- Indonesian shipments rise as prices fall to 4-year lows

- Pre-monsoon restocking keeps South African coal imports high

- Increased pet coke prices stoke interest in thermal coal imports

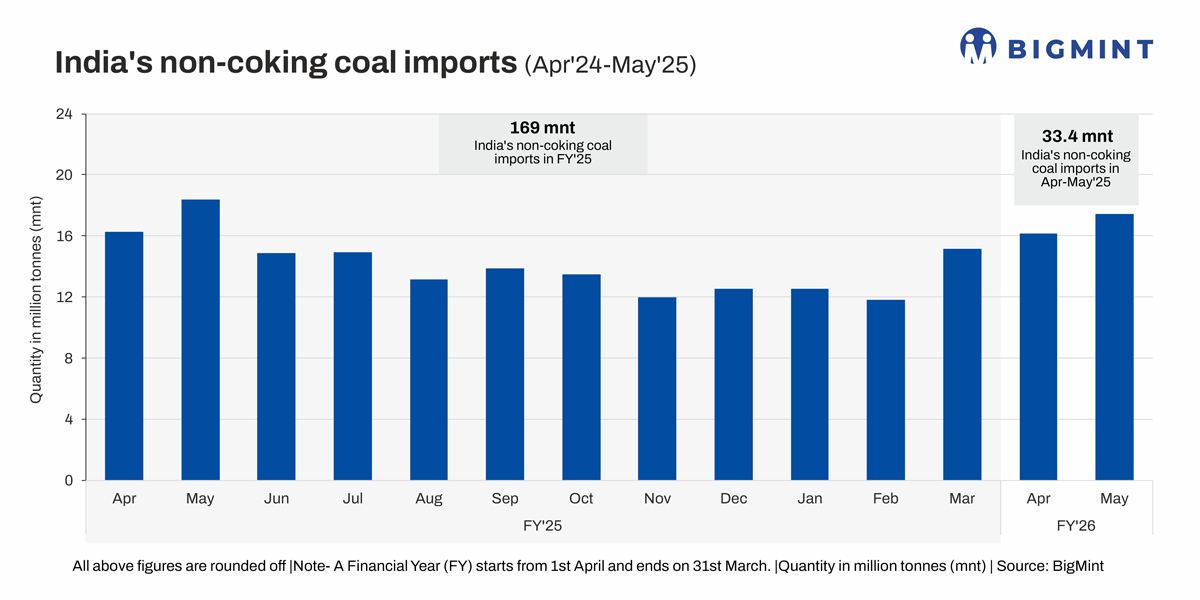

Morning Brief: Imports of non-coking coal into India, used for power generation and for industrial purposes, reached a one-year high in May 2025 of 17.44 million tonnes (mnt), as per BigMint data. Coal imports were a tad lower than 18.38 mnt in May 2024 – lower by over 5% y-o-y. However, shipments surged nearly 10% m-o-m from 15.9 mnt in April.

Indonesia remained the top exporter to India, with shipments rising by 16% m-o-m to 9.8 mnt. After climbing up by 30% m-o-m in April, South African non-coking coal imports continued to trend higher. Imports reached 3.38 mnt in May, up 0.5% m-o-m and over 25% y-o-y.

Notably, coal imports from the US and Russia increased sharply m-o-m to 2.01 mnt and 1.32 mnt, respectively. Imports from both countries surged on a lower base in April.

Among the key ports in the country, Mundra received the highest tonnage in May of 2.51 mnt followed by Krishnapatnam (1.77 mnt). Dhamra port in Odisha, too, witnessed total imports increasing by 140% m-o-m to 1.27 mnt.

Why imports edged up in May’25?

Arrivals from Indonesia increase as prices fall: Indonesian coal imports increased to the highest level since May 2024 as prices became attractive for Asian buyers after apprehensions of price hike due to the government’s HBA policy for coal exports and higher mining royalties in Indonesia subsided somewhat.

BigMint data show that Indonesian 4200 GAR benchmark coal export prices dropped to $42/t FOB Kalimantan on 16 June, down from over $50/t FOB in May. Prices have descended to the lowest levels since April 2021. This boosted exports into India and China at a time of seasonal demand upturn. Prices have been declining fast due to higher domestic coal production in India and China.

South African imports trend higher: Non-coking coal imports from South African kept edging higher in May after increasing by 30% m-o-m in April. In fact, imports in May rose to a five-month high. This reflects increased pre-monsoon restocking by Indian sponge iron mills. This is despite the fact that sponge iron prices in key domestic markets have declined to a four-year low, signalling weak steel market sentiment.

Russian, US shipments surge: Russian and American coal imports into India shot up by 52% and 42% m-o-m, respectively, in May. It’s also worth noting that India’s imports of Russian thermal coal reached a two-year high in May, as they had not been above the 1 mnt per month level since June 2023.

This shows that Russian coal in the Pacific has once again become cost-competitive compared to Newcastle coal – the Asian benchmark.

Additionally, American and Saudi pet coke prices surged in the February-April period due to rising demand for pre-baked anodes after the Chinese New Year holidays, tight supplies and declining freights. This prodded domestic cement producers to source thermal coal instead of pet coke, thereby contributing to higher coal imports from the US and Russia.

Outlook

Softening demand for coal-based generation due to the early arrival of monsoon, high coal port stocks and rising domestic coal production have collectively put a brake on non-coking coal imports. This is the reason why import volumes have been lower y-o-y even in the middle of the summer season in India. Higher domestic coal production and the increasing share of renewables are likely to keep weighing on coal imports going forward.

However, pet coke prices may surge due to the uptick in crude oil prices following the Israel-Iran war. This may keep domestic cement manufacturers interested in thermal coal imports for some time.

Leave a Reply