- Exports fall by 17 mnt y-o-y from a 3-year high in FY’24

- Downturn in Chinese demand weighs on shipments

- Global trade war, China’s steel output cuts to impact sentiments

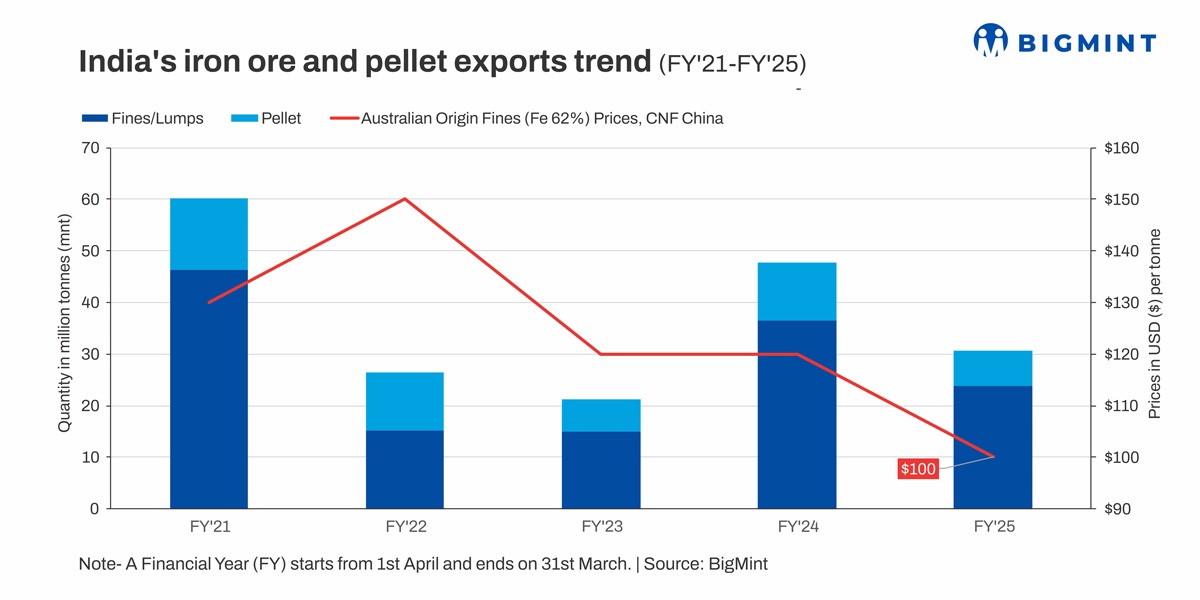

Morning Brief: India’s iron ore and pellet exports decreased by over 17 million tonnes (mnt) y-o-y in FY’25, with total exports declining to around 30 mnt from a high base of 47 mnt in FY’24, as per BigMint data. Total shipments decreased sharply by over 35% y-o-y.

Exports of iron ore fines and lumps were recorded at nearly 24 mnt, while pellet sales overseas were assessed at 6.8 mnt in the just-concluded fiscal. In FY’24, iron ore exports stood at 36.5 mnt and pellets over 11 mnt, a three-year high.

Country & company-wise exports

India’s exports of the key steelmaking raw materials were predominantly to China which accounted for 90% of exports in FY’25, although volumes fell sharply to 26.8 mnt compared with 46 mnt in the preceding fiscal. Malaysia and Indonesia were among the other importers but volumes were insignificant.

Among Indian suppliers, Rungta Mines was the top exporter of iron ore, at over 8 mnt, while JSW grabbed the distant second spot with total iron ore exports at around 2.9 mnt in FY’25. Vedanta shipped around 2.2 mnt.

Factors pressuring iron ore, pellet exports

Chinese steel production falls: As India’s largest importer of iron ore, China’s demand determines the trajectory of the market. China’s demand for iron ore and pellets dwindled on declining steel production in FY’25. The country produced 924 mnt of crude steel between April’24 and February’25, a decrease of 1% y-o-y, as per data published by the World Steel Association (WSA).

The downtrend in steel production is primarily due to a debt crisis and overcapacity in the real estate and construction sector, slowdown in infrastructure, as well as declining margins of producers. Therefore, even though iron ore imports in general were high, the general slowdown in demand led to accumulation of port inventories in China which further weighed on demand.

Global iron ore prices drop: Data show that average global iron ore prices deteriorated in FY’25 owing to weak Chinese and global market sentiments. This served to discourage Indian exporters. Average benchmark Fe 62% iron ore fines prices in FY’25 fell to $100/t CFR China versus $120/t in FY’24. The steady decline in export prices, and widening discounts on lower grades of iron ore fines in the seaborne market, made domestic sales more preferable for many Indian suppliers compared to exports.

Lower exports from Karnataka: India’s exports fell as shipments from key iron ore producing state Karnataka edged down sharply. Iron ore exports from Karnataka fell to 0.83 mnt in FY’25 compared with 3.65 mnt in FY’24. Although export trades from Karnataka had been facilitated by the lifting of restrictions by the Supreme Court, shortage of certain grades – especially low-grade fines – continues to persist. Miners in the state are primarily focusing on meeting domestic demand rather than catering to the export market.

Higher domestic realisations for pellets: Sources informed BigMint that domestic pellet ex plant realisation in Odisha averaged over INR 7,500/t in FY’25, while pellet export ex plant realisation averaged around INR 6,200-6,400/t. Therefore, higher domestic realisations naturally discouraged exports.

Outlook

Steel production cuts in China and weak market outlook for iron ore globally will continue to weigh on India’s iron ore exports. Continued downtrend in the property and construction sector, projected decline in steel consumption, and the lethal impact of global tariffs and anti-dumping duties on steel exports are likely to affect the demand for iron ore in China. The overall market uncertainty is hardly conducive to trade.

Moreover, global prices of iron ore are expected to edge down further on easing supplies, thereby disincentivising exports from India.

Leave a Reply