- Raw material supply for steelmaking, pellet production tightens

- Imports gain traction, accelerating beneficiation remains hurdle

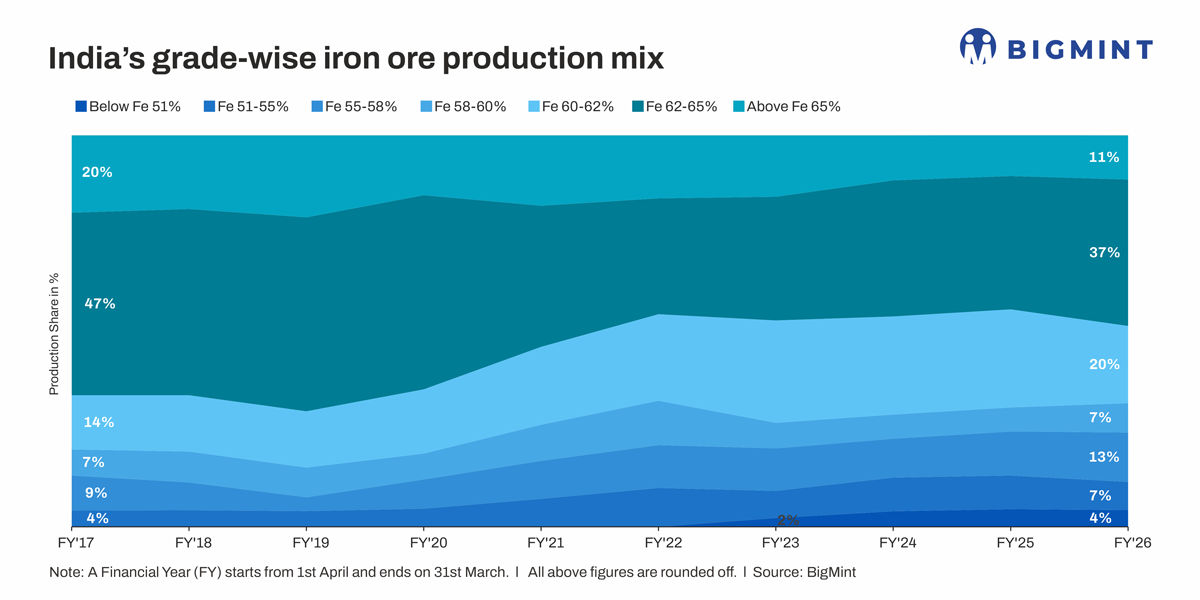

Data Deep Dive: India’s iron ore production has expanded steadily over the past decade, but the quality mix has deteriorated, limiting the usable quality for efficient steelmaking. Iron ore output rose 60% in the past 10 years, from 195 million tonnes (mnt) in FY’17 to an estimated 310 mnt in FY’26, according to BigMint data. However, the share of ore above Fe 62% has fallen sharply by 19 percentage points to 49% in FY’26 from around 66% in FY’17.

BigMint goes behind the scenes.

Falling high-grade supply tied to lower production from Odisha

The decline in India’s mid and high-grade iron ore output is directly linked to grade dilution in its key supplying states, particularly Odisha and, to a lesser extent, Chhattisgarh, which together anchor the country’s Fe ≥62% supply.

Odisha’s high-grade output has moderated in recent years, with its Fe 65%+ production falling sharply from 18 mnt in FY’20 to 6 mnt in FY’24 and only marginally recovering to a provisional 7 mnt in FY’26, even as its total output continued to rise from 147 mnt to 157 mnt over the same period.

Similarly, in Chhattisgarh, Fe 65%+ output has remained broadly range-bound at 14-17 mnt since FY’17, limiting its ability to offset Odisha’s decline.

At the national level, this has translated into a drop in Fe 65%+ production from a peak of 43 mnt in FY’19 to 34 mnt in FY’26, while its share in total output fell from around 20% (peak) till around FY’21 to 10-11% in FY’26.

Meanwhile, the share of Fe 62-65% ore in India’s total has shrunk from 45-50% in FY’17-20 to 30-37% in the subsequent years. Lower production from Odisha drove down volumes. Although output from Maharashtra has increased steadily, it has not been able to fill the supply gap left by Odisha.

Shift towards lower-grade ore intensifies

The decline in high-grade share is not only due to falling volumes alone but also a faster expansion in lower-grade production. While production of Fe 62-65% ore increased from 90.8 mt in FY’17 to 116 mt in FY’26, its share declined from 46.6% to 37.4% as total output grew faster. Meanwhile, mid-grade and low-grade categories saw consistent gains.

The Fe 60-62% ore share rose to 20% in FY’26 from 14% in FY’17, while lower bands such as Fe 55-58% and 51-55% expanded to a combined 20% in FY’26 from 13% in FY’17. This indicates a structural shift in mining output, driven by depletion of easily accessible high-grade reserves and increased extraction of lower-grade deposits.

