- Evening prices spike repeatedly as solar drops off

- Southern plants hold less than 40% of normative stocks

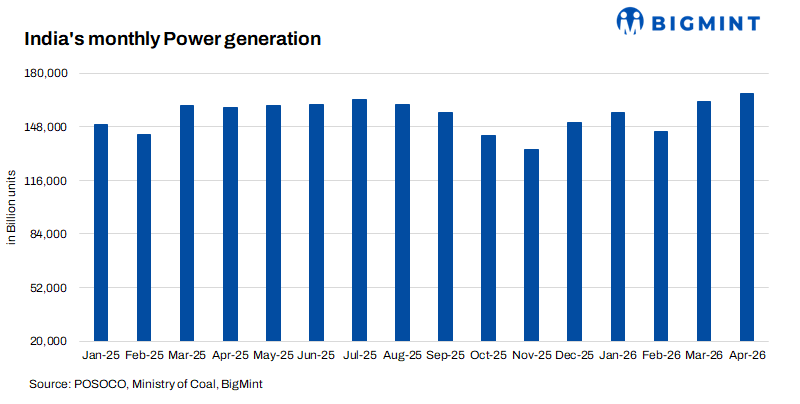

India’s power sector entered the peak summer of 2026 under severe strain. Despite a 5.3% y-o-y increase in total electricity generation in April 2026, a combination of record-breaking demand, regional coal shortages, and over-reliance on a stretched logistics network pushed wholesale power prices to the INR 10,000/MWh ceiling repeatedly during the month.

Renewable energy generation grew 22% y-o-y, but the thermal coal supply chain failed critical power plants in southern and western India, lifting electricity prices sharply during the evening.

Demand shocks the system

Peak electricity demand met during the day hit an all-time high of 256,117 MW on 25 April 2026, up nearly 9% from the April 2025 peak of 235,190 MW. The last week of April consistently saw demand above 250 GW — a level the grid was not designed to handle this early in the summer season.

The demand surge was not matched by a corresponding rise in thermal availability. The result was extreme volatility in the power exchange.

Price spikes signal supply crisis

Market data for April 2026 shows a dramatic deterioration in supply-demand balance during the last ten days of the month. Between 21 and 27 April, hourly market clearing prices hit the INR 10,000/MWh ceiling on multiple occasions during evening peak hours (19:00 to 23:00). On 24 April, purchase bids soared to 925,470 MWh, while sell bids remained flat at approximately 222,500 MWh, a mismatch that forced prices to the cap.

On 17 and 18 April, even during daytime hours, prices repeatedly touched INR 10,000/MWh. This is not a classic demand-driven price spike. It indicates that generators — especially coal-fired plants — were unwilling or unable to offer more capacity.

This is a fuel supply crisis transmitting directly into the power market.

What happens when the sun sets: The evening peak problem

The daily generation data reveals a distinct and worsening pattern. Solar generation contributes heavily during daytime hours, but its output begins to decline sharply after 16:00 and falls to near-zero by 18:30. The evening peak demand period typically 19:00 to 23:00 — coincides exactly with this solar drop-off.

During this window, the grid must rely on three sources:

- Coal and lignite (slow-ramping, but the primary base-load)

- Hydro (fast-ramping, but seasonally limited)

- Wind (variable, often lower in evening hours)

In April 2026, the evening peak saw the most severe price spikes. For example, on 22 April, between 19:00 and 23:00, prices remained at INR 10,000/MWh for four consecutive hours. On 23 April, the 19:00 to 22:00 block also hit the ceiling. These were not daytime events. They occurred precisely when solar had exited the grid.

The coal stock data explains why. Plants that would normally ramp up to meet evening demand were running low on fuel. Yadadri TPS in Telangana, with only 22% of normative stock, was generating at just 35% plant load factor (PLF). North Chennai Stage 2, at 19% stock, could not increase output. The grid, therefore, had to rely on expensive gas (where available) or accept price spikes.

The situation is self-reinforcing. Low coal stocks force plants to operate at reduced PLF or conserve fuel. Reduced PLF during the day means less buffer for the evening ramp. And when evening demand arrives, the only remaining mechanism to balance supply and demand is price — which is why the market cleared at the ceiling so frequently.

Coal generation rises, but logistics lag

Total coal-fired generation in April 2026 stood at 118,526 MU, up 2.4% from 115,720 MU in April 2025. On paper, this suggests steady thermal performance. However, the plant-level stock data tells a different story.

