- Exports to EU increase y-o-y but slow sharply from H2CY’25

- Indian steel imports fall further as safeguard duty curbs HRC inflows

- Middle East conflict halts export activity in Mar, sharp m-o-m fall likely

Morning Brief: India’s steel exports (including stainless steel) rose 45% y-o-y to 1.68 million tonnes (mnt) in January-February 2026, as steelmakers shipped higher volumes to Vietnam and the UAE to compensate for weaker demand from the EU.

The uptrend reflects sustained momentum from the second half of 2025, when exports had surged to a four-year peak. This was due to EU buyers frontloading purchases ahead of the definitive start of the Carbon Border Adjustment Mechanism (CBAM) on 1 January 2026.

However, the y-o-y rise in exports is also accentuated by weak trade flows in early 2025. Exports in H1CY’25 were subdued, affected by global oversupply, Chinese competition, and cautious buyer sentiment due to anti-dumping investigations in the EU and Vietnam.

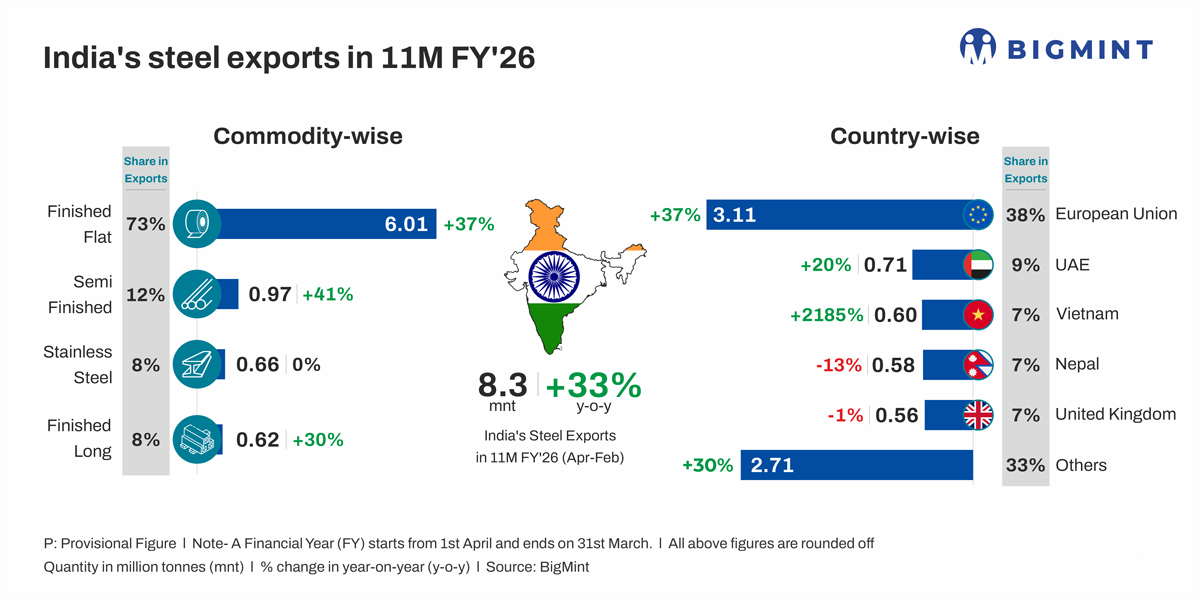

Meanwhile, in 11MFY’26 (April 2025-February 2026), exports totalled 8.27 mnt, higher by 33% y-o-y.

Factors influencing Indian steel exports in Jan-Feb’26

Exports to EU rise but pace of growth slows: The EU remained the primary destination for Indian steel exporters in January-February, recording an 11% uptick y-o-y. However, there was a marked slowdown from the strong momentum seen in H2 of 2025: the around 200,000-tonne (t) average recorded in January-February 2026 is much lower than the 335,000 t average during July-December.

The pullback reflected caution among buyers after CBAM entered its definitive phase, with uncertainty over the carbon costs they would ultimately need to absorb. This reduced the urgency that had driven restocking in the second half of 2025. Moreover, expectations of a sharp reduction in safeguard quotas kept buyers on the sidelines.

