- Better domestic realisation keeps exports subdued

- Weak Chinese holiday demand puts pressure on demand

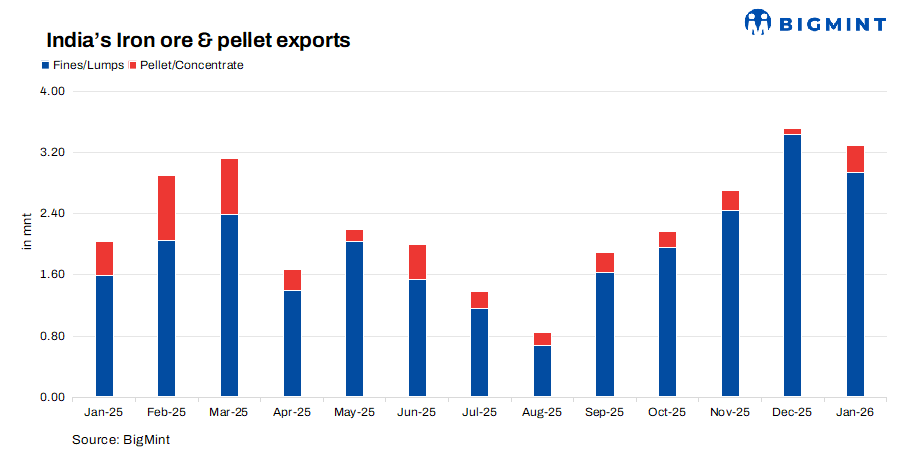

India’s exports of iron ore and pellets edged down by 6.25% m-o-m to around 3.3 million tonnes (mnt) in January, as per BigMint data, from 3.52 mnt in December. Monthly exports were 2.94 mnt of iron ore and 0.36 mnt of pellets. Iron ore and pellet exports have remained volatile in the last six months.

As per BigMint’s data, iron ore and pellet exports rose from 2.04 mnt in January’25 to 3.3 mnt in January’26.

Top exporters, ports

Exports to China fell from 2.79 mnt in December to 2.56 mnt in January. Notably, Malaysia almost doubled its imports from India to around 0.27 mnt this month against 0.13 mnt a month prior.

Rungta Mines and Vedanta remained the largest exporters contributing 1.33 mnt and 0.48 mnt, respectively. These were followed by Arcelor Mittal and Nippon Steel and Ramgad Minerals and Mining at 0.3 and 0.16 mnt in January.

The east coast remained active throughout with major shipments from Paradeep (1.85 mnt), Dhamra (0.49 mnt) and Krishnapatnam port (0.27 mnt).

Notably, stacked up inventories weighed on any urgent procurement needs, limiting closure of deals.

Why iron ore exports slowed

Weak China demand: Chinese portside iron ore and pellet inventories were recorded at 161.24 mnt in Jan’26 rising by 5.5% against 152.8 mnt in Dec’25. Ample inventories of fines, lumps, and pellets in the market remained a key reason behind the slowdown in exports. With Chinese port stocks already comfortable and the upcoming Lunar New Year approaching, procurement activity stayed limited. At the same time, the seaborne market was highly competitive, with mills using other regions for sourcing raw materials, which further reduced buying urgency for Indian cargoes. In addition, many Chinese mills are operating at reduced capacity, keeping raw material demand under pressure.

Sellers focus on domestic market: Monthly average export prices in January for low-grade iron ore fines (Fe 57%) FOB Paradip held steady at $66.5/t m-o-m. Stagnant prices were a direct reflection of weakening global iron ore prices. Fe 61% CNF China prices held at $105.6/dmt. On the other hand, domestic low-grade prices inched up by INR 150-200/t m-o-m. Thus, the domestic market remained the key focus of sellers. Tighter availability in the domestic market kept exports lower.

Meanwhile, the pellet export (6-20 mm, Fe 63%) index stood at $106/t FOB east coast, largely stable against December.

Export sentiment remained cautious with strong competition in the seaborne market due to high inventories and alternative supplies, while Chinese mills continued to run below full capacity. Single-mine cargoes saw relatively better interest, but buyers remained cautious, with most mills preferring more cost-effective port-based material.

Outlook

The export market is likely to remain quiet in February, with buying continuing to remain subdued due to the Chinese holidays and pressure on global prices.

Leave a Reply