- Indonesian exports to India down 10% y-o-y in 10MCY’25

- Thermal power generations drops 3.5% y-o-y in Jan-Oct

- Import sentiment soft despite 9% drop in coal production in Oct

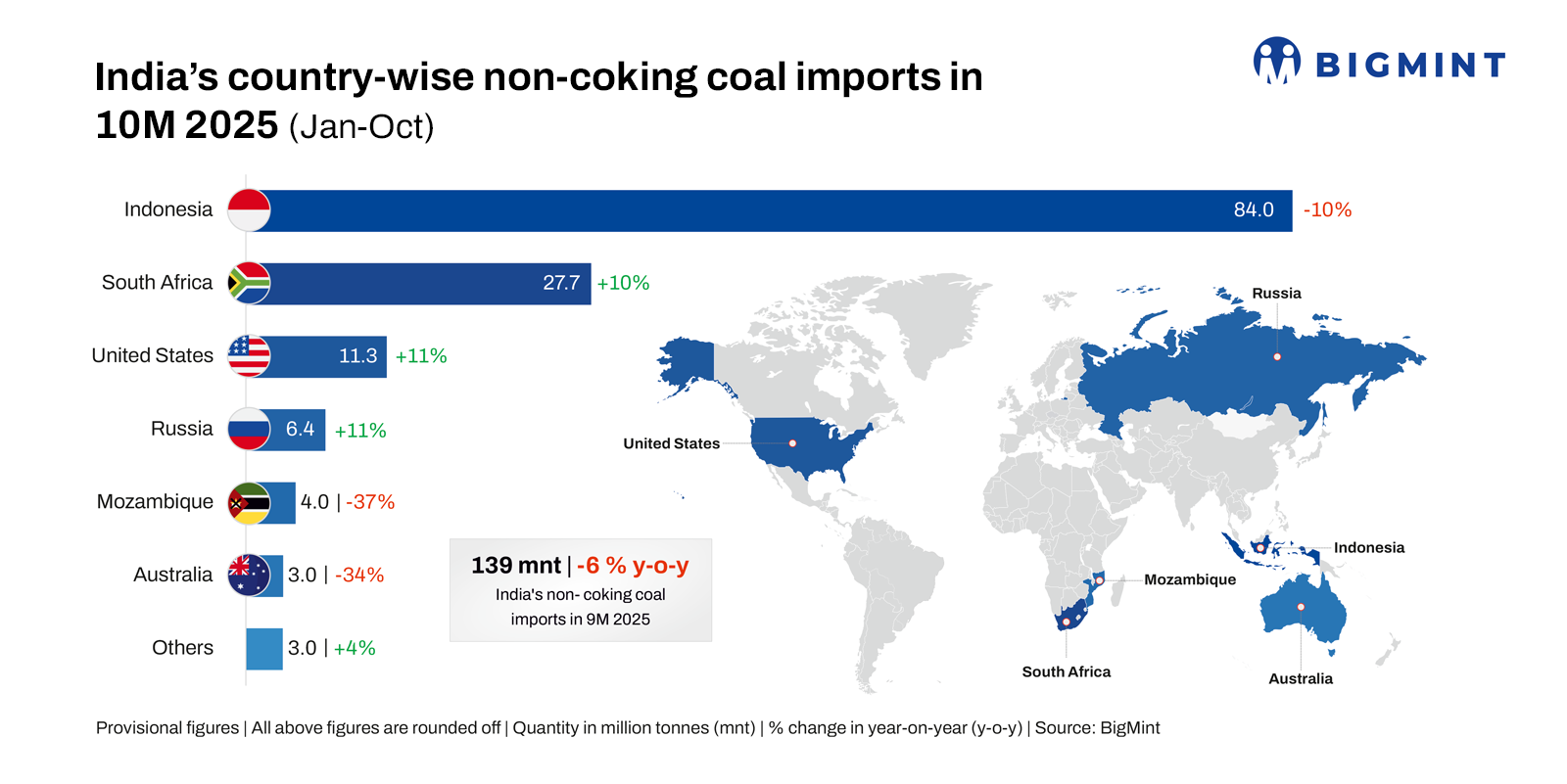

Morning Brief: India’s imports of non-coking coal, used in the power and industrial sectors, decreased from 149 million tonnes (mnt) in January-October 2024 (10MCY’24) to 139 mnt in the same period of the current year, a decrease of around 6% y-o-y, as per latest data with BigMint.

Country-wise imports

Imports in October dropped nearly 7% m-o-m despite the slump in domestic production due to unseasonal rains and cool weather. So, imports from Indonesia, mainly coal used for power production fell by 4%, while shipments from South Africa rose 4% on steady demand from the steel sector. Imports from Russia and the US, too, declined.

Coal arrivals at all the key ports showed a sharp de-growth m-o-m in October. Total unloaded volumes at Mundra and Vizag ports shrunk 45-50% m-o-m while Krishnapatnam witnessed a 23% drop.

Key trends in thermal coal import market

Lower thermal power generation: Data shows that thermal power generation fell by 3.5% y-o-y during the review period due largely to an above-average and long-extending monsoon, cooler weather and the reduced demand for cooling. This is reflected in the meagre 1% rise in power demand during the period despite GDP growth of over 6.5%. The change in weather conditions had a direct impact on imports of thermal coal, especially from Indonesia. Shipments from our Asian neighbour dropped 10% y-o-y in 10MCY’25.

10% spurt in South African imports: The 10% rise in imports from South Africa can be attributed to steady demand from the domestic sponge iron sector. India’s sponge iron production is expected to exceed 55-56 mnt in 2025 despite the steel market downturn. Therefore, imports of high FC and low VM coal from South Africa remained high.

Surge in renewable power generation: Data shows that solar- and wind-based generation (including biofuels and storage) witnessed a 22% growth y-o-y in 10MCY’25. Plentiful rainfall and an extended monsoon led to a 14% surge in hydropower output. It bears recall that India has achieved its target of 50% share for RES in total capacity five years ahead of deadline. However, grid integration and storage infrastructure gaps continue to reinforce the traditional reliance on thermal power.

Outlook

India’s coal production fell by 9% y-o-y in October on weak demand and monsoon impact, with Coal India witnessing a 3% m-o-m drop in output. Nevertheless, imports have declined throughout FY’26 mainly due to favourable weather patterns.

Going forward, with the expected surge in post-monsoon domestic coal mining and, of course, the rush before the fiscal year-end to achieve targets may result in increased domestic production and allocation at CIL auctions, thereby increasing availability across sectors.

However, the massive impact of weather patterns on domestic production and mining infrastructure shows that even slight variations in dispatches and supply shortfalls may trigger panic and compel consumers to resort to imports.

Leave a Reply