- Iron ore, pellet imports reach around 10.6 mnt in Jan-Nov’25

- Imports have hit the highest since 2018 – a 7-year high

- Govt mulls reforms to ramp up production from auctioned mines

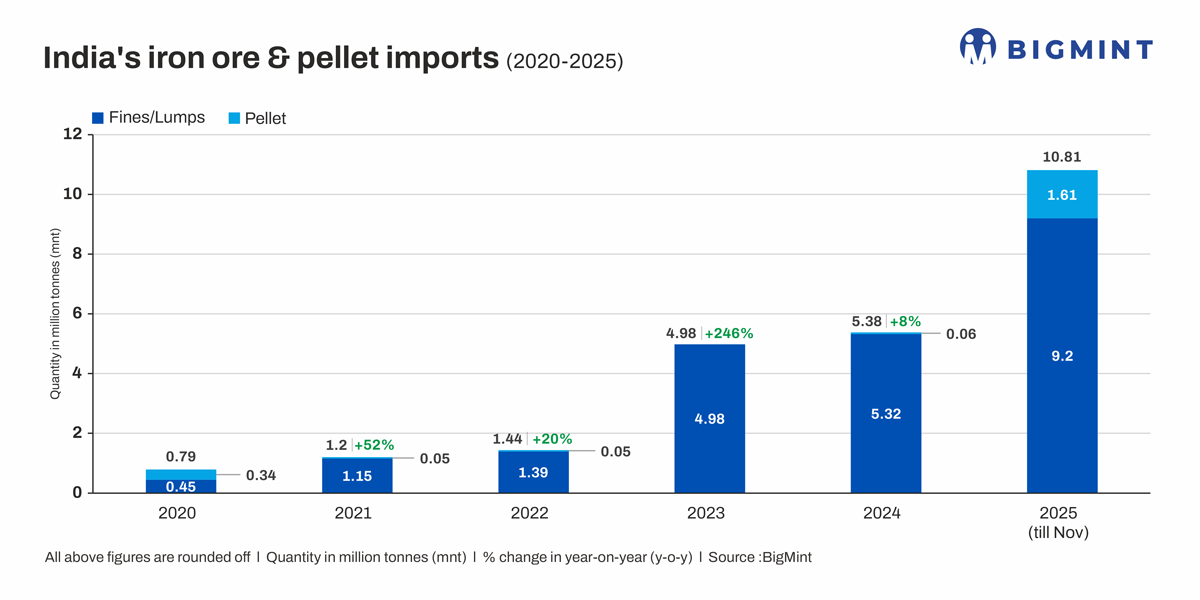

Morning Brief: India’s iron ore imports have already crossed 10 mnt in the first 11 months of CY25. In the first 11 months, total imports stood at 10.6 million tonnes (mnt), as per provisional data maintained with BigMint. Out of this, 9 mnt is fines and lumps and the rest, 1.55 mnt, iron pellets.

Imports have hit the highest since 2018 i.e. a seven-year high, and it is only the third time in history that annual imports have crossed the 10 mnt mark. In 2018, mining suspension at a few mines in Odisha had prompted the surge in imports.

JSW top importer, Brazil top exporter

Amongst iron ore importers, JSW Steel topped the list at 8.7 mnt during 11MCY’25. Other importers were AOne Steel, Balaji Malt, etc. Brazil accounted for the largest share of imports to India at 4.2 mnt followed by Oman (2.5 mnt) and Australia (1.5 mnt).

Amongst pellet importers, Suryadev was the largest at 0.22 mnt followed by Delta Global. Oman (1.5 mnt) was the largest source of imports followed by the UAE. As per sources, Iranian pellets were sourced by mills in western and southern India throughout the year.

Why did iron ore & pellet imports rise in CY’25?

- Only marginal rise in domestic iron ore output: India’s iron ore output was recorded at 237 mnt in January-October 2025 as against 233.3 mnt in the same period last year. This marginal rise in India’s iron ore production hardly matched up to the 10-12% y-o-y surge in crude steel production. India’s crude steel production stood at 135.3 mnt in 10MCY’25. Thus imports can be seen as plugging domestic shortage to an extent.

In fact Brazilian iron ore giant Vale has gone on record saying that India is emerging as a top destination coinciding with the gradual decline of steel production and iron ore demand in China. Vale’s high-grade ore blends well with India’s lower-quality supply are creating opportunities for both markets, according to Vale.

In 2025, demand outpaced domestic production and availability of higher-grade ores was a concern. Also, the delay in production from auctioned mines created a tight market. Prolonged monsoons and robust demand tightened domestic supply, prompting a rise in iron ore imports. For port-based plants such as JSW, imports were by far the best option due to high domestic logistics costs.

- Quality requirements: Quality concerns with domestic iron ore drove mills to favour imports. Indian ore typically contains higher levels of gangue, especially alumina and silica, compared to Brazilian material, making it less suitable for efficient sintering and blast furnace operations. Notably, high-grade (Fe65%), low alumina (max 1%) pellets were available for imports which are not easily obtained in the domestic market, as producers typically offer Fe62.5-63% pellets.

- Surge in pellet imports: Regional supply issues and high domestic transportation costs were the most significant factors that pushed up pellet imports. For example, market participants grappled with material scarcity in Bellary and Odisha. There was limited availability of the required iron ore grades in Bellary, which affected production of pellets.

Transporting pellets from central to western India entails logistical challenges largely due to the prohibitively high freights involved. This, coupled with the availability of overseas material at favourable prices, further tilted the scales in favour of imports.

Outlook

While domestic miners such as NMDC and others are drawing up plans to enhance production of high-grade concentrate and pellet feed, the rapid depletion of high-grade iron ore will necessarily create the requirement for imports amid calls to raise the quality of domestic steel production as well as optimising energy efficiency in ore processing, reduction and smelting operations.

However, due to the fact that only 37 have started operations out of the 138 auctioned since the amendment of the MMDR Act, the government has mulled reform measures and specific milestone-based timelines for governing both mining leases and composite licences. These measures are expected to result in increased domestic production going forward which may alleviate the need for imports to an extent.

Leave a Reply