- Balanced supply-demand keeps Indian coal prices stable

- Low-GAR tightness and Asian demand may boost prices

The Indian portside market for Indonesian thermal coal remained largely stable during the week ending 8 August 2025, with only minor adjustments observed in select low-grade segments. According to the latest assessment by BigMint, prices across most grades and ports registered minimal week-on-week (w-o-w) variation, reflecting a balanced supply-demand environment in the domestic market.

Stable pricing across key grades

Indonesian thermal coal prices maintained a steady trend across major Indian ports. The 5000 GAR grade was assessed at INR 7,150/tonne (t) at Kandla and INR 7,050/t at Vizag, unchanged from the previous week. Similarly, the 4200 GAR grade held at INR 5,700/t at Kandla and INR 5,600/t at Vizag.

In contrast minimal surge was seen in the 3400 GAR grade prices rising by INR 50/t reaching at INR 4,450/t at Navlakhi Port, where localized supply tightness supported prices despite broader market stability.

Portside coal stocks see moderate decline

India’s portside thermal coal inventories fell by 3.4% w-o-w to 14.27 million tonnes (mnt) in Week 31, compared to 14.77 mnt in the previous week. The decline was driven by a slight uptick in demand for South African coal and the fact that most traders have sold out their August cargoes, shifting focus towards September arrivals. The tightness in spot availability for Indonesian grades was more evident in certain low-GAR cargoes, although overall supply remains adequate.

Freight rates ease on Indonesia-India route

Supramax freight rates on the Indonesia (East Kalimantan)-India (Navlakhi) route eased by $0.24 per dry metric tonne (dmt) w-o-w to $15.9/dmt. While the decline offers slight relief to landed costs, its impact on portside pricing has been muted given steady domestic demand and trader caution ahead of September shipments.

Power plant stock levels decline

Thermal power plant coal stocks in India declined to 52.96 mnt as of 6 August 2025, down from 54.33 mnt a week earlier. Although the current reserves are sufficient for around 18 days of power generation, 12 plants continue to operate at critical stock levels. These shortages span across domestic, imported, and washery-reject coal, indicating ongoing inefficiencies in supply chain coordination despite healthy aggregate reserves.

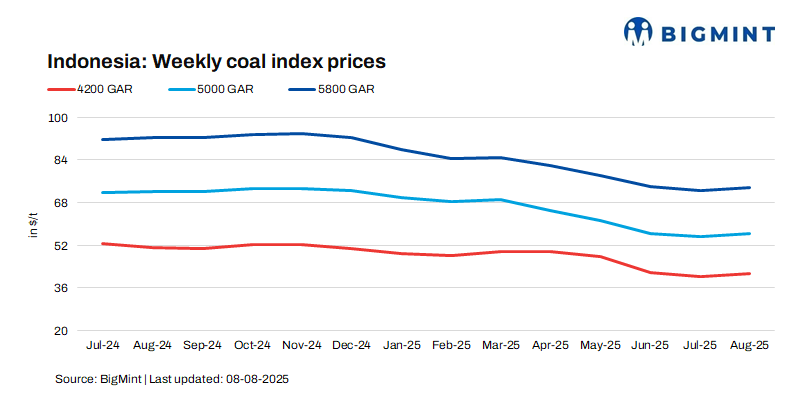

International market records modest gains

On the global front, Indonesian coal prices saw slight upward movement. The 5800 GAR grade rose by $0.39/t to $73.7, the 4200 GAR grade increased by $0.90/t to $41.8, and the 3400 GAR grade edged up by $0.10/t to $29. The gains were supported by limited spot availability from producers and selective restocking demand from East Asian buyers. However, sentiment remains cautious, as demand recovery in key importing regions continues at a slow pace.

Outlook

India’s portside market for Indonesian thermal coal expected remain range-bound, with gains capped by weak demand and ample stocks. However, local tightness in low-GAR cargoes and any rebound in Asian buying could lift prices in the coming weeks.

Leave a Reply