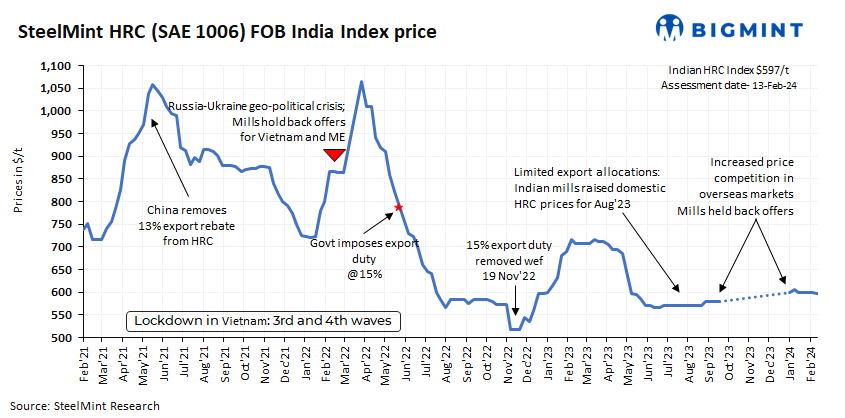

BigMint’s India HRC (SAE 1006) export index (for the Middle East and Vietnam) inched down w-o-w to $597/tonne (t) FOB against $599/t FOB east coast India, amid weakened global market sentiment. This decline comes amidst holiday periods in Vietnam and China. Additionally, Indian HRC export offers to the European Union (EU) witnessed a decrease of $10/t w-o-w.

The Lunar New Year holidays in China and the Tet holidays in Vietnam have created a lull in demand, impacting Indian HRC exports. With mills and buyers on a break, trading activity slowed down significantly leading to the drop in the export index.

Market updates:

1. Offers to ME stable w-o-w: Indian steel mills’ offers to ME remained stable w-o-w to $630-635/t CFR. No major bookings were heard as market participants are waiting for Chinese players to return from the Lunar New Year holidays. Moreover, last heard Chinese import offers to the ME before the holidays were heard at $605-610/t CFR UAE.

2. Offers to EU drop: Indian HRC exports to Europe (S275, 3mm) dropped by $5-10/t w-o-w. Current offers are around $705-710/t CFR Antwerp ($655-665/t FOB east-coast India) against $715-720/t CFR Antwerp last week. Europe’s hot-rolled coil market faces sluggish domestic demand and buyer hesitation. Unclear price trends and weak end-user demand leave buyers cautious, forcing producers to offer discounts for February stability. While import offers are cheaper, quota concerns and shipping disruptions keep them less attractive, highlighting the market’s current uncertainty.

Outlook:

The near-term outlook for Indian HRC exports remains mixed. The revival of demand post-holidays in key destinations and the evolution of Chinese pricing strategies will be crucial factors determining the sector’s performance.