Global benchmark also shifts lower

The global iron ore market has also witnessed this structural decline in ore quality. Benchmark specifications have gradually shifted from Fe 62% to Fe 61%, as the availability of high-grade material tightens. This adjustment follows Rio Tinto’s reduction of the iron content of its flagship Pilbara Blend Fines, historically around Fe 61.6% to below 61%. Similarly, BHP has already reduced the grade of its Mining Area C Fines and Newman High Grade Fines, with MAC Fines now around Fe 60.6%, as per reports.

Implications for India’s steel sector and trade

Adverse impact on BF, DRI productivity

Lower-grade ore generally carries higher alumina and silica content and raises the cost of steelmaking by increasing coke rate, flux consumption, and energy use while simultaneously reducing furnace productivity and hot metal quality.

This is particularly relevant as India aims to expand crude steel capacity while maintaining cost competitiveness. As per a report, India needs 437 mnt of iron ore to achieve the 2030 target of 300 mnt of crude steel production. However, in FY’26, of the 310 mnt produced, 24% (75 mnt) was below Fe 58%, generally unsuitable as BF feed.

Moreover, rapid expansions in direct reduced iron (DRI or sponge iron) and pellet production remain another concern. Both have almost doubled between FY’18 and FY’26, from 31 mnt to 60 mnt and 60 mnt to 117 mnt, respectively.

DR pellet production generally requires ore with high iron content, typically above Fe 67%, along with low levels of impurities, particularly alumina and silica. Low gangue content is critical because elevated alumina or silica increases slag volume and reduces pellet quality, which in turn lowers blast furnace or direct reduction efficiency. A major factor behind falling pellet capacity utilisation rates (down 10% over FY’21-26) has been the limited availability of higher grades and the overall deterioration in ore quality.

Surging iron ore imports

In FY’26, tightening availability of high-grade iron ore and pellets also drove Indian imports of both to around 12 mnt, a seven-year high and nearly double of FY’25 levels. Coastal steelmakers accounted for the bulk of this demand, with supplies largely sourced from Brazil and Oman.

In recent months, Vale has been increasingly targeting India’s coastal steelmakers that benefit from logistical advantages. Brazilian ore offers a structural advantage due to lower gangue content, particularly alumina and silica, compared to domestic material.

Similarly, pellets with Fe 65% and alumina of around 1% were imported due to competitive prices, while Indian producers typically supply pellets in the Fe 62.5-63% range.

The shift underscores a growing reliance on seaborne material to bridge quality gaps in domestic supply.

Greater focus on beneficiation

The decline in high-grade supply will also necessitate a faster increase in beneficiation across the value chain. However, this could elevate costs and energy consumption.

Beneficiation requires high capital investment in plant and machinery, along with significant operating costs due to energy-intensive processing. It also generates large volumes of tailings, creating challenges around land acquisition, disposal, and environmental clearances. Additionally, beneficiation is water-intensive, which poses operational and environmental risks. Crucially, not all low-grade ore can be upgraded economically to Fe 62%+, limiting the viability of beneficiation processes.

A significant chunk (estimated at around 40% in FY’25) of India’s 143-mnt beneficiation capacity remains unutilised. In 2022, the government had proposed that miners compulsorily beneficiate up to 80% of ore below Fe 58% to at least Fe 62%, with penalties such as higher royalties or even lease cancellation for non-compliance.

However, this move generated strong opposition at that time. In 2025, during the Ministry of Steel’s stakeholder consultations, steelmakers again highlighted the economic non-viability of beneficiation under current business models.

Notably, in 2018, the Indian Bureau of Mines (IBM) had retained the cut-off grade for haematitic iron ore at Fe 45% (revised downward from Fe 55% in 2009). During the review period, many steel producers had argued to raise the limit back to Fe 50-55% due to technical and beneficiation constraints.

Outlook

With limited operationalisation of auctioned mines, BigMint expects high-grade iron ore availability to be constrained in FY’27 as well. This would sustain reliance on imports, especially for coastal steelmakers. According to a report by the Australian government, India’s iron imports could rise to a projected 20 mnt in CY’26 and 30 mnt in CY’27.

This also reflects major steelmakers’ efforts to ensure raw material security by turning to overseas suppliers. For example, in January 2026, Tata Steel brought a trial shipment of BF-grade Fe 64% iron ore lumps from its Canadian arm, Tata Steel Minerals Canada (TSMC), to India. Licences for a combined 51 mnt/year of its approved environmental clearances (ECs) are set to expire by 2030-31. While JSW Steel ramped up its procurement from Vale last year, in March this year, it also procured cargo from BHP for trial purposes.

Meanwhile, in late 2025, the government has had discussions on enhancing raw material security; consequently, policy support is expected for scaling beneficiation capacity/boosting capacity utilisation and accelerating iron ore production. However, the impact of any such measure is likely to be felt in the subsequent years rather than the near term.

Leave a Reply