- Pig iron exports jump 115% y-o-y in FY’26

- Imports decline 43% amid improved domestic supply balance

- India emerges as competitive supplier in US pig iron market

India’s pig iron market staged a strong recovery in FY’26 after prolonged weakness witnessed over the previous few financial years, supported by improving export opportunities, tighter imports, elevated raw material costs and stronger overseas competitiveness. Domestic steel-grade pig iron prices in Durgapur averaged around INR 37,800/t in FY’26 against nearly INR 35,900/t in FY’25, supported by better export-linked demand and firmer production costs.

The market remained largely volatile through the year, with prices touching multi-month highs during Q4FY’26 amid export-led tightness, higher met coke costs and improved buying sentiment. The resurgence in overseas demand, particularly from the US and Türkiye markets, provided crucial support to Indian pig iron producers after exports had remained under pressure for the past few years.

BigMint analyses how India’s pig iron market performed in FY’26 compared with FY’25 and the key factors driving the turnaround.

Why did pig iron market conditions improve in FY’26?

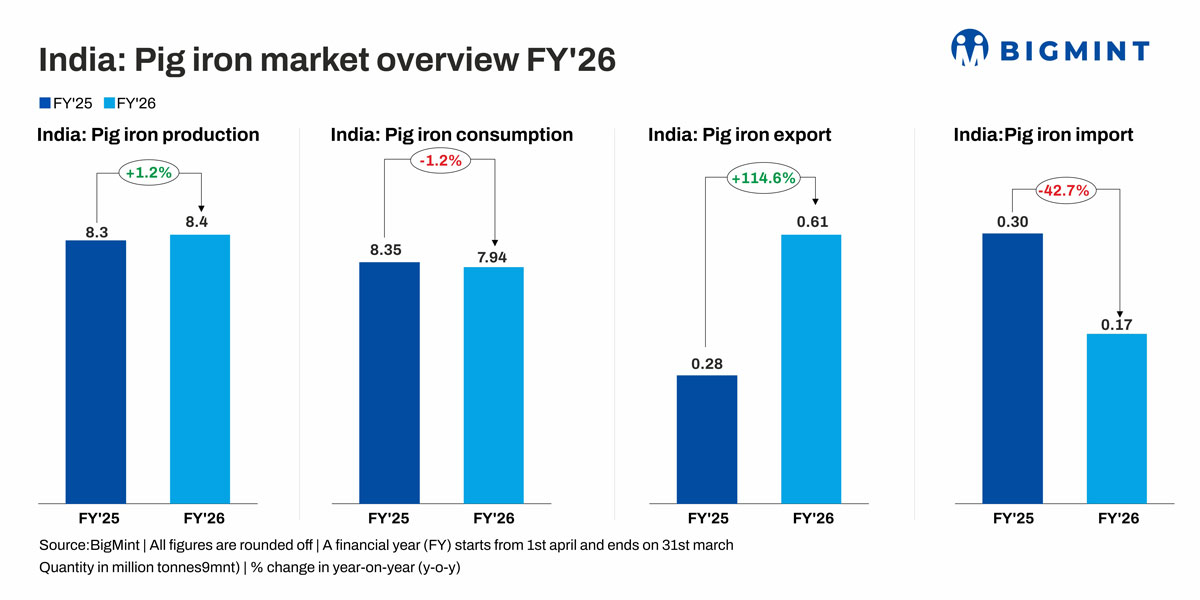

Exports rebound sharply after prolonged weakness: India’s pig iron exports increased sharply by nearly 115% y-o-y to around 0.61 mnt in FY’26 compared with 0.28 mnt in FY’25. Stronger overseas demand, improved competitiveness of Indian-origin material and relatively tighter global availability supported exports during the year.

Multiple eastern-region producers concluded sizeable export transactions to the US, Türkiye and Europe. A prominent eastern India-based producer reportedly sold around 65,000 t of steel-grade pig iron to Türkiye, while another leading supplier concluded nearly 55,000 t cargoes to the US market. Export activity remained particularly strong during Q4FY’26, tightening domestic spot availability and supporting prices across eastern India.

India emerges as competitive supplier in US market: India also re-emerged as a competitive supplier in the US pig iron import market amid favourable pricing dynamics and lower tariffs. Market sources reported Indian pig iron offers with 0.15% phosphorus content at around $440-445/t FOB west coast India, translating to nearly $480-485/t CIF New Orleans for 60,000-66,000 t cargoes.

The temporary reduction in US tariffs on Indian imports to a flat 10% significantly improved India’s competitiveness against traditional suppliers such as Brazil and Ukraine. The lower-priced Indian offers increased competitive pressure in the US market, where buyers actively sought alternative supply sources amid elevated pig iron prices and tight global availability.

Imports decline sharply in FY’26: Pig iron imports into India declined significantly by around 43% y-o-y to 0.17 mnt in FY’26 against 0.30 mnt in FY’25. Improved domestic availability, relatively stronger local production and better export-linked demand reduced dependence on imported material.

This marked a reversal from earlier years when imports had steadily increased amid weak domestic competitiveness and lower-priced overseas supplies.

Production remains stable despite market volatility: India’s pig iron production remained largely stable at around 8.35 mnt in FY’26 compared with 8.33 mnt in FY’25, indicating balanced supply conditions. However, capacity utilisation improved during the latter half of the year due to stronger export demand and better producer realisations.

Production growth remained significantly higher compared with FY’21 levels, reflecting continued capacity additions by integrated and merchant pig iron producers across eastern and central India.

Higher met coke prices support domestic pig iron market: Elevated raw material costs also supported pig iron prices through most of FY’26. Merchant met coke prices remained firm amid tighter supply conditions and import-related uncertainties.

The recent imposition of provisional anti-dumping duty on low-ash met coke imports is expected to keep domestic coke prices elevated, thereby sustaining cost support for pig iron producers in the near term. Higher production costs restricted aggressive price corrections despite intermittent weakness in downstream steel demand.

Substitute metallics continue to influence demand: Scrap and sponge iron continued to remain key substitute metallics influencing pig iron consumption patterns. Domestic HMS 80:20 scrap prices remained volatile through FY’26, while sponge iron prices fluctuated amid changing coal costs and finished steel demand.

However, limited scrap availability in several regions restricted aggressive substitution and supported pig iron consumption among induction furnace-based steelmakers and foundries.

Outlook

India’s pig iron market is expected to remain relatively supported in the near term amid stable exports, elevated met coke prices and improving global competitiveness. Export opportunities to the US and Middle East are likely to remain key demand drivers going forward.

However, domestic demand from the secondary steel sector may continue to remain cautious due to pressure in finished steel markets and competition from scrap-based metallics. Overall, pig iron prices are likely to remain range-bound with a firm undertone supported by exports and input cost pressure.

Leave a Reply