- Imports fall by 14% m-o-m in June to around 15.5 mnt

- Shipments from Indonesia down 12% y-o-y in H1CY’25

- Imported coal demand for DRI production surges y-o-y

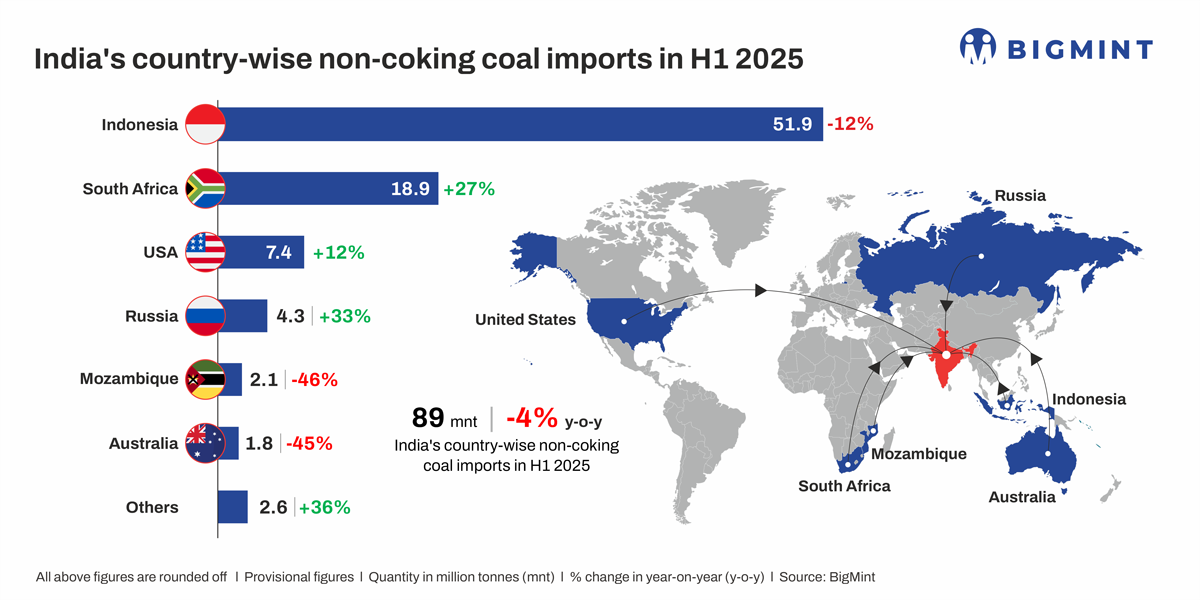

Morning Brief: India’s imports of non-coking coal, used in power production and industrial applications, reached 89 million tonnes (mnt) in January-June 2025 (H1CY’25) compared with 93 mnt in the corresponding period of last year, a decrease of over 4% y-o-y, as per provisional data available with BigMint.

Notably, imports dropped sharply by 14% m-o-m in June to around 15.52 mnt from 18.5 mnt in May. Total non-coking coal purchased by India from overseas suppliers in CY’24 stood at over 173 mnt, a marginal decrease of 1.16% y-o-y.

Top importers

The Indian company that topped the importers list in H1CY’25 was Adani Power with 10.14 mnt compared with 11.8 mnt in the year-ago period, while Adani Enterprise clocked total imports at 10.12 mnt this year compared with 13.8 mnt in H1CY’24.

Tata Power imported 6.47 mnt versus 6.2 mnt in H1CY’24, while Agarwal Coal registered 4.82 mnt of imports compared with 5.2 mnt in H1CY’24, as per provisional data.

Country-wise imports

Imports from Indonesia drop 12%: Imports from the world’s largest non-coking coal exporter, Indonesia, dropped from 59 mnt last year to 52 mnt in H1CY’25 on higher domestic thermal coal production. Russian and US imports also increased in H1CY’25.

South African coal imports up 27%: Volumes from South Africa increased sharply to 19 mnt in H1, up 27% y-o-y. India’s sponge iron sector which consumes South African coal increased imports due to higher consumption. Sponge iron production edged up by 10% y-o-y in January-June this year to nearly 30 mnt.

Interestingly, India’s non-coking coal import demand is waning from the power sector due to government measures to enhance domestic production and dispatch. But demand for imported coal of superior grade, and low in ash, is surging from the industrial sectors.

Why did non-coking coal imports edge down?

Cooler summer: India’s otherwise gruelling summer was this year interspersed with bursts of cyclonic thundershowers and cooler spells which prevented demand from peaking. The early onset of monsoon in different parts of the country also played a role in minimising coal burn. Interestingly, although overall power generation increased during the review period, coal consumption in power generation fell from 695 BU in H1CY’24 to 673 BU. Coal fired power output fell to the lowest level in five years in May.

Increased domestic production: Thermal coal production in India rose from 523.64 mnt in H1CY’24 to 533.46 mnt this year. The government has raised total coal production target for FY’26. The Ministry of Coal has given CIL a production target of 875 mnt in FY’26 against 781 mnt produced in FY’25. However, CIL’s production and dispatches witnessed a marginal de-growth in H1CY’25.

Higher power plant stocks: Total thermal coal stocks at India’s 180-odd power plants were assessed at nearly 59 mnt on 12 July which is sufficient for 20 days of coal burn. Only about five plants were assessed at levels that could be deemed critical. Demand for imports weakened amid higher port stocks and power plant inventory.

Surge in renewables: India has attained 50% share for renewable energy in total capacity – almost five years ahead of target. Power generation through solar, wind, biomass and other non-fossil sources increased by 24% y-o-y in H1CY’25 to 134.6 BU. Another about 100 BU was generated through large hydro and nuclear energy facilities, both of which saw significant growth y-o-y in H1CY’25. Therefore, reliance on coal power lessened.

Outlook

Imports are likely to drop in July as domestic coal auctions conducted by CIL’s subsidiaries have seen sufficient volumes getting booked. Also, imported coal demand will remain soft during monsoon.

Sponge iron prices hit a four-and-a-half-year low in May which resulted in increased blending of domestic coal in rotary kiln-based DRI production in order to minimise costs. Sources informed that some players were blending domestic to imported coal in a ratio of 90:10. Subdued demand for imported cargoes has resulted in stock build up at ports which will discourage fresh imports.

Incidentally, in a recent directive, the government has exempted 79% of domestic power producers from installing costly flue gas desulphurisation (FGD) equipment at power plants to control sulphur emissions. This is expected to minimise the cost burden of the majority of power producers and may result in higher production and lower electricity costs.

Leave a Reply