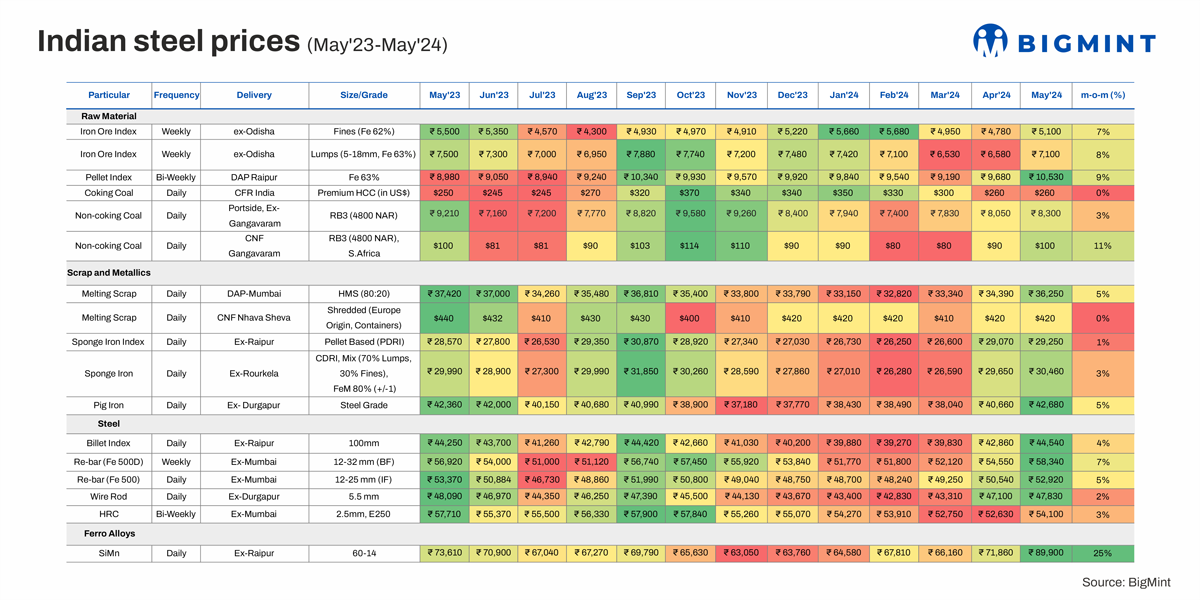

All steel and raw material prices up-trended m-o-m in May, 2024 as the supply-demand imbalance was restored after mills went ahead with production cuts. Imported South African coal rose by 11%, followed by pellets, at 9%. Imported scrap remained flat m-o-m. Finished steel prices may see a further uptick in June although there is a question mark on whether these will get absorbed in the market. In raw materials, Australian coking coal prices are expected to be in a narrow range amid constraint for July laycan cargoes accompanied by falling demand. Also, the met coke safeguard directive keeps buyers uncertain on whether the import restrictions will be imposed or annulled. On the other hand, metallics like sponge, scrap, and iron ore may see an uptrend as finished steel demand is expected to remain good post-election results and inventory depletion.