- ADD uncertainty and cautious buying keep market under pressure

- Firm Chinese coke prices limit downside despite weak domestic demand

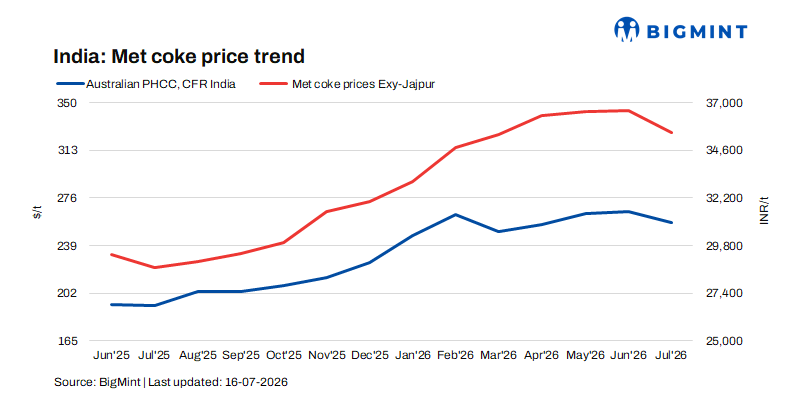

India’s met coke market exhibited mixed trends during the assessment week ended 16 July 2026, with prices softening in the eastern region while remaining stable in the west. The divergence reflected regional demand variations, subdued spot market activity, and persistent uncertainty surrounding the continuation of the anti-dumping duty (ADD) on imported metallurgical coke.

BF-grade met coke prices in eastern India inched down by around INR 100/t w-o-w to INR 35,150/t ex-Jajpur, as steelmakers adopted a cautious procurement approach amid weak spot demand and sufficient inventories. In contrast, prices in western India remained stable at INR 34,000/t ex-Gandhidham, supported by relatively healthier consumption from local steel producers.

Meanwhile, foundry-grade coke prices were stable at approximately INR 36,400/t ex-Rajkot, underpinned by consistent demand from the foundry sector.

A market participant noted, “With no anti-dumping duty currently applicable, imported coke has become more cost-competitive, putting additional pressure on domestic prices.”

Lower coking coal costs reduce raw material support

Cost support for domestic coke producers weakened during the week as premium hard coking coal prices declined. BigMint’s Premium Hard Coking Coal (PHCC) CFR Paradip assessment fell by $9/t w-o-w to $254/t last week, easing production costs for coke manufacturers and limiting any upward momentum in domestic coke prices.

Import market subdued despite competitive pricing

India’s imported met coke market remained largely inactive despite buyers actively seeking lower-priced cargoes. Uncertainty over the government’s stance on extending the anti-dumping duty continued to discourage fresh bookings, with most consumers preferring to defer purchases until greater policy clarity emerges.

Although international coke prices remained broadly supported by elevated coking coal costs, buying interest in India stayed muted. Reflecting subdued trading activity, BigMint’s Indonesian-origin BF-grade metallurgical coke (65/63 CSR) assessment edged down by $1/t w-o-w to $318/t CFR India.

China’s stable coke market provides global price support

China’s met coke market remained stable during the week, supported by healthy coke plant operating rates and acceptable producer margins. However, demand fundamentals weakened as declining steel mill profitability prompted maintenance shutdowns and expectations of lower pig iron production.

The proposed 10th round of coke price hikes remains under negotiation, with steel mills strongly resisting further increases amid growing expectations of a market correction. Nevertheless, constrained coking coal supply and stable freight rates continue to provide underlying support to global coke prices.

Pig iron market reflects cautious sentiment

India’s steel-grade pig iron market continued to reflect cautious buying sentiment. Prices in Durgapur increased by around INR 300/t w-o-w to INR 37,800/t ex-works, although auction participation remained subdued.

SAIL’s Bokaro Steel Plant (BSL) offered 14,000 t of steel-grade pig iron through auction on 10 July, of which only 7,000 t (50%) was sold at an average price of INR 36,500/t ex-works. While the average bid improved marginally by INR 100/t compared to the previous auction, only half of the offered volume was booked, indicating that buyers remain cautious despite modest price gains.

Outlook

India’s met coke market is expected to remain range-bound with a mild downside bias in the near term, as steelmakers continue need-based procurement amid weak margins and adequate inventories. Lower premium hard coking coal prices have reduced cost support, while uncertainty over the continuation of the anti-dumping duty (ADD) is keeping buyers cautious.

Delayed or absent ADD implementation could increase pressure from cheaper imports, whereas policy clarity, along with firm Chinese coke prices and tight coking coal supply, is likely to support the market and limit further downside.

Leave a Reply