- Crude steel production shows mixed trends y-o-y

- Sharp decline in steel prices drags down EBITDA/t

- PAT sinks, JSW Steel hardest hit with 43% fall y-o-y

Morning Brief: Amid bearish market trends, Indian Tier 1 mills witnessed a downbeat FY’25, with EBITDA/tonne (t) falling by 8-23%. This decline came in the wake of lower steel prices, though there was a slight uptick in sales y-o-y in alignment with the increase in India’s steel consumption. Meanwhile, crude steel production presented contrasting trends y-o-y.

Production sees mixed performance

While India’s crude steel output climbed up by 6% y-o-y in FY’25, Tier-1 mills’ production volumes showed varying trends y-o-y.

JSW Steel (standalone) took the lead among primary mills, recording its highest-ever annual output. However, y-o-y, crude steel production inched up a minor 1% to 22.47 million tonnes (mnt). Capacity utilisation was at 91% last fiscal, and production volumes were boosted by the ongoing expansion of the Vijayanagar steel works, where a new blast furnace (BF) and steel melting shop (SMS) were commissioned.

Tata Steel also recorded its highest-ever output of 21.68 mnt in FY’25, up by 4.3% y-o-y. Notably, the company commissioned India’s largest blast furnace at Kalinganagar, increasing the total capacity at the site from 3 to 8 mnt/year. Additionally, efforts are underway to scale up production units at Kalinganagar, Ludhiana, and Jamshedpur.

SAIL’s output dipped a slight 0.3% y-o-y to 19.19 mnt, while JSP clocked a modest 2.4% growth to 8.12 mnt. JSP increased its capacity utilisation to 85% in FY’25 from 83% in FY’24, driven by operational improvements.

AM/NS India’s output declined 5.7% y-o-y to 7.2 mnt. Production was likely impacted by the closure of AM/NS’s Corex-2 plant, following a fatal accident.

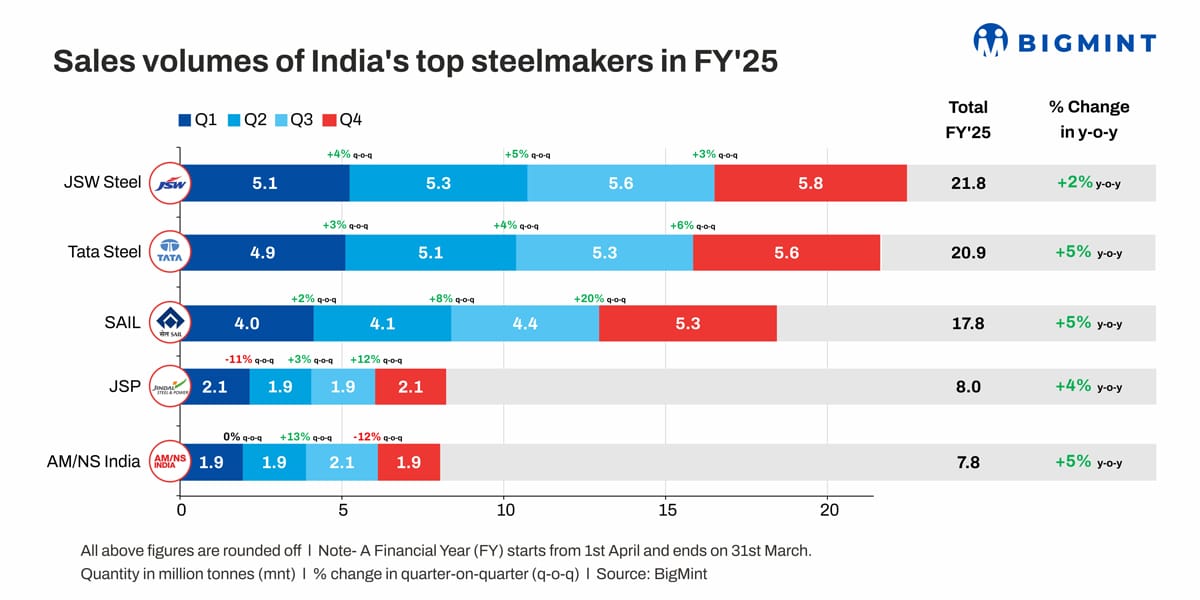

Sales volumes edge up y-o-y on strong domestic trade

All five steel producers were able to lift sales volumes y-o-y, though the rise was modest, ranging within 2.4-5.2%. Domestic sales were a key driver of the rise in volumes, but export performance was largely poor, given a lacklustre global market.

