- Consumption weak y-o-y amid high prices and fuel switching to coal

- Import dependence persists as domestic output meets ~70% demand

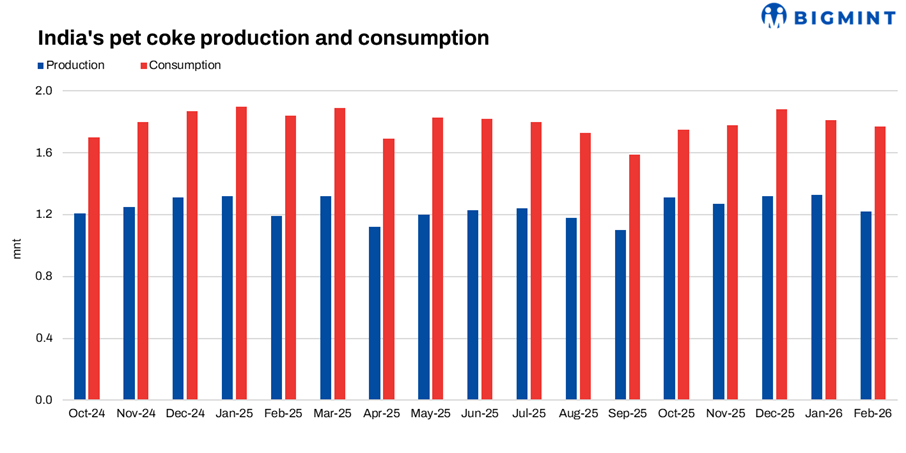

Domestic petcoke production and consumption trends in India reflected a mixed yet stable trajectory in February 2026, shaped by refinery operations, demand dynamics, and evolving global conditions. Production stood at 1.22 mnt, registering a marginal 2.6% y-o-y increase, while declining 8.5% m-o-m from January due to shorter operational days. On a cumulative basis (April-February of FY’26), production reached 13.49 mnt, slightly lower by 1.2% y-o-y, indicating overall stable but subdued output levels.

Production trends and supply dynamics

Petcoke production in India continues to remain closely linked to refinery product mix decisions, particularly output of high-value fuels such as diesel, petrol, and ATF. As a by-product of delayed coking units (DCUs), production does not respond directly to petcoke demand but rather to broader refining economics.

In February, the decline in m-o-m production was primarily attributed to operational factors such as fewer days in the month. However, global developments, including geopolitical tensions in the Middle East, have created uncertainty in crude supply chains. Rising freight, insurance costs, and logistical disruptions may impact refinery throughput going forward, potentially influencing petcoke output in the coming months.

At the same time, India’s continued access to alternative crude sources such as Russia provides some cushion against supply shocks. Structurally, domestic production remains insufficient to meet demand, with output meeting only 68-73% of consumption, necessitating continued reliance on imports.

Consumption trends and demand outlook

Petcoke consumption in February stood at 1.77 mnt, down 4.5% y-o-y, while cumulative consumption during April-February declined 8% y-o-y to 18.55 mnt. Despite this, demand fundamentals remain linked to infrastructure activity, particularly from the cement sector, which is the largest consumer.

Post-monsoon recovery in construction activity has supported gradual demand improvement since November. However, overall consumption has remained lower compared to last year, largely due to rising petcoke prices and shifting fuel economics. Cement manufacturers, who can switch between coal and petcoke, have increasingly opted for coal in recent months due to better cost competitiveness.

Import regulations also play a critical role in shaping consumption. While imports of raw petcoke (RPC) and calcined petcoke (CPC) are regulated, cement sector imports remain unrestricted, making them the dominant driver of import volumes.

Overall, the demand outlook remains cautiously firm, supported by infrastructure activity, but sensitive to price movements and global supply dynamics. The interplay between coal and petcoke prices will continue to influence consumption patterns in the near term.

Leave a Reply