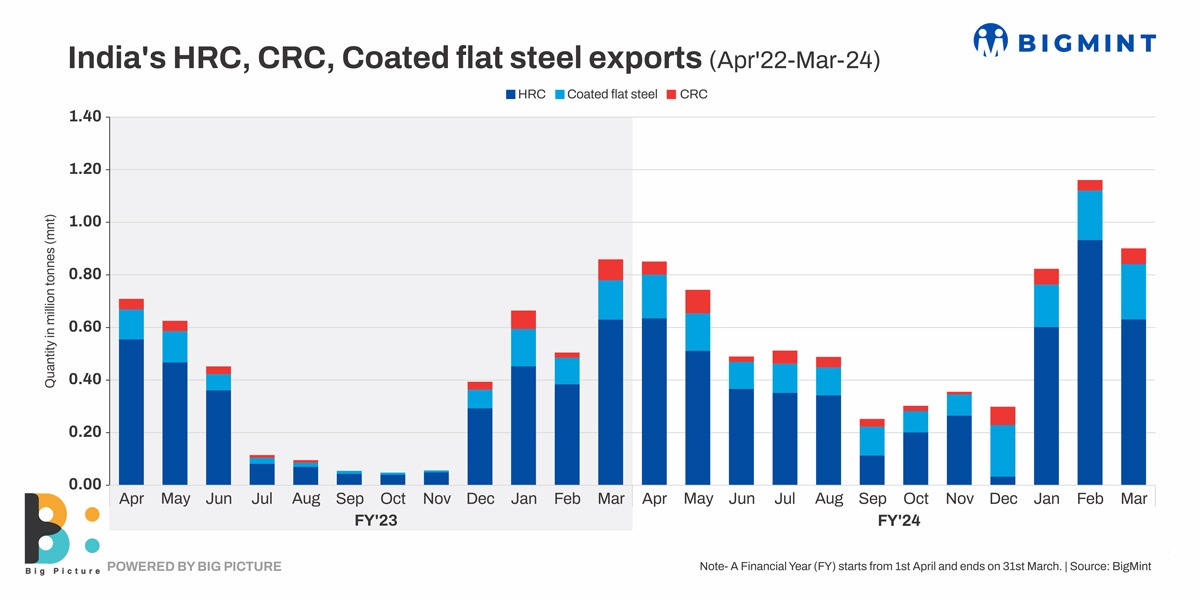

HRC production increased 6% to 14 million tonnes (mnt) in Q1 (January-March, 2024) against 13 mnt in Q4CY’23 (October-December) and 13% from 12.55 mnt in Q1CY’23. This was mainly on account of increased supplies in the market. NMDC’s Nagarnar Steel Plant starting commercial production from late last year while JSPL commissioned its 5.5 mntpa hot strip mill at Angul. But demand lagged behind supply which pressured down prices. Tier-1 mills, challenged by the triple whammy of low domestic and overseas demand and excess supply, eventually resorted to maintenance shutdowns. Some put their hot strip mills (HSMs) on maintenance shutdown to reduce HRC production especially from April. This impacted availability of the base material for cold rolling and led to tighter CRC supply. This, in turn, kept CRC prices supported with a marginal m-o-m drop. Higher HRC diversion for CRC downstream use: Mills also resorted to diverting their HRCs towards coated flat steel production in-house, and this averaged an astounding around 90%. Downstream CRC utilisation averaged 8.83 mnt in January-March 2024 against 7.98 mnt in Q4CY’23 and 7.52 mnt in Q1CY’23. Naturally, saddled with HRC inventory, mills evolved a good way to utilise the same. This also kept CRC prices propped-up especially since galvanised exports rose q-o-q to 667,000 t in Q1 against 323,000 tonnes in October-December 2023.