- Firm import parity supporting domestic coke prices

- Weak pig iron demand capping further price increases

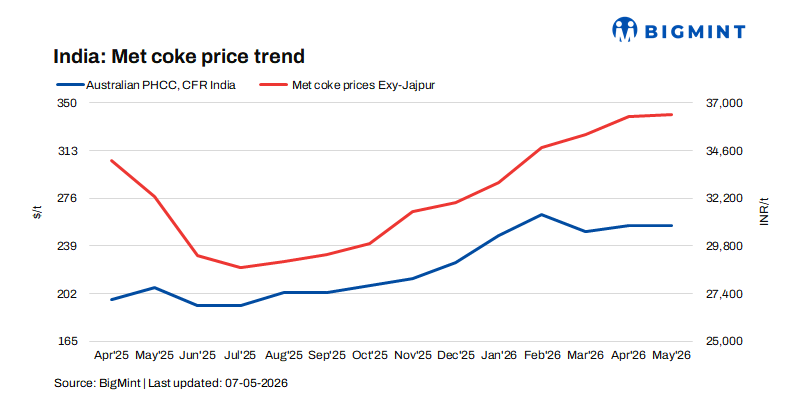

India’s blast furnace (BF)-grade metallurgical coke prices remained largely stable w-o-w as of 7 May 2026, supported by balanced supply-demand dynamics and firm import parity levels.

In the eastern region, BF coke prices were stable at INR 36,400/t ex-Jajpur, while western India witnessed a marginal increase of INR 200/t to INR 33,500/t ex-Gandhidham, reflecting improved replacement costs and firmer imported offers. Meanwhile, foundry-grade (+90 mm) coke prices remained unchanged at INR 36,400/t ex-Rajkot, indicating stable demand from the casting and foundry segment.

Rising imported coke offers strengthen domestic prices

Domestic coke prices continued to derive support from elevated import parity. Market participants noted that following the DGTR proposal to reduce anti-dumping duty on imported met coke, Indonesian suppliers raised FOB offer levels significantly, resulting in higher landed costs for Indian buyers. As per BigMint’s assessment Indonesian-origin BF-grade coke (65/63 CSR) was assessed at around $300/t CFR India, up by $9/t w-o-w.

In addition, a bulk trade for Indonesian BF coke (65/64 CSR, 30-90 mm) was reportedly concluded on 1 May at $276/t FOB Indonesia for July laycan shipment (15-20 July) for a cargo of around 30,000 t. The increase in FOB offers, coupled with elevated freight levels, has strengthened the competitiveness of domestic coke.

Firm coking coal market continues to support coke costs

As on 6 May, Australian premium hard coking coal (PHCC) prices increased by $2/t w-o-w to $233/t FOB Australia amid firm buying interest and tight availability of quality coking coal. However, there are unconfirmed reports of prices increasing by $5-10 in recent deals. Simultaneously, China’s domestic coke market remained stable, while negotiations for the third round of coke price hikes between steel mills and coke producers continued.

Market sentiment in China was supported by constrained raw material supply and relatively healthy steel margins, which helped sustain demand for coke. These factors collectively maintained cost pressure on global coke producers and supported firmness in Indian coke prices.

Pig iron market signals softer spot demand

On the downstream side, pig iron market indicators reflected relatively cautious sentiment. Steel-grade pig iron prices in Durgapur declined by INR 500/t w-o-w to INR 38,300/t ex-works, suggesting softer spot buying activity from foundries and secondary steel producers.

Additionally, NMDC’s pig iron auction held on 5 May witnessed subdued participation, with only 4,700 t booked out of the offered 8,000 t at a base price of INR 38,000/t ex-works. Bid prices were lower by INR 100/t compared to the previous auction held on 23 April, where the entire quantity was sold at INR 38,100/t ex-works. The weaker auction response indicates cautious procurement behaviour amid moderate downstream demand conditions.

Outlook

The Indian met coke market is expected to remain stable in the near term, supported by elevated import parity, firm coking coal prices, and higher Indonesian FOB offers. However, subdued pig iron demand and cautious buying sentiment from downstream consumers may restrict any sharp upward movement in domestic coke prices.

Going forward, market participants are likely to closely monitor developments in Chinese coke price negotiations, Australian coking coal trends, freight movements, and the final implementation of DGTR duty revisions, all of which could influence the direction of imported and domestic coke prices in the coming weeks.

Leave a Reply