- Steel prices show sustained decline in Oct’25

- Iron ore prices remain firm amid supply concerns

- Coking coal edges up slightly on strong China cues

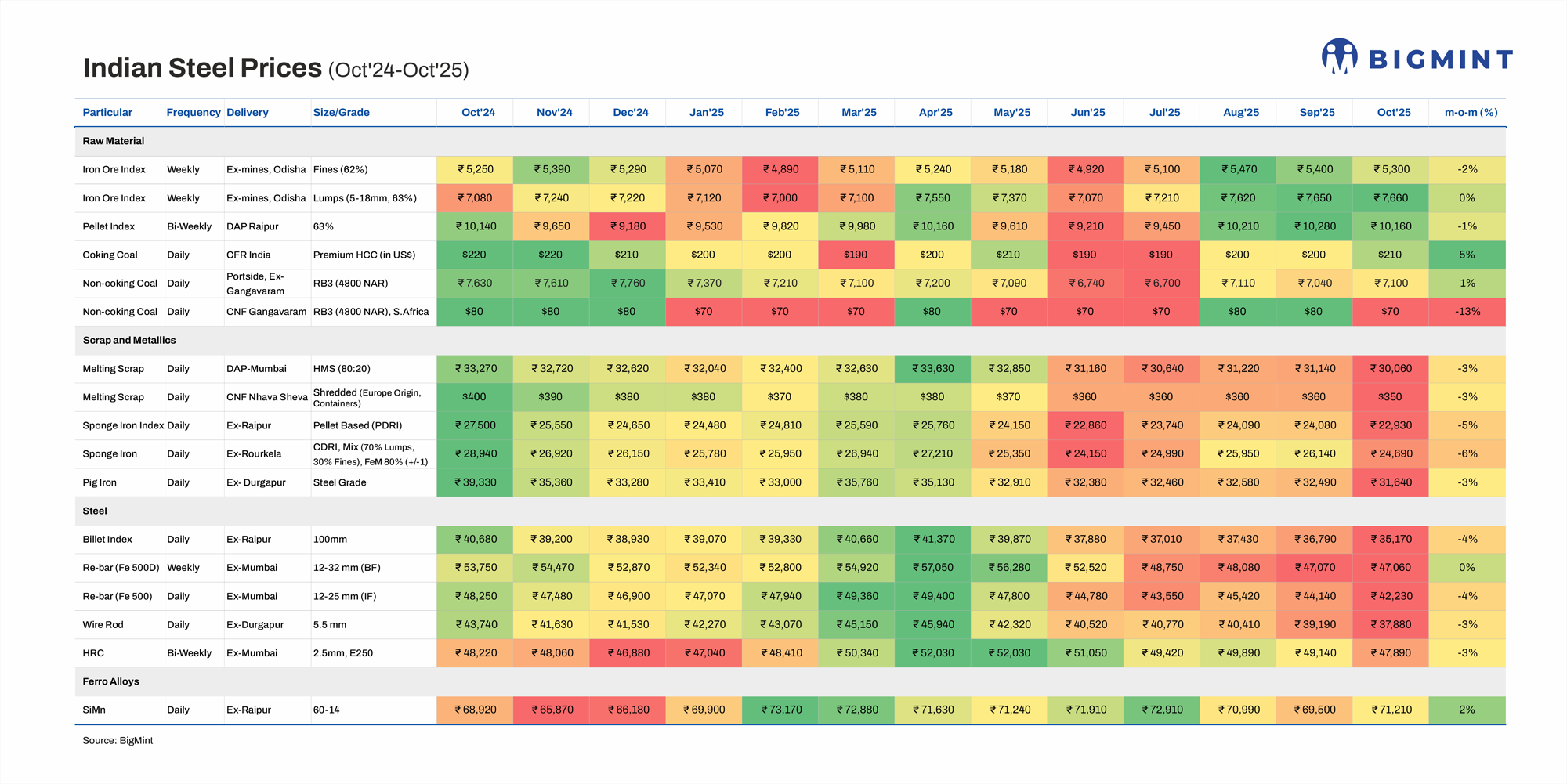

Morning Brief: The Indian steel market continued to weaken further in October 2025, with steel and metallics prices declining m-o-m even against the stagnant levels witnessed in September. The sustained decline in steel prices happened at a time when iron ore and coking coal prices have remained relatively firm, thereby piling pressure on producers.

The Tier-1 mills had reduced list prices of HRC and CRC in early October and inventory pressure both at the trade level and in mills increased due to subdued activity during the festive period. A slight post-festive rebound has been seen in the longs segment; however, flat steel prices continue to weaken amid muted sentiments and the decline in global steel prices. Domestic prices are at 5-year lows and the bottom is still not in sight.

Price movements in Oct’25

Iron ore & pellets: BigMint’s Odisha iron ore assessments for fines and lumps showed relative stability m-o-m, with fines decreasing marginally and lumps remaining firm. With the monsoon finally receding, availability increased. However, India’s iron ore production increased by just 0.7% y-o-y in H1FY’26, while crude steel production rose more than 12% in H1. Weak steel market conditions, non-operationalisation of auctioned mines, surrender of auctioned mines by leading players impacted production.