Renewable energy accounted for most of the incremental generation. Coal barely kept pace with demand growth, and in several regions, it failed to do so. Gas-fired generation fell by one-third, indicating high input costs or limited fuel availability.

Ground truth: Coal stocks at critical levels

Analysis of daily coal stock data for 30 April 2026 across major thermal power plants reveals a severe regional imbalance.

Key observations from plant-level data

Telangana is in the red. Yadadri TPS, a 2.4 GW plant, is generating at only 35% PLF due to coal starvation. Kothagudem (new) is burning stock faster than it is replenished, operating at 74% PLF but with only 19% of the required stock. The remarks column for these plants explicitly directs the Singareni Collieries Company Limited (SCCL) to “ensure supply” — an indication that the linkage is not delivering.

Tamil Nadu faces a twin crisis. North Chennai Stage 2 has stock in transit issues, meaning coal is allocated but not arriving. Stage 3 relies on Mahanadi Coalfields (MCL) for urgent supplies. Tuticorin TPS received 38,600 tonnes (t) on 30 April — well above its daily consumption of 11,200 t — yet still sits at just 41% of normative stock. This suggests a deep deficit carried forward from previous weeks.

Karnataka’s Yermarus TPP, despite 70% PLF and daily receipts of 19,700 t against consumption of 16,700 t, remains below the 40% threshold. The plant has been drawing down stock faster than it can be rebuilt.

What daily generation data shows

The daily generation figures for April 2026 reveal a system under progressive stress.

Over 1-15 April, total daily generation ranged between 5,200-5,700 million units (MU). Coal contributed 3,700-4,200 MU, while renewable energy ranged within 750-950 MU. Maximum daily demand during this period stayed below 235 GW.

From 16 April onward, the picture changed. Daily generation jumped to 5,800-6,100 MU. Coal generation peaked at 4,360 MU on 25 April. Renewable energy touched 1,171 MU on 17 April. Maximum demand crossed 250 GW on 24 April and hit 256 GW on 25 April.

However, coal generation could not sustain this level. By 30 April, coal generation had fallen back to 3,733 MU — a drop of 14% from the peak just five days earlier. Total generation fell to 5,505 MU, and maximum demand dropped to 234 GW.

This end-of-month decline is not seasonal. It reflects a system where fuel constraints forced lower thermal output, and the grid had to manage with reduced supply.

Market implications for May-June 2026

The outlook for the coming months is cautious for grid stability but clear for power prices.

Risks to monitor: Coal replenishment for stressed plants in Telangana, Tamil Nadu, and Karnataka requires immediate and prioritised rakes. Given ongoing summer passenger rail demand, this is not guaranteed. Hydro generation rose 11.8% in April, but reservoir levels will decline as summer progresses. Solar generation remains strong during the day, but the evening peak vulnerability persists.

Price outlook

Market clearing prices are expected to remain above INR 5,000/MWh for most of May, with periodic spikes to INR 10,000/MWh during evening hours. If coal supplies do not improve by mid-May, day-ahead prices may average INR 6,500-7,000/MWh.

Actions required

Three measures could alleviate the situation. First, expedite coal rakes to Telangana (Singareni linkage), Tamil Nadu (MCL linkage), and Karnataka. Secondly, provide temporary relaxation of import hedging norms for coastal plants to allow spot imports. Thirdly, implement demand-side measures for industrial consumers during evening peaks, such as time-of-day tariffs or voluntary load reduction.

The evening peak remains the weak point

The fundamental problem is not the total amount of coal in the country. It is the timing and location of coal availability relative to demand. Solar provides relief during the day, but it cannot address the evening peak. That load must be met by thermal and hydro. When thermal plants operate with thin coal buffers, they lose the ability to ramp up in the evening. The market then clears at the price ceiling — not because demand is extraordinarily high, but because supply has no room to move.

April 2026 was a stress test for India’s power system. Coal logistics failed a handful of large, strategically important plants in southern India. Market prices reflected that failure with an unprecedented frequency of INR 10,000/MWh events. The coming weeks will determine whether this was a transient logistics crunch or the beginning of a deeper structural problem.

BigMint will continue to track daily coal stocks, generation trends, and power prices. For real-time alerts and customised data sets, contact the research team.

Leave a Reply