- Sep volumes recover to over 14 mnt after 2.5 year low in Aug

- Indonesian coal imports drop 10% y-o-y in Apr-Sep’25

- Surge in renewable generation far outpaces power demand growth

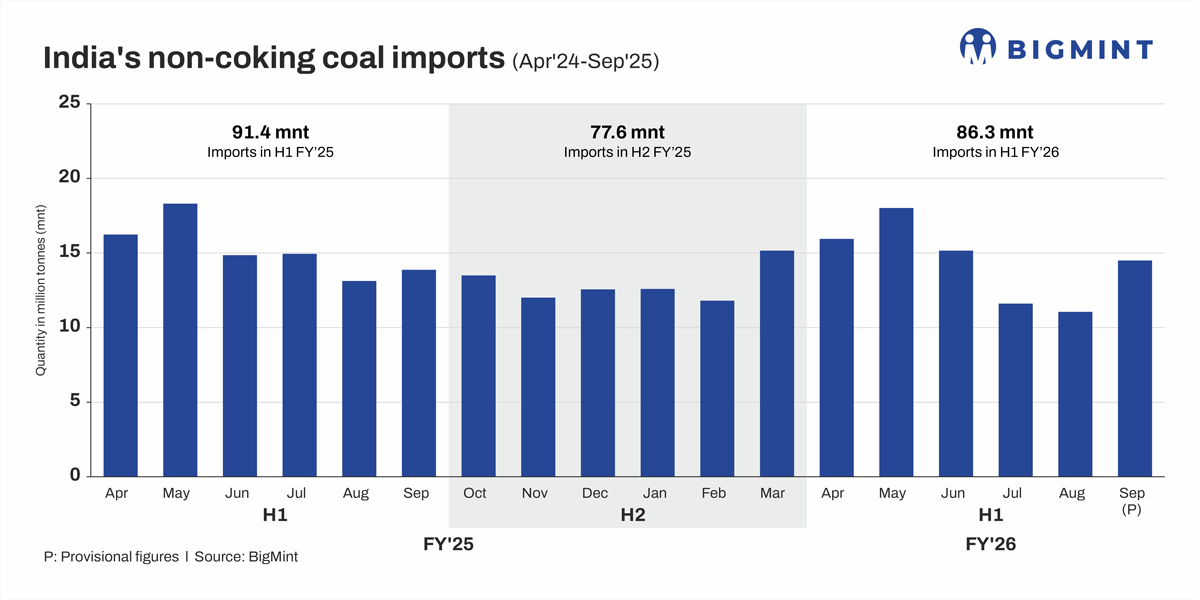

Morning Brief: India’s imports of non-coking coal, used in the power and industrial sectors, decreased from over 91million tonnes (mnt) in April-September 2024 (H1FY’25) to 86.3 mnt in the same period of the current fiscal, a decrease of around 6% y-o-y, as per latest data with BigMint. Non-coking coal imports in FY’25 were around 169 mnt.

However, import shipments in September recovered to reach 14.5 mnt after hitting a 2.5-year low of 11 mnt in August. This was primarily due to a certain recovery in industrial activity ahead of the festive season and fast depletion of stocks at coal-based power plants.

Key suppliers, buyers

The major suppliers to India were Indonesia with 50.8 mnt in H1FY’26, a decrease of 10% y-o-y, followed by South Africa (16.3 mnt) and the US (8 mnt). Notably, South African exports to India increased sharply, by 95% m-o-m, in September from August levels indicating renewed buying interest from the steel industry. This contributed to raising overall volumes.

The main importers were Adani Enterprises (12 mnt), Adani Power (7 mnt), Agrawal Coal (5.2 mnt) and Tata Power (5 mnt).

Why did non-coking coal imports drop in H1FY’26?

Lower thermal power generation: Data from Power Foundation of India shows that coal- and lignite-based generation was around 610 billion units (BU) in FY’26, 68% of total generation, as assessed on 22 September last. Notably, coal’s share was 74% in FY’25. In September, as in previous months, coal-powered generation shows a decrease m-o-m.

The lower share of coal-fired generation in FY’26 has been due to a cooler summer and absence of extensive heatwaves, a heavy and extended monsoon in several parts of the country which drastically lowered the demand for cooling, as well as the surge in renewable power generation. Therefore, apart from the routine imports for the imported coal-based plants, demand has been restrained.

Increase in domestic supplies: India’s coal production in the April-August period of the current fiscal reached over 361 mnt, higher by 0.7% y-o-y. Despite the 4% drop in CIL’s production in H1FY’26 (about 10-11 mnt) total output increased as new mines have entered operations. Reforms in CIL e-auction policies and higher offered volumes in auctions have boosted domestic coal availability both at power stations and for the non-regulated sector.

Coal stocks at power plants were around 57-58 mnt, or sufficient for over 20 days’ consumption, for the better part of FY’26. But stocks dropped below 50 mnt in September, and were assessed as enough for 15 days of consumption, which explains the m-o-m surge in coal imports last month.

Surge in renewable power generation: While India’s power demand increased by just 1.4% y-o-y in H1 and coal-fired generation in H1CY’25 fell by over 3% in January-June, generation from solar and wind saw record surges during that period. Because total power demand addition was far outpaced by renewable capacity addition the demand for imports was substantially reduced.

Solar generation rose by a record of 17 TWh (+25%) compared to 8 TWh (+13%) in the same period of last year, according to a study by Ember. This growth lifted its share in the electricity mix to 9.2%, up from 7.4% in H1CY’24.

Wind generation also increased strongly, by a record addition of 11 TWh (+29%), against just 0.5 TWh (+1.3%) last year. In fact, data shows that wind’s share in total electricity generation during the monsoon months of June, July and August was 6-7%.

Outlook

CIL has set a supply target of over 900 mnt in FY’26, which is 18% higher y-o-y. The projected demand from the power sector is estimated at over 668 mnt this fiscal. Domestic coal production growth at just 0.7% y-o-y in H1FY’26 may have led to shrinking stocks at power plants. However, post-monsoon, production is expected to witness a surge.

CIL is also seeking to cater to the steel and other non-regulated sectors through e-auctions. However, CIL subsidiary SECL’s recent notification on making financial coverage (FC) mandatory for all buyers (e-auction, FSA, MoU) to ensure coal quality upgradation and rectify the old problem of grade slippage may initially lead to further compliance, as well as financial and procedural complications for buyers. But this will ultimately result in quality upgradation and substitution of imports.

In conclusion it can said that if a tempered manufacturing momentum continues during and after the festive season, with power demand remaining largely flat, demand for imported coal, apart from routine purchases, is expected to remain subdued in the coming months.

Leave a Reply