- Robust availability keeps prices on leash

- Basmati swings sharply, recovers in Sept’25

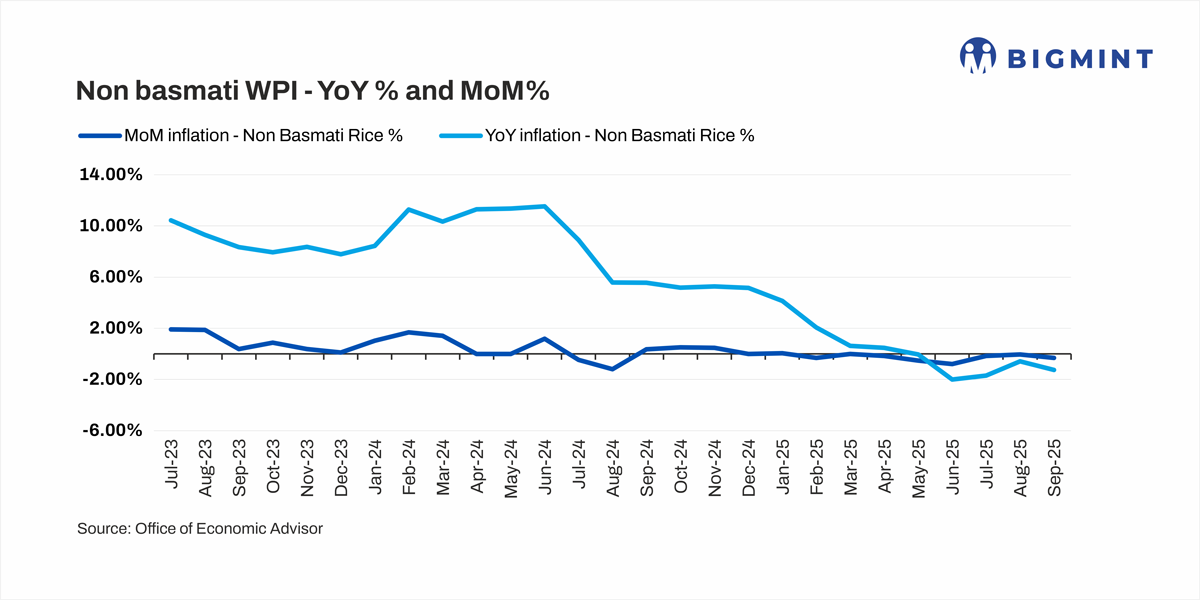

While volatility is a sustained feature in rice prices in India, data available with BigMint reveals these have been trending lower since the middle of 2024.

The y-o-y inflation rate for non-basmati rice indicates, it started high at over 10% in July 2023, remained consistently robust at above 8% till March 2024. It peaked at around 11.5% between May-July 2024, followed by a sharp and sustained deceleration, with y-o-y inflation dropping significantly to less than 6% by September 2024. The downtrend continued into 2025, crossing the 0.0% mark around June 2025, and eventually entering negative territory by September 2025, settling at approximately -1%. This indicates that by the end of the period, non-basmati prices were lower than they were a year earlier.

Basmati was more volatile. The y-o-y inflation rate shows a period of high annual price growth at around 8% in July 2023, peaking slightly above 10% in November 2023, and then experiencing a steady decline to 5-6% through the first half of 2024 before a steep drop. Y-o-y inflation turned negative (deflation) around November 2024, hitting its lowest point at approximately -7.50% in January 2025. This indicates basmati prices were significantly lower than a year earlier. However, prices recovered rapidly, crossing back into positive territory by July 2025 and ending at around 4% in September 2025 but way lower than 2023’s peaks.

Thus, the overall strong annual inflationary surge seen in 2023-2024 completely reversed by late 2025, leading to price deflation compared to the previous year.

Factors behind decreasing prices

Adequate supplies pressure down prices: By the middle of 2025, broad WPI food inflation slowed down, and headline WPI moved towards a slight deflation as large domestic supplies (large stocks) and lower cereal prices eased wholesale pressures. Basmati and non-basmati have small direct WPI weights, so their recent relative softening helped slow food inflation. Earlier, prices of paddy and rice rose in 2023-24 and into late 2024 mainly boosted by weather concerns. The monsoons were erratic leading to a combination of drought and excess rainfall which caused some food sub-indices to rise. From middle-to late-2024, wholesale prices of basmati peaked because some premium export grades were hard to find. This led to strong demand for certain grades (especially basmati), and an overall strong procurement trend.

Higher buffer stocks: India’s rice buffer stocks averaged a record high in the period January-June, 2025 or H1CY’25, reveals data maintained with BigMint. Data tracked since 2022 shows buffer stocks of rice held by the Food Corporation of India (FCI), the nodal government agency for procuring and distributing foodgrains and other crops, in H1CY’25 averaged 370 lakh tonnes (LT) against 291 LT in the same period in CY’24, 235 LT in H1CY’23 and 310 LT in H1CY’22. The higher stocks are a result of increased paddy procurement by the government from farmers and offer a narrative of higher supplies.

Lifting of non-basmati export curb: From mid-2024, the export policy for non-basmati rice was freed from the prohibited clause clamped in July 2023. This ban had been necessary to stabilise prices of non-basmati and also boost domestic supplies. As domestic production improved due to a comfortable supply trend within the country, these restrictions were progressively relaxed till March 2025 which eased prices too.

Outlook

India’s domestic balance sheet for rice in 2025-26 shows a market in surplus, with robust availability, strong but manageable usage, and high carry-out stocks. All these factors will not only affect policy and market dynamics but prices too, in the medium term.

Leave a Reply