- Imports decline to around 3 mnt in Apr-Sep’25

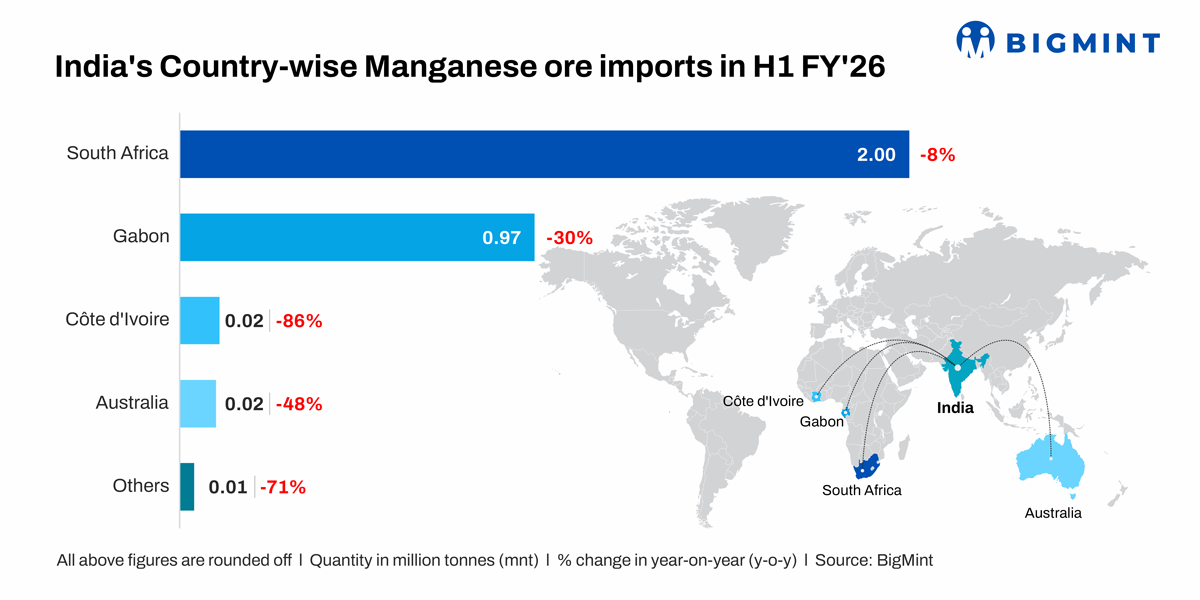

- South African ore exports down 8% y-o-y in H1FY’26

- Cost pressures weigh on alloys production, exports affected

Morning Brief: India’s manganese ore import volumes fell by 20% to 3.03 million tonnes (mnt) in April-September 2025 (H1FY’26) against 3.76 mnt in H1FY’25, as per provisional data with BigMint.

The downtrend in imports till date in the current fiscal points to a trend reversal: over FY’21-FY’25, the country’s manganese ore demand jumped by over 55% to 10.38 mnt from 6.66 mnt on steel capacity expansion, infrastructure push, and growth in manganese alloys production.

However, the impact of shrinking margins and weak global demand on domestic alloys production effected the trend reversal in H1FY’26.

Country- & grade-wise imports

South Africa continued to be largest source of India’s manganese ore imports. However, volumes fell by 8% y-o-y to 2 mnt in H1. Imports from other major sources such as Gabon and Australia fell by 30% and 48%, respectively.

On the other hand, imports of high grade (above Mn46%) fell by over 45% y-o-y, while imports of mid-grade ore (Mn35-46%) increased by 8% y-o-y to 2.58 mnt. Imports of mid-grade (Mn26-35%) ore also decreased sharply.

Why did imports drop in H1?

• Manganese alloys producers slash output: As many as five key ferro alloy producing units in Vizag have either cut or suspended manganese alloys production due to cost pressure. This is because raw material and electricity prices, which make up the bulk of production costs, have stayed firm, while realisations have declined due to the sustained drop in steel prices.

• Producers shift to other commodities: Some domestic smelters have reportedly shifted to manufacturing pig iron and other ferro alloys products like ferro chrome due to the cost pressure in the silico segment. This is a fairly common phenomenon at times of soaring production costs and narrowing margins as well as lack of global demand for Indian alloys. Naturally, the demand for imported manganese ore was affected due to this.

• Trade disruptions impact ferro manganese exports: Slower shipping movement in the MENA region due to heightened geopolitical risks (e.g., Red Sea and Gulf crises) has impacted Indian manganese alloys export prospects. Importers in these regions are deferring or re-negotiating contracts due to volatile exchange rates.

As per BigMint data, India’s ferro manganese exports to the UAE fell from nearly 75,500 t in H1FY’25 to 50,000 t in H1FY’26. This impacted ferro manganese production in India as well because the share of exports to total production of ferro manganese in the country is over 60%. Therefore, weaker exports of alloys directly impacted ore demand and imports.

• Global supplies impacted, domestic output up: South32’s manganese ore production was impacted from South Africa, as volumes fell by 8% y-o-y to 0.551 mnt in Jul-Sep’25 reflecting underground development activity at Wessels. Notably, FY’26 production guidance remains unchanged at 2,000 kwmt, with planned maintenance scheduled in the December quarter.

On the other hand, India’s manganese ore production inched up by 2% to 1.74 mnt in H1. India has steadily increased its manganese ore output in recent years. From 2.7 mnt in FY’21, production expanded by 41% to 3.80 mnt in FY’25. However, even with this growth, production still lags behind total demand.

Outlook

Imported manganese ore volumes are expected to rise in the near term as H1 imports remained lower than the previous fiscal, prompting buyers to replenish inventories. Moreover, the uptick in manganese alloys exports is likely to support import demand.

However, trends in steel production and overall market demand will remain key factors influencing the trajectory of ore imports.

Leave a Reply