, new domestic capacities and potential trade safeguards—particularly against ASEAN inflows-could gradually recalibrate India’s stainless steel import profile, reducing its reliance on overseas supply over the medium term.

Leave a Reply