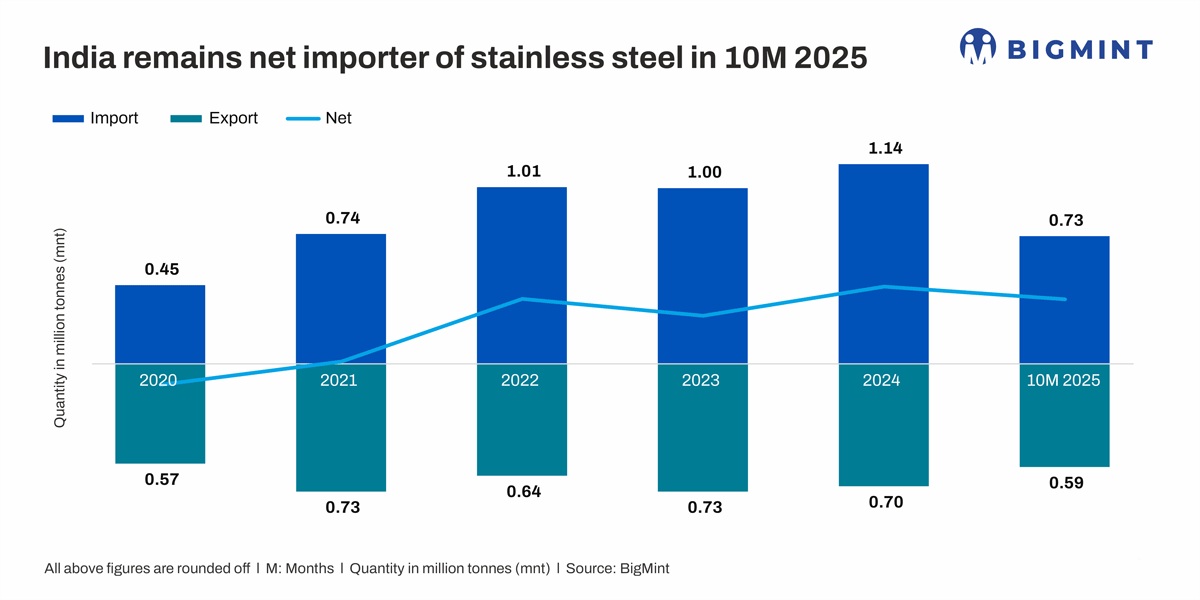

- Total exports edge down to 0.73 mnt against 0.93 mnt in 10MCY’24

- China sees unprecedented plunge in exports of stainless steel flats

- Domestic stainless steel production rises 8% in Jan-Oct, flats up 6%

Morning Brief: India’s stainless steel imports saw a noticeable contraction during 10MCY’25 (January-October 2025) driven primarily by a steep decline in arrivals from China, improving domestic stainless steel production, and cautious procurement amid volatile raw material prices

Total stainless steel imports were 0.73 million tonnes (mnt), down 21% from 0.93 mnt in 10MCY’24. Around 0.72 mnt were stainless steel finished flats, imports of which fell by 22% from 0.90 mnt in 10MCY’24, while inflows of long products were recorded at 23,300 t, down 16% from last year’s 27,600 t

Series-wise imports

300-series flats imports grew 14% y-o-y to 0.33 mnt from 0.29 during the review period last year supported by steady demand from process industries and high-end applications. In contrast, 400-series imports fell sharply by 29% y-o-y to 0.17 mnt. 200-series flats remained relatively stable with a mild 3% decline at 20,000 t, while other grades corrected significantly due to shifts in sourcing patterns and reduced import dependency.

Series-wise, 300-series longs dropped 3%, reflecting sluggish activity in fabrication and engineering. 400-series longs showed a modest 7% increase, driven by consistent auto-component and appliance demand. The 200-series declined 7%, while other specialty grades fell 36%.

China’s collapse reshapes India’s import mix

China—traditionally India’s dominant stainless steel supplier-recorded an unprecedented ~70% y-o-y collapse in flat product shipments, plunging to 0.16 mnt from 0.52 mnt last year. This single trend accounted for the majority of the decline in total imports. In contrast, Vietnam, South Korea, and Thailand expanded their supplies, filling part of the gap left by China. Indonesia and Japan held stable positions with marginal variations.

Long products mirrored this trend: Chinese imports fell 62%, with Taiwan, Germany, and Italy also registering declines. However, South Korea’s shipments more than doubled to 3,900 t, and Japan posted slight gains—indicating selective demand for precision-engineered long products rather than bulk commodity imports.

Why are imports declining? Three-pronged shift

1. Domestic production rises to record levels

India’s stainless steel production increased 8% y-o-y to 3.20 mnt in 10MCY’25. Flats production stood at 2.19 mnt (+6%), while longs surged to 1.0 mnt (+25%). Expanding capacities, better mill utilisation, and efficiency gains allowed domestic players to capture demand previously met via imports, especially in commodity grades.

2. China’s export slowdown

The collapse in Chinese shipments-driven by shifting export priorities, weaker price competitiveness, and compliance concerns-was the biggest single factor. With Chinese mills facing domestic uncertainties and tighter scrutiny abroad, the flow of low-priced stainless steel into India weakened considerably.

3. BIS compliance alters sourcing behaviour

The rollout of BIS certification requirements reshaped procurement strategies. Although the government temporarily relaxed compliance under IS 6911, IS 5522 and IS 15997 until 31 December, importers still faced documentation challenges, higher risk perception, and added lead-time uncertainty. This pushed many buyers to prioritise domestic suppliers who offered predictable timelines and assured quality.

Imported 304 HRC (3-25 mm) is landing at INR 175,000-180,000/t ($1,900-2,000/t), making it nearly INR 5,000-10,000/t cheaper than domestic prices. BigMint’s latest assessment places domestic 304 HRC at INR 180,000-184,000/t on 18 November. Following the temporary BIS announcement, the market-particularly the 300 series-has seen a sharp correction and selling pressure has increased.

Outlook

India’s stainless steel imports are expected to stay moderate over the coming months, even with the temporary BIS relaxation effective until 31 December. Most buyers are taking a cautious stance as they wait for clarity on QCO enforcement in 2026 and assess how many overseas mills will ultimately secure BIS approval.

Domestic mills are operating at improved utilisation levels and offering competitive pricing, which is likely to continue substituting imports, especially in commodity-grade 200 and 400 series. With Chinese exports slowing and domestic supply remaining steady, India’s import dependence is expected to stay low.

A potential uptick in imports may only materialise once BIS norms for 2026 are finalised, global raw material prices stabilise, and export flows from China and ASEAN become more predictable. Until then, domestic sourcing will continue to dominate India’s stainless steel market.

Leave a Reply