- BF rebar prices drop over 4% in May, HRC just about 1%

- Inventory pressure, widening gap with IF prices, weigh on BF rebar

- HRC prices stable amid wide differential with imports, fresh export bookings

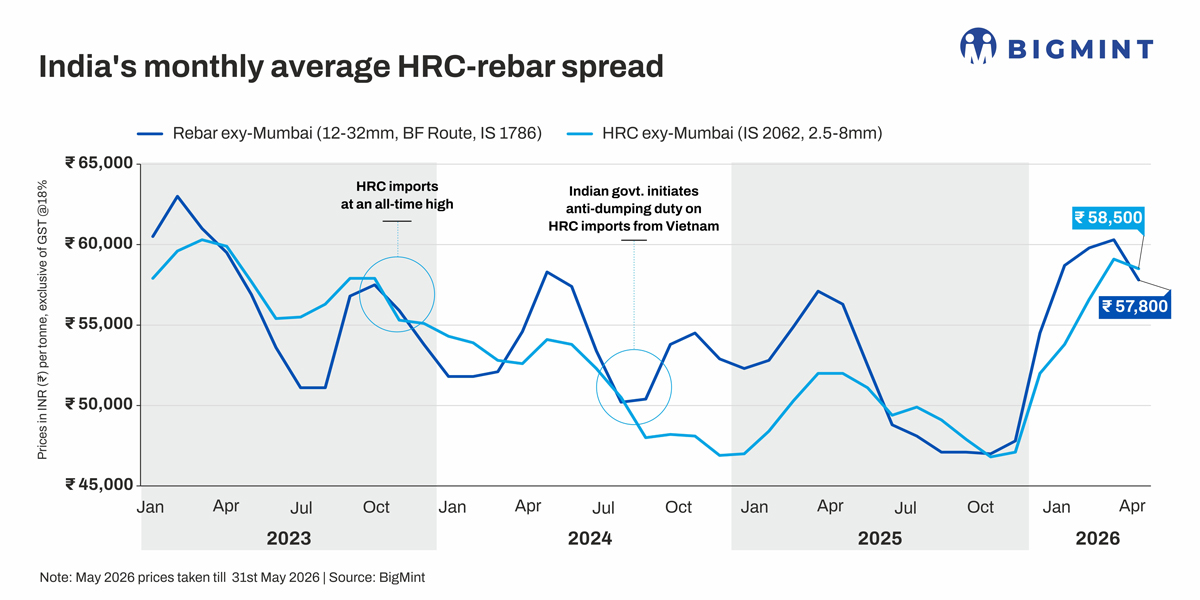

Morning Brief: The price spread between domestic hot rolled coil (HRC, IS 2062, 2.5-8mm) and blast furnace-origin rebar (12-32mm, IS 1786) returned to positive zone after a gap of six months since November 2025. The domestic HRC-rebar spread, calculated on the basis of monthly average prices reported by BigMint, was in negative zone since November 2025 despite the imposition of safeguard duty on flat steel imports in end-December.

The spread stood at INR 700/t in May compared with a reverse spread of – INR 1,200/t in April. While average HRC prices declined by 1.02% m-o-m in May, rebar prices fell by over 4%, as per data. Significantly, while BigMint’s India steel composite index fell 3.7 percentage points in May and the rebar index declined by over 7 percentage points, HRC was relatively stable – dropping around 1.7 percentage points.

Steel prices came under pressure in May, with the construction sector witnessing muted activity and inventory accumulation at the distributor level. The cessation of violent conflict in the Middle East, and gradual stability retuning in fuel and freight markets, weighed on steel prices. Government data also showed a deceleration in demand compared to April.

However, rebar prices were directly affected compared to HRC, bearing the immediate brunt of weakness in the construction sector. On the other hand, HRC continued to remain largely stable on the back of strong manufacturing activity in April and May but weak exports weighed on prices.

In normal circumstances, the spread usually stands at around INR 5,000/t.

Price movements in May

HRC prices decline in May from initial hikes

Leading steelmakers had initially revised their list prices upward for early May, raising both HRC and CRC prices by INR 1,000/t ($11/t). The price uptick was driven by scheduled maintenance shutdowns at key steel mills. These planned outages temporarily constrained HRC production by approximately 10-15%.

