- Domestic scrap consumption rises amid increased generation

- Reliance on domestic scrap rises as GST challenges get settled

- Will FY’25 consumption remain range-bound?

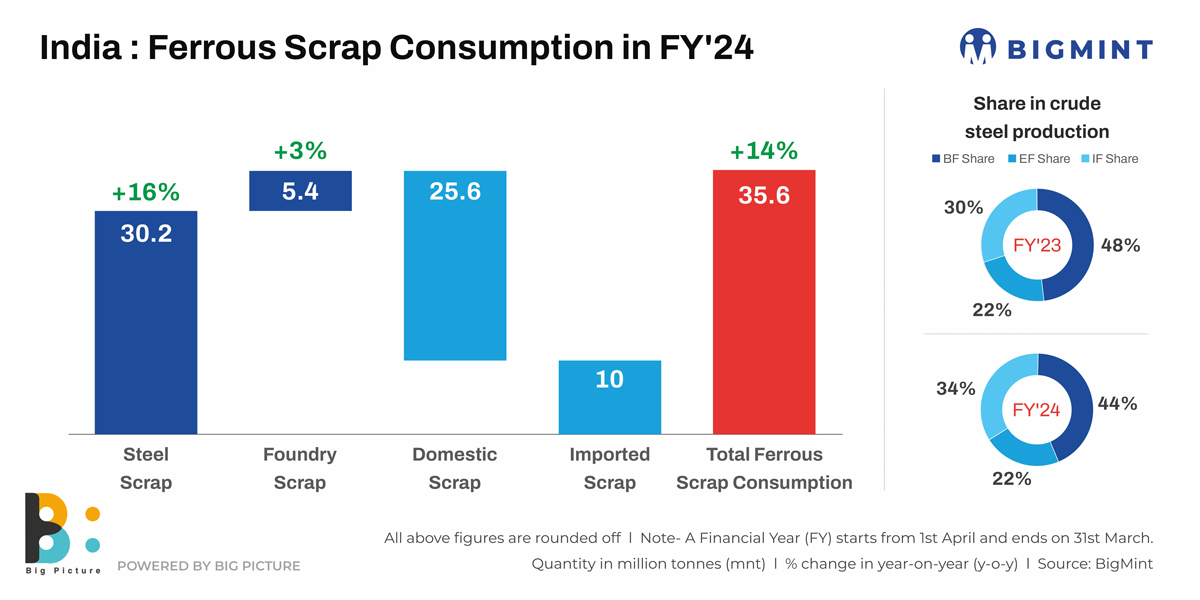

Morning Brief: India’s total domestic ferrous scrap consumption (including steel and foundry) is slated to rise a moderate 14% to around 36 million tonnes (mnt) in financial year 2023-24 (FY’24), as per BigMint’s estimates. Consumption volumes in FY’23 were at 31 mnt.

Domestic scrap consumption: In the 36-mnt pie, the share of domestic ferrous scrap consumption is expected to rise a sizeable 22% to over 26 mnt from the present 21 mnt although the imported variety’s share is likely to remain largely stable at 10 mnt y-o-y.

Steel segment’s share: The steel segment’s share in consumption in FY’24 will possibly rise 16% to 30 mnt (from 26 mnt in FY’23) while foundry’s intake will remain more or less flat at 5.4 mnt from 5.2 mnt last fiscal.

Factors that will aid rise in scrap consumption this fiscal

1) Rise in electric furnace-route production: India’s crude steel production is expected to rise an estimated 9% to 138 mnt in FY’24 from the current 126 mnt. And, a major portion of this additional 12 mnt addition is slated to come from the electric furnace segment, where scrap is a key raw material.

2) Share of blast furnace route to drop: As a result, share of blast furnace-route steel-making is expected to drop to 44% by the end of the current fiscal from the present 48% while contribution from the electric furnace segment will rise to 56% (from 52% in FY’23).

3) Domestic generation rises amid smoothened GST issues: Domestic scrap consumption is also likely to be up a considerable 28%, on the back of increased domestic scrap generation and collection. BigMint understands that the goods and services tax (GST) issues, which had been plaguing the market in the initial part of the fiscal, have been smoothened out. Resultantly, with market players more comfortable in handling local transactions, generation and collection have also received a fillip. For instance, giving an indication of the rising domestic generation trend, for the full year of 2023, the same rose to an estimated 27.50 mnt against 26.50 mnt in 2022.

On the other hand, imported scrap consumption will possibly remain static y-o-y in FY’24 at around 10 mnt.

Outlook

Looking ahead, at FY’25, BigMint estimates that ferrous scrap consumption will not show any sharp upward swing but remain more or less static at FY’24 levels of about 26 mnt. And, certain factors can drive this scenario: First, the new crude steel-making capacity additions in the pipeline from tier-1 mills will pertain to the blast furnace route as these projects had been conceived much earlier, prior to the formulation of emission goals by the Indian government. Secondly, sponge iron production may remain robust in India on the back of an expected moderation in domestic thermal coal prices amid higher production. Lastly, the other three major ferrous scrap importers – Turkiye, Bangladesh and Pakistan – may boost their consumption of this raw material, which would lead to less scrap being available for India at competitive prices. As per the IMF’s Global Economic Outlook, global growth is estimated to remain at 3.1% in CY’24 and rise to 3.2% in CY’25 while headline inflation is expected to fall to 5.8% in CY’24 and to 4.4% in CY’25.