- Capacity expansions disproportionately higher than production growth

- Declining exports on weak Chinese demand impacts utilisation rate

- Weak steel prices squeeze margins, some DRI makers shift to lumps

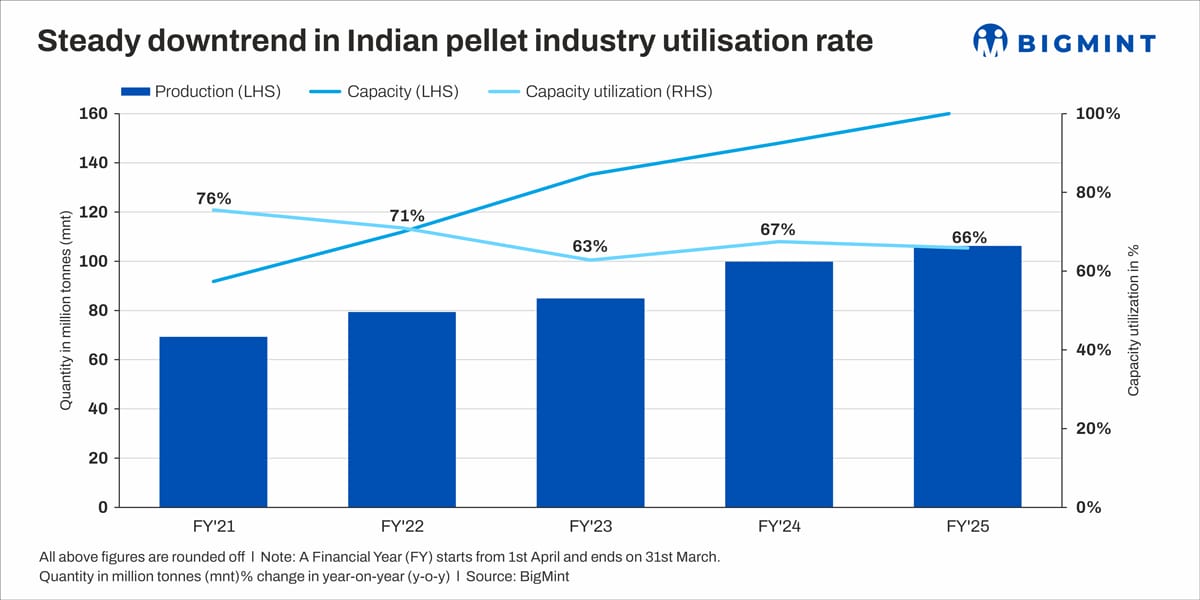

Morning Brief: The Indian pellet industry has seen a steady decline in production capacity utilisation rates between FY’21 and 7MFY’26, with a cumulative drop of 10% in capacity utilisation rate, as per BigMint data.

In the last five years, capacity utilisation rates were at their healthiest at 76% in FY’21, which then fell to a low of 63% in FY’23. Since then, there has been a minor recovery, with capacity utilisation at 67% in FY’24, 66% in FY’25, and 68% in 7MFY’26 (April-October 2025), but the peak of FY’21 remains out of reach.

This trend seems to be an anomaly, given that India’s steel production is on the rise and the consumption of sponge iron has also jumped (by 41% between 2021 and 2024). Notably, some major blast furnace-based producers have also lifted the share of pellets in their raw material mix to 40-50% from 20% previously.

Consequently, the question arises: Why have India’s pellet producers failed to lift capacity utilisation rates in recent years? What challenges have affected pellet producers? BigMint goes behind the scenes.

Factors affecting pellet industry utilisation rate

Capacity expansions overtake production growth: India’s pellet production recorded a robust compound annual growth rate (CAGR) of around 9% over FY’21-25 to 106.3 million tonnes (mnt) in the last fiscal year. However, pellet production capacity expanded at a faster pace of 12% during the same period, totalling 161.3 mnt in FY’25.