However, market conditions remained weak through late May, with buyers restricting procurement to immediate requirements and distributors reporting slower movement across regional markets. Mills continued focusing on inventory liquidation and dispatch discipline amid subdued spot demand and cautious downstream participation.

Steel consumption moderated in April following the fiscal year-end peak, reinforcing softer visible demand entering the monsoon quarter. However, broader industrial indicators remained constructive. Manufacturing PMI remained in expansionary territory during April, supported by stronger new orders and production activity, while industrial production, logistics activity, and power consumption continued to show resilience despite external uncertainties.

Export bookings rise but currency drop affects prices: Higher export booking volumes in May as against April was supportive for prices. With the domestic market for HRC remaining subdued, mills sought to redirect volumes to the export markets. Bookings increased, especially to the Middle East and Vietnam, even as mills tried to relieve themselves of inventory pressure by channelling material to the export market.

Another factor which supported exports was the rapid deterioration in the INR, with the currency dropping to historic lows against the USD. A depreciated INR made exports lucrative for the domestic mills even though overall realisations declined. This turnaround in export sentiment supported HRC prices.

China export HRC prices stable amid Yuan appreciation: Domestic HRC prices received some support from stable Chinese HRC export prices amid rising domestic prices due to surging coke rates, as well as the uptick in the RMB. The currency has appreciated 6.54% against the USD over the past year. The appreciation of the RMB and the depreciation of INR led to Indian exporters finding themselves in a comfortable position vis-à-vis their Chinese counterparts. The supportive Chinese HRC price environment also kept domestic prices stable.

Imports still expensive: Despite the surge in bulk HRC imports in April and May, especially from China, price dynamics was more affected by sentiment in the domestic construction and manufacturing sectors, with weakness in construction activity impacting downstream steel demand.

Imported HRC prices were higher than domestic: the differential with imports from non-FTA countries, primarily China, was assessed at over INR 7,000/t, while the spread with HRC (landed) from FTA countries was over INR 4,000/t. Therefore, the rise in imports was due to other causes which did not distort domestic prices even as currency depreciation made imports unviable.

Rebar prices correct from elevated levels

Rebar prices softened during late May as distributors reduced offers amid persistent selling pressure and slower construction-linked demand. Buyers continued following a need-based procurement strategy amid uncertain pricing trends and delayed project execution during the monsoon phase.

Prevailing heatwaves in many regions, unavailability of labour due to various factors directly affected construction momentum. On the other hand, the widening gap with IF-route rebar prices, which softened throughout May, impacted BF rebar prices.

Supply-side pressure remains a key concern. Inventories at major mills reportedly increased materially entering the quarter, while distributors continue holding elevated stock levels amid slower market movement and softer project offtake. This inventory overhang is expected to keep mills under pressure to prioritise dispatches and maintain competitive pricing.

Raw material sentiment mixed: Raw material conditions remain mixed. Iron ore prices corrected amid softer steel demand and improved ore availability, while coking coal prices remained relatively firm due to tighter seaborne supply.

Outlook

Elevated wholesale inflation in fuel and industrial inputs may help limit aggressive downside correction in steel prices, though current market conditions remain fundamentally demand constrained. Despite cost inflation, mills are expected to roll over HRC prices for June amid subdued trade market sentiment.

The domestic mills are also awaiting the rollout of country-specific EU import quotas from June, which are expected to slash total imports by 47%. Weak export sentiment in the EU will naturally affect domestic HRC prices going forward.

After the rally in March and April, rebar prices are expected to remain subdued till August, with the monsoon quarter intervening. In June, we expect rebar prices to remain under pressure in the absence of momentum in the construction sector. Although monsoon delay might propel construction momentum somewhat government spending is bound to be affected due to the higher forex outflow on account of fuel prices.

However, manufacturing activity surged in May, with the HSBC PMI rising to 55. Manufacturing demand is expected to support HRC prices and downstream steel demand. BigMint expects the HRC-rebar spread to widen in June.

Leave a Reply