- Growing renewables supply lowers prices despite intermittent supply tightness

- Scheduled electricity volumes grow much more slowly than market participation

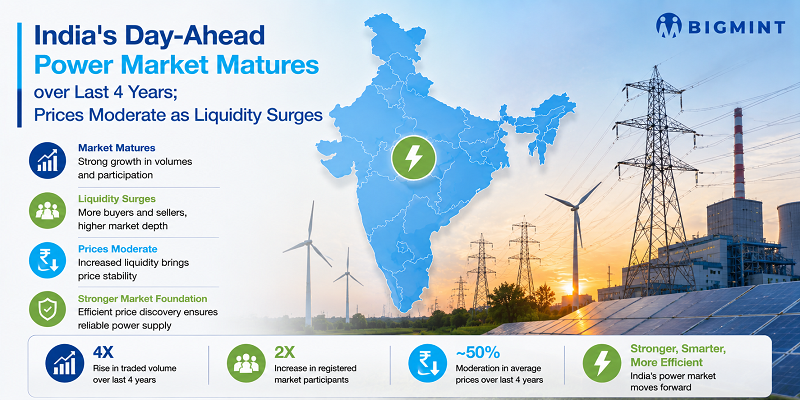

India’s Day-Ahead Market (DAM), a physical electricity trading market on the Indian Energy Exchange, has undergone a significant transformation over the past four years, evolving from a relatively small balancing platform into an increasingly important mechanism for electricity procurement and price discovery.

Between Q2CY’23 and Q2CY’26, purchase bids increased by more than 57%, while sell bids surged by over 83%, reflecting rapidly growing participation by distribution utilities, generators, traders and open-access consumers. However, scheduled volumes increased by only 6.8%, indicating that market participation has expanded much faster than actual electricity traded.

Interestingly, despite record electricity demand and significantly higher market activity, average spot prices have not followed a similar upward trajectory. Instead, the growing availability of renewable generation and improved supply liquidity have moderated average prices, although the market continues to experience occasional scarcity pricing during periods of system tightness.

Taken together, the Q2 data suggest that India’s spot electricity market is becoming deeper, more liquid, and increasingly efficient, while also highlighting the growing complexity of balancing rising demand with an increasingly diversified generation portfolio.

Market liquidity expands rapidly

Perhaps the most striking development over the past four years has been the dramatic expansion in market participation. Purchase bids rose from 23.1 million MWh during Q2CY’23 to 36.4 million MWh during Q2CY’26, while sell bids increased even faster from 24.3 million MWh to 44.6 million MWh.

The substantially faster growth in sell bids suggests that generators are increasingly willing to offer electricity through the Indian Energy Exchange rather than relying solely on long-term bilateral contracts. At the same time, higher purchase bids indicate that distribution companies and large industrial consumers are becoming more comfortable using the spot market to optimise procurement portfolios.

This trend reflects the continuing maturation of India’s organised electricity markets. Rather than serving only as a balancing platform for occasional shortages, the Day-Ahead Market is increasingly being used as an integral part of day-to-day procurement strategy, supported by transparent price discovery and competitive bidding. The exchange itself has also continued to attract broad participation from utilities, generators, traders and commercial consumers.

The growth trajectory also demonstrates increasing confidence among market participants that exchange-based procurement can complement traditional power purchase agreements by providing operational flexibility.

Scheduled volumes grow much more slowly than market participation

Although bidding activity has expanded sharply, actual scheduled electricity has remained remarkably stable. Final scheduled volumes increased only from 12.53 million MWh during Q2CY’23 to 13.38 million MWh during Q2CY’26 — an increase of less than 7%.

This divergence between bids submitted and electricity ultimately scheduled provides one of the most important insights from the data.

The rapidly widening gap suggests that India’s Day-Ahead Market is becoming increasingly competitive. Buyers and sellers are submitting significantly more bids than before, but only a relatively small proportion ultimately clears the market.

Several factors are likely contributing to this trend.