Despite limited spot transactions, prices have held steady due to the restricted availability of material in the open market. Supplies from smaller private miners are limited at present. Even though buyers are cautious, the shortage of ready stock is preventing any major price correction.

BigMint’s pellet index for Raipur, PELLEX, dropped marginally in October tracking weak sentiments in the semis and metallics segments. India’s pellet production edged up by 5% on the year in H1 of this fiscal, with new investments being announced in eastern and central India. Therefore, higher supplies are likely to weigh on prices.

Coking Coal: BigMint’s CFR India index for hard premium coking coal showed a marginal uptick of 5% m-o-m in August due to the hike in offers from Australia following higher prices fetched in the Chinese market. The Chinese market for met coke witnessed its second straight round of price hike recently in response to tight supply and resilient demand. Therefore, Indian buyers have been obliged to accept higher prices.

Non-coking coal: Post-festive sluggishness and cyclone-related disruptions along the east coast have kept trade activity muted. India’s sponge iron output dropped to a 7-month low of 4.71 mnt in September reflecting production curtailment due to weaker end-user consumption and reduced coal intake. Portside stocks also increased in end-October. So, prices have been under pressure.

Melting scrap: Steel prices are at a five-year low, and narrowing steelmaking conversion margins are adding to the pressure. As a result, secondary steelmakers are cutting production, but mills continue to incur losses. This has impacted scrap demand and prices. Alternative feedstock (such as sponge iron) and semi-finished steel prices have been on a downtrend affecting scrap prices. In the Mumbai market, trading was muted during the Diwali holidays. Limited demand, weak liquidity, and cash flow constraints kept buying restricted to fulfilling urgent needs.

The imported ferrous scrap market remained subdued as trading stayed limited amid a wide bid-offer gap and weak domestic steel sentiments. Scrap imports increased by just 4% y-o-y in H1. Mills avoided fresh bookings due to weak steel demand and falling DRI prices as well as competitive offers at home.

Metallics: With steel prices at 5-year lows, sponge and pig iron prices trended down in October. Average sponge iron prices declined by 5-6% m-o-m and production curtailments were reported amid increasing economic unviability due to firm raw material prices. Prices at pig iron auctions decreased amid the overall decrease in steel prices.

Billet: BigMint’s billet index dropped an average 4% m-o-m in October on limited trading during the festive season and weak steel prices impacting margins. In Raipur, prices were under pressure due to negative cues from neighbouring markets and persistent weakness in finished steel demand which restricted any meaningful recovery in trades.

Rebar: The primary mills increased rebar prices by up to INR 1,000/t $11/t) for early-October deliveries as against levels prevailing in end-September. However, prices in the IF steel market fell in the range of INR 200-1,000/t across regions in mid-October. Finished long steel prices fell on selling pressure due to high inventory levels and subdued demand. Trade-level BF rebar prices declined in mid-October. The major primary mills either offered discounts or reduced list prices due to subdued sentiment ahead of Diwali.

Trade prices edged down across major markets in end-October as some primary mills either increased their discounts or reduced list prices owing to subdued market sentiments after Diwali. Inventories at mills rose slightly by around 15% in end-October, compared with levels seen at the beginning of the month.

Wire rod: Wiire rod prices neared five-year lows in October amid sluggish buying inquiries. In the induction furnace (IF) segment, prices witnessed a monthly average decrease of INR 1,300/tonne (t) ($15/t) m-o-m to INR 37,900/t ($427/t) exw-Durgapur as compared to September levels, the lowest since November 2020. Prices sunk due to weak steel prices and construction activity and market uncertainty.

HRC: The leading steel manufacturers decreased prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-17/t) for October sales as compared to the list prices of early-September in the first week. The market remained sluggish as slow demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings.

Thin margins, heavy stocks, and the Navratri and Durga Puja holidays further dampened trading activity. HRC trade prices edged lower in the last week of October due to demand staying subdued amid limited trading interest.

Silico manganese: Domestic silico prices edged up marginally due to limited spot material availability as exports from India hit all time high in Aug’25. The tight supply in domestic alloys market has created a supply dearth which is keeping prices supported.

Outlook

Domestic steel prices will most likely remain rangebound in the near term, with a slight rebound likely. Flat steel export offers may stay under pressure in the short term, driven by cautious market sentiment and the approaching CBAM. This will be a drag on domestic prices too. Liquidity constraints and uncertain market conditions may limit demand amid softening global prices.

In the longs segment, the post-Diwali resurgence in market momentum and expectations of a pickup in infrastructure and construction activities will drive steel demand and trade. Market participants are largely in a wait-and-watch mode. The upcoming monthly price revisions expected to be announced by the leading mills will guide sentiment and set the trajectory for the domestic market.

Raw materials prices, on the other hand, are expected to remain firm with supply concerns resurfacing amid the rapid surge in steel output.

Leave a Reply