- South African offers rise while Indian buyers remain highly selective

- Domestic mid-CV coal stays tight, supporting firm auction participation

India’s imports of seaborne thermal coal has slowed 6% y-o-y to 151.7 million tonnes in the first 11 months of CY 2025, amid low prices of domestic coal and low consumption by the thermal power sector. Buyers are resisting firm seaborne offers, especially for South African RB2/RB3 and Indonesian mid/low CV:

- Indian interest in South African RB5500 is increasingly price-sensitive, with many buyers preferring to wait out current CFR/FOB levels rather than chase tonnage.

- Portside RB 5,500 NAR has edged up at key east-coast ports, but the response from end-users has been selective restocking, not a broad-based buying wave.

South African coal offers rise further as sellers hold stocks for higher levels

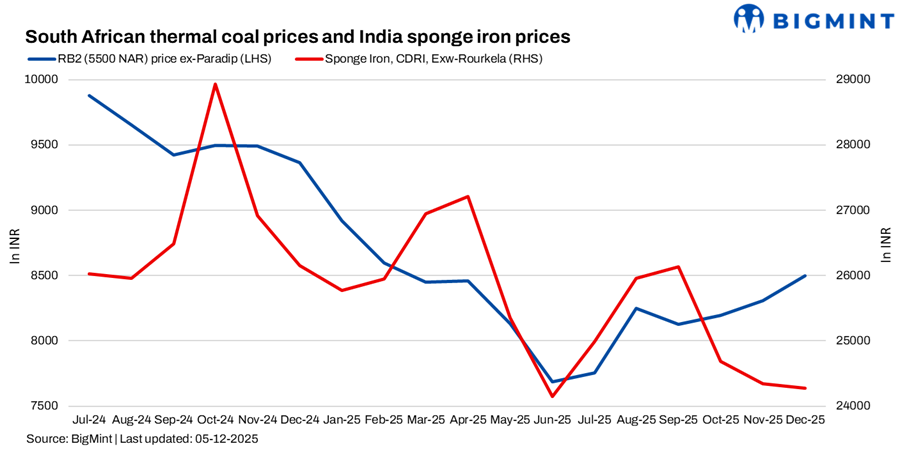

South African thermal coal offers increased w-o-w across Indian ports, supported by stronger indices, firm seaborne prices, and tightening freight. Ex-Paradip RB2 rose to INR 8,800/t and RB3 to INR 7,400/t. At Gangavaram, RB2 increased to INR 8,700/t and RB3 to INR 7,300/t, while Vizag RB2 moved up to INR 8,650/t and RB3 to INR 7,300/t – a broad gain of INR 100-400/t.

Some sellers withheld stock in anticipation of further hikes, with expectations of continued firm offers through Feb amid vessel shortages for Jan-Mar deliveries. A 5,000 t deal was concluded at INR 8,700/t ex-Mangalore, while another 5,000 t of RB2 coal was booked at INR 8,400/t ex-Mangalore. Export offers also strengthened, with RB2 rising to $76/t and RB3 to $60.5/t, up $1-2 w-o-w.

Behind this caution lies a different Indian fuel mix story:

Industrial consumers in cement, sponge iron and metals are leaning harder on domestic mid- and high-CV coal where they can secure it, rather than paying up for imported alternatives that are inflated by freight and a weaker rupee.

The recent SECL auction underlines this preference. Mid- and high-CV grades (G6-G9) cleared with strong premiums to notified prices, and the auction saw near-full uptake. Cement, aluminium and sponge iron units aggressively booked 5,200-5,500 kcal/kg NAR material, signalling that domestic mid-CV coal remains fundamentally tight, even as imported low-CV cargoes struggle to clear.

High-CV: supported, but support is fragile

At the top of the quality stack, the tone is neutral to mildly positive rather than outright bullish.

- FOB NEWC 6,000 NAR is assessed around the high-$100s/t. The physical market shows bids roughly in the $104.50-109/t area and offers stretching up toward $115/t, with an occasional outlier trade at $110/t.

- The presence of deep index-discount bids (index -$6 to -$8) and persistent $8-10/t bid-offer gaps tells you that buyers are not convinced by any strong upside story and are preparing for softer index prints.

- In South Africa, RB 6,000 FOB around the low-$90s is being held up by tight rail/terminal logistics and recent Korean purchases, while RB 5,700 at ~$89/t and RB 5,500 at ~$76/t are broadly flat and aligned with global mid-CV weakness.

High-CV coal is therefore outperforming low-CV, but its strength is relative, not absolute. Support rests on logistics, grade preference and Atlantic pull, rather than on booming underlying demand.

Outlook

For the seaborne market, India is bearish on imported volume but bullish on quality. It is not absorbing surplus Indonesian or RB low/mid-CV cargoes, but it is bidding up the domestic grades that best fit its industrial and captive power needs.

Leave a Reply