- Benchmark iron ore fines index drops $2.5/t m-o-m

- Producers eye better margins in domestic market

- Chinese HRC, rebar prices decline by $8-12/t m-o-m

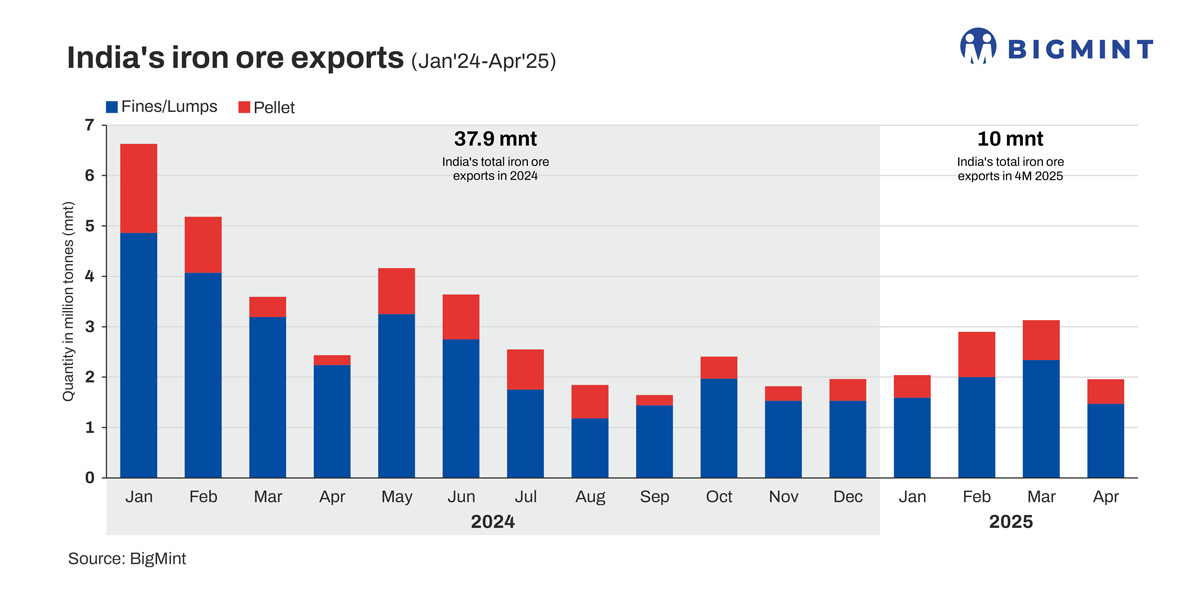

Morning Brief: India’s iron ore and pellet exports fell by 37% m-o-m in April 2025 to 1.96 million tonnes (mnt), a four-month low, according to data compiled by BigMint. For reference, March registered 3.13 mnt, a nine-month high.

Exports of iron ore fines and lumps totalled 1.47 mnt in April, reflecting a 37% drop from 2.34 mnt in March. Pellet shipments stood at 0.49 mnt, down by 38% m-o-m from 0.79 mnt.

Country-wise break-up

China received 73% of India’s exports in April, with shipments plunging by 52% m-o-m to 1.44 mnt from 2.98 mnt. Notably, in March, China’s crude steel output had reached a 10-month peak. Generally, China accounts for over 90% of India’s total exports.

However, exports to Malaysia and Indonesia increased significantly, to 0.22 mnt and 0.19 mnt, respectively, in April from 0.09 mnt and 0.06 mnt in March.

Company-wise shipments

Among the major exporters, Rungta Mines shipped 0.62 mnt, followed by KIOCL at 0.22 mnt, Vedanta at 0.19 mnt, and AM/NS India at 0.13 mnt.

Factors impacting India’s exports in April

- US-China tariff tensions prompt cautious buying: Trade tensions between the US and China escalated exponentially in April, with the US imposing tariffs of 145% on Chinese imports and China hitting back with 125% tariffs on American goods. This back-and-forth kept mills jittery, due to the potential impact on China’s exports of steel and downstream products such as electronics and automotive equipment.

In fact, amid the trade conflict with the US and growing protectionism in other countries, the China Iron and Steel Association (CISA) has forecast a 20-mnt drop in China’s exports of steel products in CY’25. The US tariff policy is expected to account for a 3-mnt loss in steel exports.

Consequently, steelmakers were cautious about their procurement of iron ore, which led to sluggish trades. Additionally, some steelmakers sourced material from port inventories rather than importing fresh cargo, for the sake of cost-effectiveness to help support margins.

- Export prices fall, margins turn unviable: Amid muted demand and competitive pricing from other regions, Indian traders had to reduce their iron ore export prices. However, this made it difficult for them to secure profits. As a result, Indian iron ore producers held back from the seaborne market.

To illustrate, the benchmark Fe 62% Australian iron ore fines index fell by $2.5/tonne (t) in April to a monthly average of $100/t CFR China, a seven-month low, against $102.5/t in March. India’s iron ore and pellet export prices mirrored this downtrend, with both plunging to their lowest in seven months.

BigMint’s export index for Indian low-grade iron ore fines (Fe 57%) declined by $2/t m-o-m in April to $60/t FOB Paradip, while the index for pellets (Fe 63%, 3% Al) exports fell by $3/t m-o-m to $93/t FOB east coast India in April.

- Miners divert material to domestic segment: Miners kept their attention on the domestic market amid poor realisations from exports. Domestic iron ore prices gained amid active procurement by steelmakers. Fines (Fe 62%) increased by 3% m-o-m to INR 5,240/t ($62/t), while lumps (5-18 mm, Fe 63%) climbed up by 6% to INR 7,550/t ($89/t), both ex-mines Odisha.

This price hike, in turn, boosted pellet (Fe 63%) tags by 2% m-o-m to INR 10,160/t ($120/t) DAP Raipur, supported by favourable sentiments in the sponge iron and billet markets.

Moreover, ex-plant realisations from domestic pellet transactions in April were, on average, around INR 2,000/t ($23/t) higher than those from export deals. The same in March stood at INR 1,700/t ($20/t).

- Lower steel prices weigh on Chinese import demand: Prices of Chinese hot-rolled coils (HRCs) and rebars declined m-o-m in April, pressuring demand for iron ore. Domestic HRC prices fell by RMB 90/t ($12/t) m-o-m to RMB 3,250/t ($447/t), while rebar tags eroded by RMB 60/t ($8/t) m-o-m to RMB 3,250/t ($447/t).

- Labour Day holidays slow down trade: The Chinese Labour Day holidays during 1-5 May further dampened trading activity during the month-end. There was limited and cautious buying, with market operations gradually winding down ahead of the holiday break.

Outlook

Uncertainty looms ahead. Although seaborne trade may rebound following the Labour Day holidays, trade activity is expected to remain under pressure due to geopolitical conflicts and lower buying interest in China.

However, if Chinese crude steel production remains strong – at around March levels – and steel prices continue to show weakness, preference for low-grade Indian fines may resurface.

Leave a Reply