- Tight US refinery output, Middle East disruption support global prices

- Indian buyers resist high offers, switching to cheaper thermal coal

Record-high US Gulf assessments, supply disruptions from the Middle East, and a widening premium over thermal coal are forcing industrial buyers to rethink their fuel strategy.

Scarcity and resistance

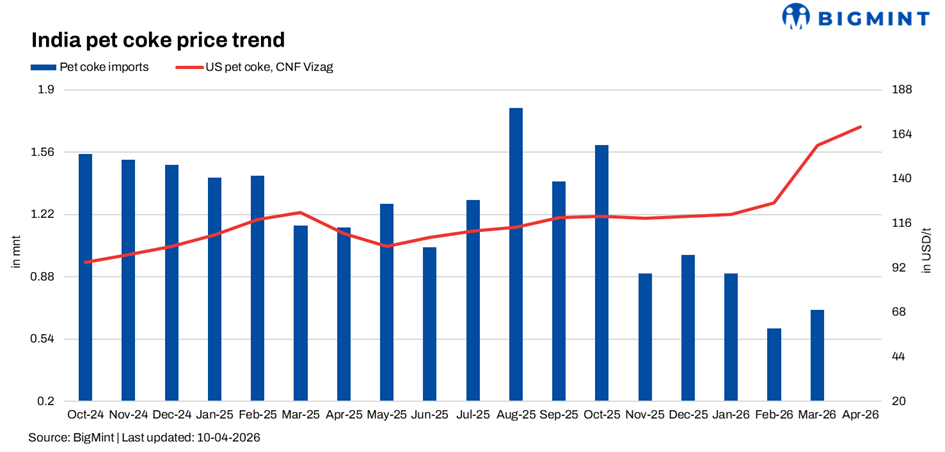

The global petroleum coke market entered April 2026 in a state of unusual tension. On one side, supply constraints and geopolitical disruptions have pushed prices to levels not seen in three years. On the other, end-users particularly in India are refusing to follow, choosing instead to switch fuels or walk away entirely. The result is a market that is technically strong but fundamentally fragile. Sellers are holding firm. Buyers are holding back. And the gap between offers and bids has become unusually wide.

Global petcoke price table (as of early April 2026)

Is tight supply here to stay?

US refiners are operating in a changed environment. Refinery output in the first quarter of 2026 was on the lower side, keeping petcoke supply tight. Permanent refinery closures on the West Coast have reduced overall coke production capacity. Maintenance turnarounds at key Gulf

Coast refineries have limited spot availability. And a shift toward lighter crude slates at some refineries has reduced petcoke yields.

Looking ahead, some traders expect supply to improve. Higher crude prices and wider heavy-light spreads could incentivize refiners to process more heavy sour crude, which produces more petcoke. Additionally, the Middle East conflict could prompt the US to ramp up oil production, increasing petcoke availability. But for now, the message from refiners is consistent: spot cargoes are limited, and there is little urgency to discount.

End-users are saying: Enough is enough

The response from Indian cement manufacturers has been one of firm resistance. One India-based producer explained that with prevailing offer levels, petcoke is not economically viable. The company has shifted entirely to coal. Numerous smaller cement producers have also moved away from petcoke.

The economics is stark. CFR India 5,500 NAR thermal coal was available at around $103-105/t, while petcoke was being offered at $160/t. Even adjusting for calorific value, the premium has become too large to justify. Cement manufacturers are struggling to pass on higher costs to customers, squeezing margins. One buyer noted that offers in the mid-$150s were still too high, with expectations of a correction during April.

Some cement plants have switched to US thermal coal instead. One buyer reported shifting to US coal, which was cheaper by about $15/t compared to petcoke. US Northern Appalachian coal with 6,900 kcal/kg NAR is the preferred alternative due to its high calorific value and sulfur content. Others are relying on domestic coal, using G8-G9 grade material from Singareni.

Market waiting for a trigger

Traders are caught in the middle. They see the supply constraints and rising freight that justify higher prices, but they also see buyers walking away. Offers for US-origin petcoke to India were in the range of $158-160/t CFR for April and May loading cargoes. But bids were coming in at $150-152/t, and sometimes lower. The gap has persisted for weeks, and only a handful of deals have been heard.

Some traders with imminent laycans have reduced offers to entice buyers, but the response has been limited. Buyers are holding steady on their price expectations and actively seeking alternative options. There is a sense that the recent run-up may have been overdone. One participant noted that previous high levels were completely hypothetical, creating a non-tradable market. The correction, when it comes, could be sharp.

Freight factor

Freight rates have become a critical component of delivered prices. The Supramax rate from Houston to Krishnapatnam on India’s east coast rose to $50.50/t, up 75 cents on the week and marking the second consecutive week of increases. Rising freight has made US-origin material even more expensive for Indian buyers. Some traders noted that suppliers preferred selling into Europe, where netbacks were better than what Indian buyers were willing to pay.

Middle East disruption

The war in the Middle East has disrupted high-sulfur petcoke flows from major suppliers such as Saudi Arabia and Oman. The effective closure of the Strait of Hormuz brought shipments to a halt, and even with a ceasefire, vessel movements remain limited. An estimated 800 vessels with 20,000 seafarers remain blocked. While some LNG and crude movements have resumed, petcoke flows will take longer to normalize. Insurance premiums remain elevated, and shipowners are waiting for clarity on security arrangements. US petcoke refineries have stepped in to fill the gap, but at a $40-50/t pemium over thermal coal on a delivered basis.

Growing threat to petcoke demand

The most significant development in India is the accelerating shift away from petcoke toward thermal coal. The price comparison is telling: CFR India East 5,500 NAR thermal coal at $103/t versus $160/t for 6.5% sulfur petcoke. One buyer has completely shifted to coal and is not considering petcoke. Another reported that numerous smaller cement producers have also moved away. This shift is not limited to petcoke. Some cement plants are also moving away from expensive US thermal coal, switching to Russian, South African, or domestic alternatives. Indian industrial consumers are price-sensitive and technically capable of switching fuels when economics dictate.

Outlook

The near-term outlook depends on three factors. First, the duration of the US-Iran ceasefire. If it holds and shipping normalises, Middle Eastern petcoke could return, increasing supply and putting downward pressure on prices. Second, the behaviour of Indian cement buyers. If they continue to resist current levels and persist with coal switching, sellers may be forced to lower offers to clear inventories. Third, refinery output in the US. If heavy crude runs increase, petcoke supply could improve, easing the tightness that has supported the rally.

For now, the market is in a holding pattern. Sellers are holding firm, pointing to supply constraints and high freight. Buyers are holding back, pointing to cheaper alternatives and margin pressure. Which side blinks first will determine the direction of petcoke prices for the rest of the second quarter.

Leave a Reply