In absolute volumes, over FY’21-25, India/s pellet production increased by 37 mnt, while installed capacity rose by 69.5 mnt.

The indiscriminate increase in installed capacity has been driven by optimism around rising crude steel production and sponge iron usage. Strong export momentum also influenced significant capacity expansion plans.

Export momentum wanes: Weakening exports have curtailed offtake from pellet plants, keeping production enthusiasm low.

During the pandemic, in FY 21, exports had totalled a massive 13.8 mnt, while in FY’22, they were at 11.1 mnt. This had given rise to an imbalance in the domestic market and prices in 2022, consequently prompting the imposition of a steep 45% export duty in May of the same year.

Although the duty was rolled back in November, the damage was significant: capacity utilisation rates dropped by eight percentage points in FY’23, mirroring the steep plunge in exports to 6.3 mnt.

While exports recovered to 11.3 mnt in FY’24, volumes again fell in FY’25 to 6.9 mnt. In 7MFY’26, export volumes have declined further by 54% y-o-y due to weak demand from China.

Limited availability of high-grade iron ore: Blast furnace (BF) grade (Fe 63-65%) and direct reduced (DR) grade (around Fe 67%) are the two standard grades produced. Production of the latter has been constrained by the limited availability of high-grade iron ore and deteriorating quality of domestic ore. Grade depletion has reached a stage where even the availability of quality BF-grade pellet feedstock has become uncertain.

Additionally, it is understood that the shortage of the required high-grade pellets triggered imports of a massive 1.2 mnt in 7MFY’26.

Margins tighten amid falling steel prices: Pellet producers have faced leaner margins in recent months due to comparatively elevated iron ore costs despite weak finished steel prices, with several commodities trading at a five-year low. This also may have contributed to low operational rates.

For example, Fe 62% fines prices averaged INR 5,400/tonne (t) ex-mines Odisha as of 29 November in Q3FY’26. This is significantly higher (38%) than the INR 3,900/t recorded in Q3FY’23. Conversely, induction furnace (IF) rebar prices, exw-Raipur, have plunged by INR 10,400/t (20%) to an average of INR 41,600/t in Q3FY’26 (till 29 November) from INR 52,000/t in Q3FY’23.

Consequently, due to downward pressure from finished steel prices, pellet prices, DAP Raipur, have increased by a slower INR 1,600/t (19%) to INR 10,000/t in Q3FY’26 against INR 8,400/t in Q3FY’23, despite a much higher surge in iron ore costs.

Some sponge producers shift to CDRI: Procurement by sponge iron units has been somewhat muted in the last few months, even though DRI production has increased by 9% y-o-y in H1FY’26. It is heard that some major Chhattisgarh-based sponge iron plants have switched to DR-CLO-based production (CDRI). Tight margins and high competition in pellet-based production have prompted this move. Producers that self-consume their DRI production have also embraced this shift.

Consequently, the price gap between PDRI and CDRI narrowed to INR 3,000-3,200/t last week, as per sources, compared to INR 3,800-4,000/t at the beginning of November.

Outlook

The pellet industry’s capacity utilisation rates are unlikely to improve unless significant structural changes are made. India’s heavy export reliance on China poses a considerable risk, and the expected downtrend in crude steel production is likely to pressure Indian pellet makers. Meanwhile, encouragingly, capacity utilisation rates have remained largely stable y-o-y so far in FY’26 despite lacklustre exports, indicating perhaps that domestic consumption has improved, at least to a certain degree.

Some producers have flagged rising imports as the key factor leading to low capacity utilisation. However, BigMint’s analysis suggests that the downtrend began much before the start of import arrivals. In fact, even with 1.2 mnt of imports in 7MFY’26 against 0.02 mnt in 7MFY’25, the pellet capacity utilisation rate has inched up by two percentage points y-o-y to 68%. Imports, however, might remain attractive for many producers along the west coast due to cost considerations.

Leave a Reply