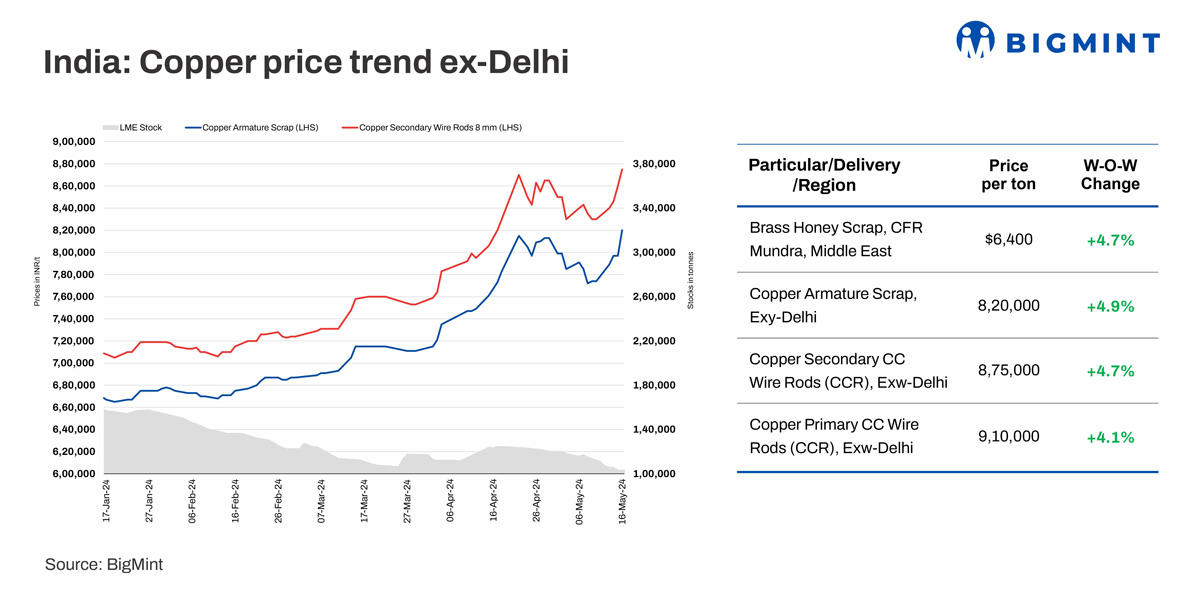

BigMint’s assessment of domestic copper armature prices have been reported at INR 820,000/t, exy-Delhi, rising w-o-w, reflecting an increase of 1.2%. Notably copper prices in the futures market of London Metal Exchange (LME) have hit 2-year high levels i.e. up over $10,300/t levels recently.

Prices of secondary CCR rods (99%) were at INR 875,000/t ex Delhi, rising by 1.7% w-o-w. Meanwhile, primary CC rods were observed at INR 910,000/t, up by 2.2% w-o-w. Imported scrap prices have increased by up to 4.8% w-o-w.

Demand for secondary continuous cast copper rods (CCR) remained robust in the western and northern markets. However, reports suggested that talk scrap is experiencing variations with trades observed at 53- 53.5% of LME prices for USA-origin material to CFR Mundra, and 52-52.5% from Australia to Chennai. Northern-based mills are offered Malaysian talk scrap at approximately $5,350-5,400/t, while UAE-origin talk scrap faced a bid offer disparity of 0.5-0.75%.

Copper motor scrap prices are being offered at $1,300-1,350/t by sellers based in the EU and USA. However, these prices seem to be higher than the bids currently being placed. Notably, buyers from Pakistan and the Far East are placing bids that exceed those from Indian buyers by $60-70/t. This discrepancy highlights a competitive edge for Pakistan, India and Far East buyers in securing copper motor scrap at present rates.

However, buyers remain cautious about importing material due to the high futures prices, preferring to rely on local consumption until the price rally stabilizes.

BigMint’s assessment of USA-origin talk scrap was at $5,425/t, 2.6% w-o-w rise, Middle East origin largely from the UAE prices were recorded at $5,160/t, rise by 2.4% w-o-w.

Global update

In April, China’s copper cathode output was 985,100 t, a decrease of 14,400 t (1.44%) from the previous month, and an increase of 1.56% compared to the same month last year. From January to April, the cumulative output was 3.9047 million t, an increase of 222,200 t (6.03%) y-o-y. The reason for the m-o-m decline in output in April was that seven smelters underwent maintenance, as per latest reports.

In May, more smelters are scheduled for maintenance. Around eight smelters will undergo maintenance, affecting 1.64 mnt of smelting capacity. This will be the primary reason for the production decline expected in May 2024 which may lead to price hike in near term.

Recent offers, deals for the week

Australia Copper cables High grade traded at 94% LME CIF Chennai.

Australia Medium grade copper cables was at 92% LME CIF Chennai.

Australia low grade copper cables was at 88% LME CIF Chennai.

Brass honey Australia 2% was 62% LME CIF Chennai.

Australia talk sold to CIF Chennai at 52.5% LME.

Copper motors mix From UK was sold at $1,320/t CIF Nhava Sheva.

Cu motors mix from EU traded at $1,290/t yesterday to CIF Nhava Sheva.

EU origin Cu motors mix was traded at $1,270 to 1,275/t CIF Pakistan recently.