JSW Steel’s consolidated India operations registered a 15% y-o-y climb in domestic sales in FY’25, while exports plunged 39% y-o-y.

Conversely, Tata Steel, which saw the highest percentage growth among the Tier 1 mills, was able to lift its exports by 20% to 1.2 mnt in FY’25. Domestic sales grew a modest 4% to 19.7 mnt. Among end-user sectors, Tata Steel witnessed notable growth in the retail (targeted to individual house builders), construction and infrastructure, and consumer durables and packaging segments. Tata Tiscon also achieved its best-ever sales volumes with 19% y-o-y growth to 2.4 mnt.

At SAIL, volumes edged up by 4.7%, aligned with the increase in domestic consumption.

JSP’s domestic sales increased by 7% y-o-y, while exports plummeted 29% in FY’25, with the latter’s share in total sales volumes slipping to 6% from 9% in the previous fiscal. Interestingly, the share of flat products in overall figures also increased to 43% from 32% in FY’24, indicating robust demand.

Meanwhile, AM/NS India recorded sales growth of 4.9% to 7.8 mnt.

EBIDTA tumbles amid falling steel, raw material prices

All mills posted a fall in their earnings before interest, taxes, and depreciation and amortisation (EBIDTA), with JSW Steel recording the steepest fall of 23% y-o-y. Only SAIL was able to contain the fall to a single-digit 8%.

The sharp decline in flat steel prices was the key contributor to the drop in EBITDA/t. In the trade segment, hot-rolled coil (HRC) prices lost 11% to INR 50,030/t ($584/t) ex-Mumbai in FY’25 from INR 56,000/t ($653/t) amid weak demand, following the massive influx of cheap imports.

Meanwhile, blast furnace (BF) rebars fared better, with a mere 1% dip to INR 53,780/t ($628/t) from INR 54,300/t ($634/t) in FY’24.

The erosion in iron ore prices also led to lower steel tags. The Fe62% Odisha iron ore index fell 4% to INR 4,940/t ($58/t) in FY’25 from INR 5,150/t ($60/t) in FY’24, given the downtrend in the steel market and increased production.

Additionally, prices of premium hard coking coal from Australia increased 5% y-o-y to $230/t CFR. Given weak demand and price resistance, it was difficult to pass on these costs to end-users, which ultimately led to further contraction of the mills’ EBITDA/t.

In conjunction with the drop in EBITDA, profit after tax (PAT) also fell for all mills. JSW Steel’s PAT plunged 43% to INR 5,245 crore ($612 million), and JSP’s was down by 29% to INR 4,248 crore ($496 million). SAIL registered a 21% drop to INR 2,148 crore ($251 million), while Tata Steel’s PAT fell a relatively minor 6% to INR 13,803 crore ($1.6 billion).

Outlook

Despite the grim performance in FY’25, there seems to be some optimism regarding the ongoing fiscal. For instance, JSW Steel projects a demand growth of 8-10% in FY’26, amid a strong capex push by the government. SAIL also expects favourable policies and infrastructure growth to support domestic steel demand. Both steelmakers have also alluded to the positive impact of the safeguard duty, which has played a crucial role in slowing down steel imports.

However, going by current market trends, it is uncertain whether there will be bullish momentum throughout the year. Presently, steel prices have been on a steady downtrend, battered by global steel industry downtrend, trade uncertainty, weak prices in major steel exporting countries, soft domestic demand, and liquidity woes. The outlook for the near future is clouded, though there is hope that demand will pick up in the long term.

Leave a Reply