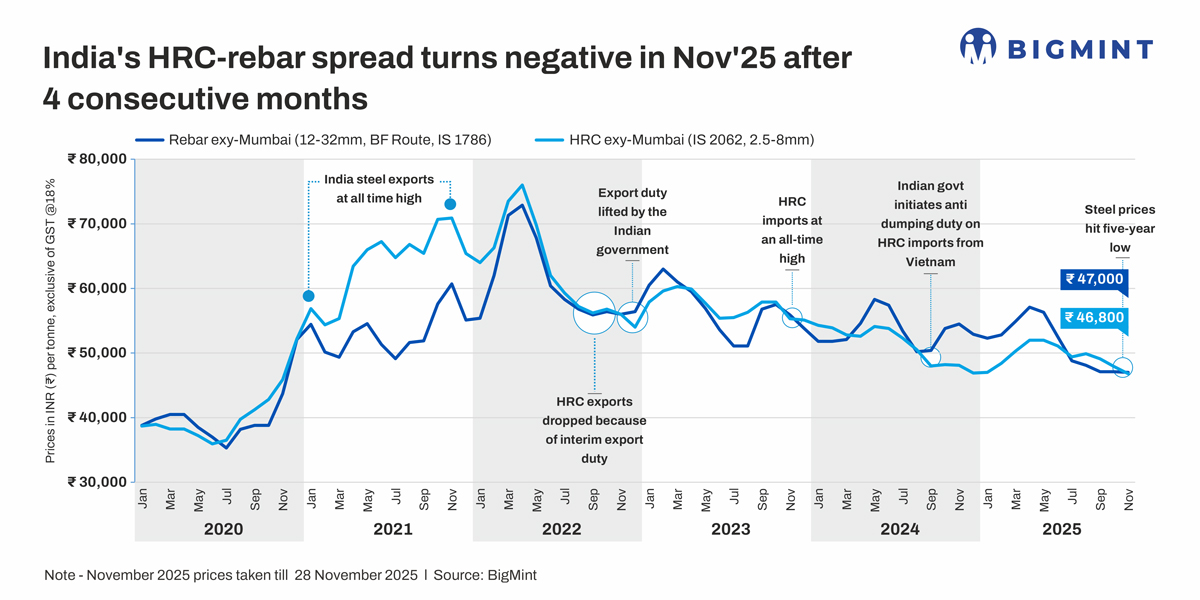

- Spread recorded at – INR 300/t compared to INR 800/t in Oct

- HRC prices drop by 2.3% m-o-m, rebar falls just 0.2%

- Market expecting an imminent price correction in Dec

Morning Brief: Indian steel prices in November 2025 showed a downward trend due to the slowdown in trade momentum and the rapid buildup of inventories belying expectations of a post-festive trend reversal – some signs of which were seen toward the end of October. Encouraging economic policies such as GST rationalisation in the auto sector and the expected pickup in construction and infrastructure activities after Diwali failed to have any significant impact on steel market sentiments and prices.

The spread, or gap, between domestic HRC (IS 2062, 2.5-8mm) and blast furnace-origin rebar (12-32mm, IS 1786) again turned negative in November, as per BigMint assessment, after remaining in the positive zone for fourth months from July to October. Compared with the INR 800/t expansion in October, the spread swung back again to the negative zone in November: – INR 300/t. While weighted average HRC prices declined by INR 1,100/t m-o-m in November (or 2.3%), rebar prices decreased by just INR 100/t on-month, or 0.2%.

Under normal market conditions HRC commands a premium of around INR 4,000-5,000/t over BF rebar. However, persistent weakness in global steel prices from end-2024 onwards has eroded domestic flat steel prices and pushed the spread into reverse zone.

Steel price scenario in Nov’25

HRC market movements: Thanks to most of the leading primary producers hiking list prices of HRC for November sales by INR 1,250/t compared to end-October, the trade market witnessed a fleeting phase of dynamism in the beginning of last month. Firm domestic iron ore prices, the temporary uptick in exports to the EU and safeguard measures restraining the inflow of steel imports kept sentiments positive.

However, trade prices kept edging down throughout the month as the list price hikes by some Tier-1 producers were ill-absorbed by the market, which continued to witness poor demand even as supplies remained high. Mills and distributors actively pushed sales as piling inventories and liquidity constraints affected demand. Stock levels at distributors and company yards were elevated.

Oversupply and high inventory levels led to a steady decline in prices. Incidentally, the government’s decision to suspend BIS norms for certain steel product imports is expected to cover all aspects of end-user demand and lead to further supply and price normalisation. In the last week of November, buyers delayed purchases expecting an imminent price correction in December.

Rebar prices soften: Rebar prices in the Mumbai market, as per BigMint assessment, had edged up in early November due to the hike in semi-finished steel prices, IF rebar prices and renewed dynamism in the market. However, high production levels soon led to an inventory buildup.

Rebar production from the major mills rose 3% m-o-m to 4.21 mnt in October supported by higher output from JSW Steel, Tata Steel and Jindal Steel. However, demand remained sluggish, causing inventory buildup at mills. Prices in November fell to a five-year low on muted trading activity across markets, with sellers offering discounts to clear inventories. Surplus material in the trade channel intensified the pressure on prices, market sources informed.

Outlook

Elevated supply continues to pressure prices and is delaying any meaningful market recovery in both the longs and flats segments. While there is a latent optimism regarding a rebound in real demand and consumption in the upcoming January-March quarter, declining production and demand in China, as well as key markets such as the EU and Japan, is likely to impede any recovery in global steel prices.

The impact of this is likely to be adverse for domestic steel prices from which the domestic industry is hardly immune.

Leave a Reply