- Prices drop to lowest level since pandemic amid domestic overcapacity

- Decline in coal and raw material prices impact sponge iron prices

- Near-term outlook dim amid deteriorating steel market sentiment

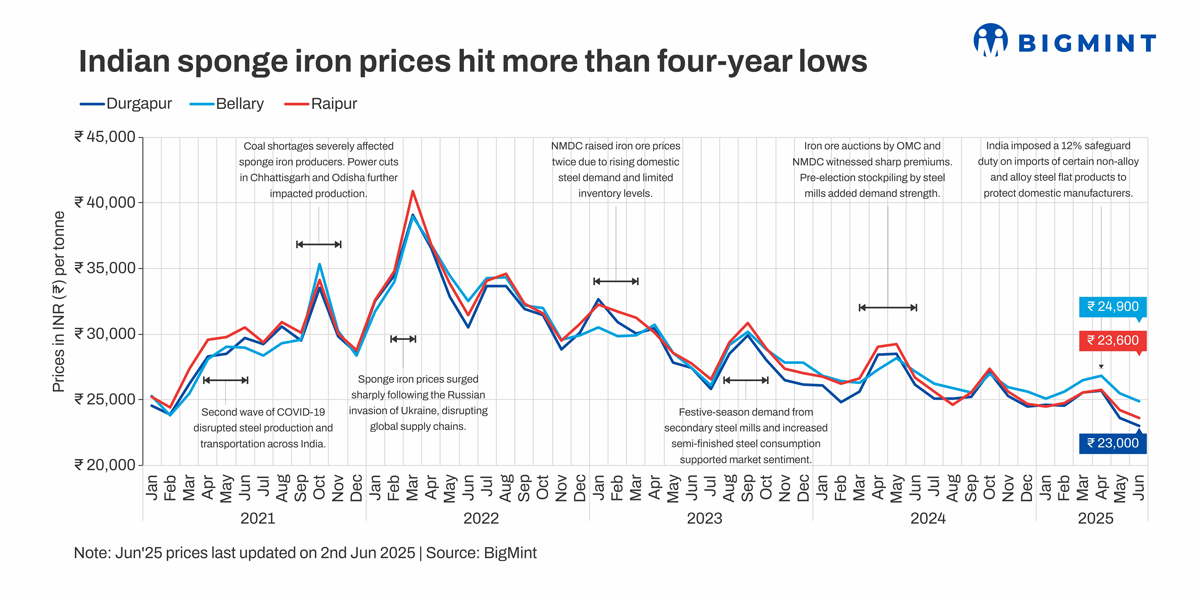

Morning Brief: In what appears to be a significant decline, sponge iron (direct reduced iron) prices in India tumbled to a 52-month low in major steel and metallic production hubs across the country in May 2025, as per latest data collated by BigMint. This shows an extreme level of pressure on domestic sponge iron prices amid struggling steel market sentiment; in fact, prices have dropped to lows last seen during the pandemic years.

In India’s key sponge iron production hubs of Raipur, Durgapur and Bellary in central, eastern, and southern India, respectively, prices dropped to levels last witnessed in February 2021. The monthly average price of pellet-based DRI (PDRI) declined by INR 1,450-2,400/t in major hubs like Raipur and Durgapur in May. Out of India’s total crude steel production of 152 million tonnes (mnt) in FY’25, sponge iron had roughly a share of 30%.

Why prices dropped to multi-year lows?

Rapid capacity growth outstrips consumption: Domestic sponge iron production capacity has grown manifold over the last few years, with production reaching around 55-56 mnt in FY’25. Capacity is estimated at around 68-70 mnt. The share of coal-based sponge iron production in India is over 80%.

The growth in induction furnace-based steel production has been sustained through the increase in sponge iron output. On the other hand, India’s pellet production touched a new record of 105 mnt in FY’25, which sustained the DRI market – around 63% of India’s sponge iron production is based on iron pellets.

Although domestic steel consumption growth has been rapid (touching around 144-145 mnt in FY’25), the ongoing scenario of global uncertainty and deterioration in steel prices, coupled with growing overcapacity in the domestic sponge iron sector, weighs on prices. After increases in late March, sponge iron prices fell in major markets from April to May due to inventory pressure amid subdued demand for downstream products – billets and finished steel.

Notably, lower prices results in lower working capital, which meant that either DRI kilns are operating at higher capacity or idle plants may have started production.

Weakening coal prices: Data show that domestic coal prices softened from high levels of around INR 7,000-10,000/t through much of 2022-2023 to fall below INR 5,000/t exw-Bilaspur, as per BigMint, on 31 May. Similarly, imported South African RB2 coal (5500 NAR) prices dropped from levels higher than INR 10,000/t in end-2023 to below INR 8,000/t ex-Paradip in end-May 2025. Reduced domestic and imported coal prices helped sponge iron producers slash costs and also impacted prices.

Deteriorating economics of production: The superior economics and sustained profitability of the domestic sponge iron sector has driven capacity growth, thanks to sufficient iron ore availability, easing domestic coal supplies, moderation in imported coal prices from the elevated levels seen in 2022-23, as well as volatility of imported ferrous scrap prices. Iron ore fines, pellets, and coal are the core cost drivers in sponge iron production, accounting for 60–70% of the total cost.

Moreover, domestic producers operating medium to large kilns have the advantage of installing waste heat recovery boilers (WHRB) for power production, thereby enhancing financial benefit through recycling of waste heat.

Moreover, domestic producers operating medium to large kilns have the advantage of installing waste heat recovery boilers (WHRB) for power production, thereby enhancing financial benefit through recycling of waste heat.But the superior economics of sponge iron production is now threatened by the abrupt downtrend in prices. BigMint assessment shows that the conversion spread from PDRI to billets dropped in Raipur by 4% in May, signaling reduced profitability for sponge iron-based billet manufacturers. In Durgapur, spreads remained relatively stable but narrowed slightly compared to April. At the same time, domestic production of sponge iron increased by 7% y-o-y in January-May 2025 to around 21 mnt. So, oversupply seems to be weighing on domestic prices.

Softening exports: After a robust showing in 2024, sponge iron exports to Nepal and Bangladesh remained muted in 2025. Export volumes in April and May 2025 fell by over 30% y-o-y, impacted by declining prices and sluggish finished steel demand in neighbouring markets. Buyers remained cautious amid sufficient local availability of semi-finished steel, reducing their reliance on Indian sponge iron.

Therefore, channeling of surplus production to the export markets has been rendered unfeasible, thereby further pressuring prices.

Outlook

Any noticeable uptick in domestic steel prices currently looks unlikely, with the advent of monsoon in different parts of the country impacting construction activity. Amid global trade uncertainty and decline in export prices of the major counties, a rebound in steel prices looks unlikely.

Sponge iron prices declined 4-5% m-o-m across key eastern and central Indian markets in May. With declining iron ore and coal prices globally and subdued finished steel offtake, the near-term outlook suggests continued pressure on prices. Weaker exports and narrowing conversion spreads may impact sponge iron production volumes in the coming months.

Leave a Reply