In January, the European Commission reportedly approved the new EU steel safeguard mechanism proposed to replace the framework that has been in place since 2018 and is due to expire on 30 June 2026. This includes a 47% reduction in tariff-free import quotas and the introduction of a 50% ad valorem duty on volumes exceeding the revised limits.

Meanwhile, Indian mills exhausted their allocated HRC quota for Q1CY’26 in mid-January, indicating a strong export push at the start of the year before demand eased as per expectations.

Exporters shift focus to Vietnam, UAE: With EU demand slowing, Indian mills increased shipments to Vietnam (up manifold) and the UAE (rising 62%).

Exports to Vietnam recovered after Indian HRCs were cleared of anti-dumping concerns. At the same time, reduced Chinese presence in the market due to anti-dumping measures helped Indian suppliers gain market share. In January, Vietnam’s imports from China were 31% lower y-o-y at 1 mnt, while Japanese ones were down 33% at 0.26 mnt.

Shipments to the UAE also rose, supported by steady demand. Competitive pricing improved the viability of exports to the UAE. In December 2025, both Indian and Chinese export offers averaged $468/t FOB.

Notably, while Vietnam and the UAE emerged as alternative outlets, their capacity to absorb material remains limited compared with the EU. As a result, overall export levels may prove difficult to sustain if European demand remains subdued, other markets do not scale up intake further, and Chinese exporters ramp up export efforts.

Imports decline on policy oversight

India’s imports (including stainless steel) declined 17% y-o-y to 1.27 mnt during January-February 2026, extending the broader downtrend seen since April of last year. In 11MFY’26, imports totalled 8.66 mnt, lower by 12% y-o-y.

HRC imports were down by 25% y-o-y in January-February. Trade barriers were the primary driver, including the safeguard duty on flat steel imports and anti-dumping duties on Vietnamese flat steel.

The spread between domestic and imported HRC prices (that is, landed costs after incorporating the safeguard duty) narrowed to around INR 2,000/t as of early March compared to INR 12,000/t in December 2025, as Indian mills undertook consecutive price hikes to manage raw material cost pressures. Despite domestic material’s shrinking price advantage, import offers were limited throughout January-February.

Sharp falls in imports from South Korea and Japan were also observed, though these were offset by a modest rise in Chinese imports.

Outlook

BigMint expects exports to drop sharply in March as the escalating US-Iran conflict has caused severe logistical bottlenecks and surging shipping costs. The impact is significant given that Saudi Arabia and the UAE together accounted for around 10% of India’s total steel exports in 2025.

The disruption comes at a time when exporters had been relying on increased shipments to the UAE to offset weakening demand from Europe. In fact, the UAE’s share in India’s total exports increased to nearly 15% in January-February following the surge in shipments.

The impact is not confined to the Middle East, with spillover effects visible in Europe-bound shipments as well. A growing number of vessels are avoiding the Red Sea-Suez Canal route, opting instead for longer voyages via the Cape of Good Hope. This has extended transit times by around 15-20 days, disrupted delivery schedules, and sharply increased freight and insurance costs, reducing the competitiveness of Indian exports to Europe. The logistical challenges add to existing pressures from regulatory changes and quota limitations in the EU, further weighing on export prospects.

Meanwhile, imports could increase if the conflict drags on. Indian steelmakers are facing rising raw material costs due to tight supply, and production cuts may be in store if material shortages continue and energy costs surge. As such, Indian buyers could procure more volumes from overseas, especially cheap Chinese material, despite rising shipping costs. The India-China route is not affected by the conflict in the Middle East, and rising domestic prices may make Chinese material more cost competitive. China’s export opportunities have also turned limited, as shipments to the Middle East accounted for roughly 20% of its exports. Consequently, China may redirect surplus volumes towards India as Middle East demand weakens.

Beyond the immediate impact of the war in the Middle East, exports to the EU are likely fall significantly from June due to the nearly 50% cut in safeguard quotas. The outlook for Indian exports for 2026 remains subdued unless mills branch out to new markets.

Leave a Reply