- Domestic coal production up 6% in Apr-Feb of FY’25, as per Coal Ministry

- Govt’s blending mandate ceases in Feb, higher sales seen in CIL e-auctions

- Indonesia’s move to link coal export prices to domestic index may impact India’s imports

Morning Brief: India’s imports of non-coking coal, used in the power as well as industrial sectors, fell to the lowest level since November 2024 to around 12.2 million tonnes (mnt) in February, a decrease of 3% m-o-m, as per latest BigMint data.

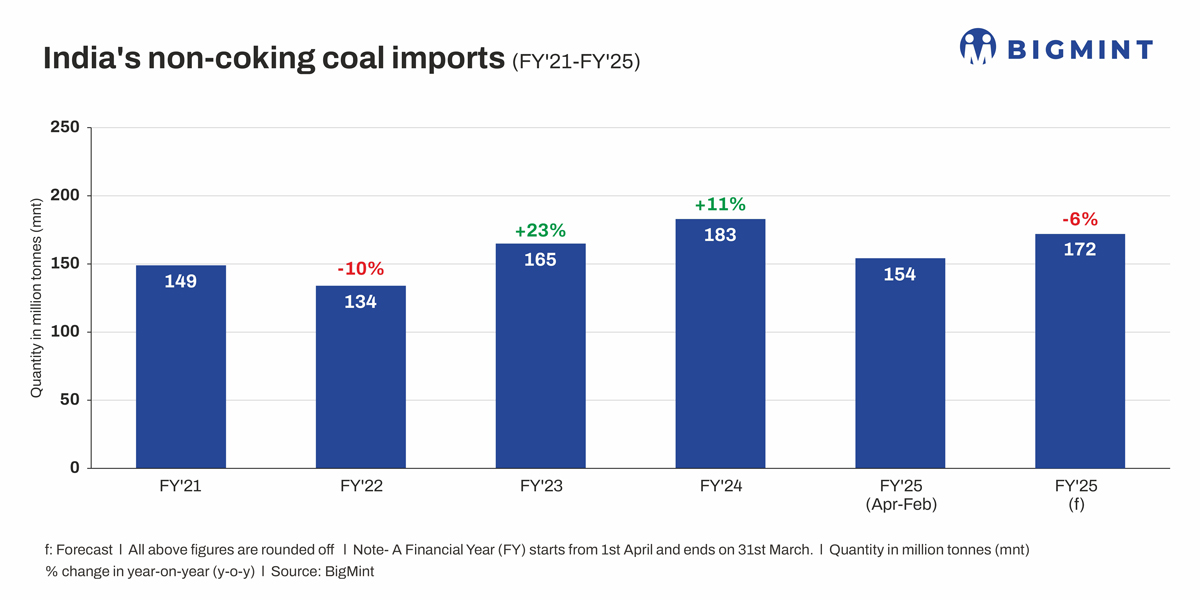

Total imports declined by around 1.3% y-o-y to around 173 mnt in 2024. In FY’24, cumulative imports stood at 183 mnt.

Country-wise shipments

Data shows that imports from Indonesia, the top exporter, decreased by more than 6% m-o-m in February to 6.96 mnt, while South African coal shipments fell even more sharply by 30% m-o-m to 2.4 mnt, the lowest in the last six months.

Indonesian coal imports to India in FY’24 were assessed at around 112 mnt, and its share in India’s non-coking coal exports stood at around 62%.

Even as coal imports from the US increased in February to nearly 1 mnt, Russian shipments recorded a decline of 19% m-o-m.

Factors impacting coal imports

*Growth in domestic coal production: At over 74 mnt in February, CIL’s coal production remained quite strong, although witnessing a marginal decline compared with January. Q4 of a fiscal year usually sees higher coal production as miners ratchet up operations to meet fiscal targets.

According to the Union Coal Ministry, cumulative coal production has reached 928.95 mnt in April-February of the ongoing fiscal, reflecting a 5.73% increase compared to 878.55 mnt in the same period last year. Likewise, coal dispatches have risen to 929.41 mnt, marking a 5.5% growth from 880.92 mnt in the previous year.

Coal production is expected to rise by 6.5% in FY’25, albeit moderating a bit vis-a-vis the over 11% y-o-y growth in FY’24. Higher production and dispatches have directly contributed to minimizing the reliance on imports.

*Higher domestic coal availability: Data shows that CIL’s coal dispatches stood at around 63 mnt in February, dropping slightly from January, but sales at auctions by CIL’s subsidiaries edged up in February, thereby increasing domestic coal availability. For instance, SECL auctions witnessed total sales at around 2.2 mnt in February compared to 1.9 mnt in January. Similarly, sales at auctions by ECL increased to over 0.4 mnt in February from around 0.2 mnt in January.

In CY’24, CIL reduced the Earnest Money Deposit (EMD) for its e-auctions from INR 500/t to INR 150/t. This aimed at boosting participation and competitiveness, as e-auction premiums dropped significantly from 252% in FY’23 to 29% in FY’25.

*Higher stocks at TPPs: As per data from the Central Electricity Authority (CEA), coal stocks at domestic thermal power plants (TPPs) stood at a multi-year high of nearly 56 mnt, as on 16 March. This is even higher than 47-48 mnt at the end of January and is expected to last for 19 days at a plant load factor (PLF) of 85%. Only five, i.e. one-third, of the 15-odd imported coal-based plants in the country have a critical stock situation, as per the CEA. Therefore, dependence on imports has decreased.

*Drop in share of imported coal for blending: Notably, the government’s mandate on imported coal blending for power plants ended in February. The mandate has been revised several times since 2020. Also, Coal Ministry data reveal that, as of January, the share of imported coal for blending in power plants fell by 23.56% y-o-y.

*Rising share of renewables-based generation: Source-wise power generation data reveals that total generation from solar, wind, biomass coupled with storage technologies grew around 12% y-o-y up to February of the current fiscal, while large hydropower generation increased by over 10%. At the same time, thermal generation edged up by just 2.6% y-o-y during the period. The growth in renewables weighed on coal demand, especially amid a 4% decline in power demand in February.

*Decline in sponge iron production: South African coal exports to India dropped sharply by 30% m-o-m due largely to the decline in domestic sponge iron production in February. As per provisional data with BigMint, the country’s sponge iron production fell by over 6% m-o-m to 4.5 mnt in February, which impacted demand for South African coal. As shipments had been strong in December and January, higher stocks also weighed on import demand.

Outlook

BigMint projects non-coking coal imports to fall to 172 mnt in the current fiscal from 183 mnt recorded in FY’24. Indonesia will emerge as the top coal exporter to India in FY’25, although total shipments are estimated to shrink by over 4% y-o-y to around 107 mnt from 112 mnt in FY’24.

The Indonesian government’s move to link coal export prices with the domestic HBA index is likely to lead to reduced interest for Indonesian coal, especially among Chinese and Indian buyers who favour Indonesia due to lower coal prices. The move, effective from March, will trigger a spate of re-negotiations of existing contracts, with the HBA replacing the ICI. This may impede coal imports from Indonesia, especially because Indian buyers can fall back on higher domestic stocks.

On the domestic front, Q1FY’26 may witness higher coal imports due to the surge in midsummer demand. The Coal Ministry is committed to fulfilling the FY’26 coal demand of over 906 mnt from the power sector, and peak demand is expected to reach 270 GW in FY’26. However, domestic production is slated to reach over 992 mnt in FY’25, and sufficient stocks at coal-fired plants may keep import demand rangebound.

Leave a Reply