Transmission congestion continues to constrain power flows between regions, preventing some competitively priced electricity from being scheduled. Commercial optimisation by both buyers and sellers also influences bid selection, while the growing diversity of generation sources has increased the complexity of market clearing.

Consequently, the exchange is becoming progressively deeper in terms of liquidity even though physical traded volumes are increasing at a much slower pace.

This is characteristic of more mature electricity markets, where participation expands significantly faster than actual dispatch volumes.

Price behaviour reflects improving supply liquidity

One of the more interesting observations from the four-year comparison is that average market prices have not risen in line with growing electricity demand.

Instead, the market experienced three distinct phases.

During Q2CY’23 and Q2CY’24, average market clearing prices (MCPs) remained elevated at around INR 5,200/MWh, reflecting tighter supply-demand conditions.

In Q2CY’25, prices corrected sharply as average MCP declined to INR 4,409/MWh, driven by improved supply availability, higher renewable generation, and better overall market liquidity.

During Q2CY’26, quarterly average MCP recovered modestly to INR 5,101/MWh, although weighted average prices remained below those prevailing during CY’23 and CY’24.

The monthly data reinforce an important structural trend.

Weighted average prices during Q2CY’26 remained significantly below those recorded in both CY’23 and CY’24 despite substantially higher electricity demand. This indicates that improved supply availability — particularly from renewable generation — has increased competitive pressure within the Day-Ahead Market.

Higher market liquidity has enabled buyers to procure larger volumes of competitively priced electricity, moderating average procurement costs even as electricity consumption has continued to rise.

Scarcity pricing has not disappeared

While average prices have moderated, the market continues to exhibit periods of acute tightness. The quarterly snapshots show that the maximum MCP reached the regulatory ceiling of INR 10,000/MWh during every Q2 between CY’23 and CY’26.

This illustrates an important characteristic of India’s evolving electricity market. For much of the day, abundant supply — particularly from renewable generation — keeps prices relatively competitive.

However, during specific trading blocks when demand strengthens rapidly, renewable output falls, or transmission constraints emerge, prices can still rise sharply and occasionally reach the regulatory cap. The Indian Energy Exchange continues to publish these unconstrained and scheduled market outcomes as part of its daily market data.

The result is a market that increasingly displays two distinct pricing regimes:

- relatively low average prices during periods of comfortable supply; and

- occasional scarcity pricing during short periods of system stress.

Such behaviour is typical of electricity markets with increasing renewable penetration, where average prices decline but price volatility during tight supply conditions can remain elevated.

The market is becoming more efficient rather than more expensive

The four-year evolution of the Day-Ahead Market suggests that India’s spot electricity market is becoming more efficient rather than structurally more expensive.

Demand has increased substantially over the period, yet average weighted prices have generally moderated because improvements in supply availability and renewable integration have strengthened competition among sellers.

Meanwhile, the sharp increase in market participation indicates growing confidence in exchange-based procurement as utilities increasingly optimise purchases between long-term contracts and the spot market.

The combination of higher liquidity, relatively stable scheduled volumes, and lower weighted average prices suggests that the Day-Ahead Market is evolving into a more efficient mechanism for price discovery rather than merely a platform used during periods of power shortages.

Outlook

The next stage of development for India’s Day-Ahead Market is likely to be characterised less by rapid growth in electricity volumes and more by improvements in market efficiency.

As renewable capacity continues to expand, exchange participation is expected to increase further, supported by growing procurement flexibility among utilities and commercial consumers.

At the same time, investments in transmission infrastructure, congestion management, storage technologies and market reforms will become increasingly important in converting the growing pool of bids into higher scheduled volumes.

The Q2 data over the past four years suggest that India’s Day-Ahead Market has entered a period of structural maturity. Liquidity is rising rapidly, competitive price discovery is improving, and the exchange is assuming a progressively larger role in balancing one of the world’s fastest-growing electricity systems. The next phase of evolution will depend not only on additional generation capacity but also on the ability of the market and the grid to efficiently translate increasing liquidity into greater physical electricity trade.

Leave a Reply