- Currency depreciation and higher offers drive price upside

- Adequate inventories and cautious procurement may limit upside momentum

Indian portside prices of Indonesian-origin thermal coal registered a sharp week-on-week increase as of 1 May 2026, with gains of INR 200-400/t observed across grades.

The uptrend was primarily driven by the continued depreciation of the Indian Rupee against the US Dollar — hovering near record levels around INR 95/USD — alongside firmer export offers from Indonesian suppliers. Rising seaborne freight rates further added to the overall landed cost, exerting upward pressure on domestic portside prices.

A market participant learned that Improved demand fundamentals, particularly from Gujarat’s Morbi ceramic cluster, also supported the price rally, expectations that nearly 90% will be operational by mid-May. This phased ramp-up is anticipated to drive incremental coal demand, especially for mid- to lower-grade Indonesian coal typically consumed by the sector.

Price movement across key coal grades

Portside prices witnessed notable increases across major Indonesian coal grades. High-grade 5,000 GAR coal prices rose by around INR 400/t week-on-week to INR 10,100/t at Kandla and INR 10,000/t at Visakhapatnam, backed by improved offtake interest.

Mid-grade 4,200 GAR coal prices increased by INR 200/t to INR 7,850/t at Kandla and INR 7,750/t at Visakhapatnam, reflecting relatively balanced demand-supply dynamics. Meanwhile, lower-grade 3,400 GAR coal prices saw a sharper rise of INR 400/t to approximately INR 5,500/t at Navlakhi.

Port inventories indicate adequate supply

India’s non-coking coal inventories at major ports rose marginally by 2.1% w-o-w to 14.60 million tonnes as of Week 17 (ended 25 April), compared to 14.30 million tonnes in the previous week. The modest increase suggests that while cargo arrivals remained steady, evacuation levels were also sustained. Despite the recent price uptick, overall buying sentiment remained cautious, with consumers continuing to procure on a need-based basis.

Thermal power plant stocks remain comfortable but uneven

Coal inventories at Indian thermal power plants declined slightly during the week but remained broadly sufficient at 53.7 million tonnes, equivalent to around 17 days of consumption as of 30 April. However, stock distribution remained uneven, with approximately 23 plants operating at critical levels. These include plants reliant on domestic coal, imported coal, and washery rejects, highlighting localized supply tightness despite an overall comfortable inventory position.

Global market trends and freight impact

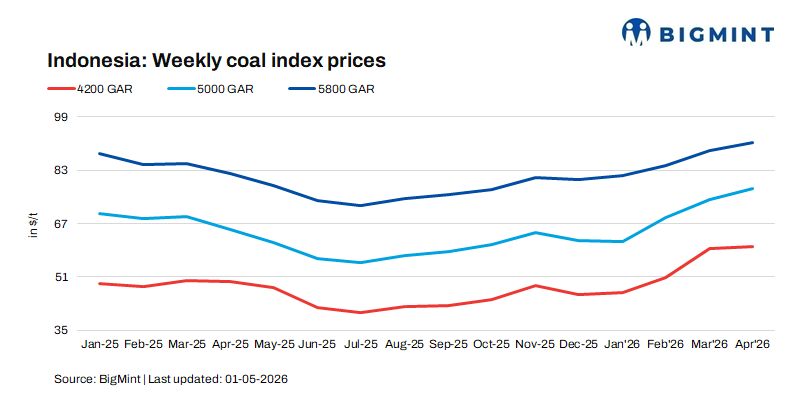

International coal markets presented uptrend signals. Indonesian benchmarks showed marginal strength, supported by improved Asian demand and relatively tighter spot availability. Prices for 5,800 GAR and 4,200 GAR coal increased by around $0.9-1/t, while 3,400 GAR prices edged up by $0.4-0.5/t.

Additionally, Indonesia’s HBA benchmark prices for the first half of May 2026 moved higher across all calorific value segments, reinforcing bullish sentiment.

On the logistics front, Supramax freight rates from East Kalimantan to Navlakhi remained stable week-on-week to around $21/t, further contributing to cost-push inflation in landed coal prices.

Outlook

Near-term outlook remains firm with limited upside potential. Prices are supported by INR weakness, stable global benchmarks, and gradual demand recovery. However, ample inventories, cautious buying, and comfortable power plant stocks may restrain gains unless supply tightens further.

Leave a Reply