- Rising steel, raw material prices propel trend

- Indian mills betting big on post-election demand

- Bulk imports likely to remain high in short term

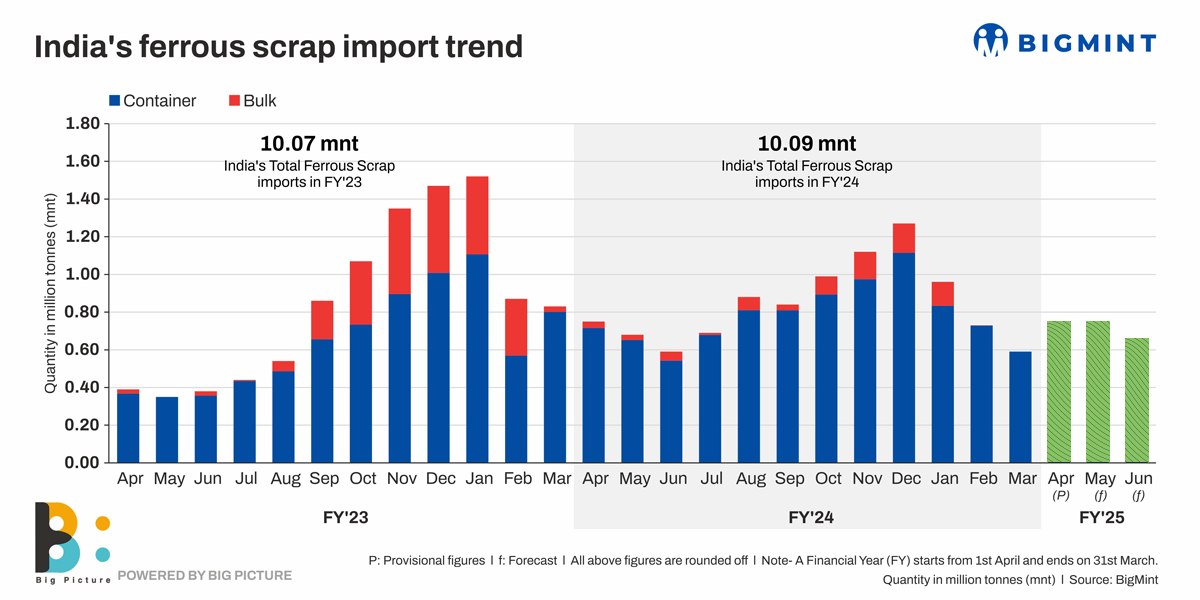

Morning Brief: Indian scrap buyers are again showing a propensity to buy bulk cargoes after a long hiatus. Data maintained with BigMint shows imports of bulk ferrous scrap cargoes had dropped sharply from March 2023, and had remained depressed throughout last fiscal (FY’24) at a mere 0.75 million tonnes (mnt) compared to a far heftier 2.30 mnt in FY’23.

However, as per the latest information available, India secured bookings of approximately six bulk scrap vessels in April 2024. These, originating in the US west coast, are probably expected to reach Kandla, Chennai, and Vizag ports in May -June. The deals were heard at $400-405/tonne (t) for shredded and $395-400/t for HMS 80:20. It may be noted that bulk offers have also increased by $5-10/t of late.

Why are bulk scrap imports increasing of late?

1) Rising steel prices in India: Prices of finished steel are increasing in India on the back of three reasons. One is the production cuts undertaken, especially in longs, from January, which helped to restore the supply-demand imbalance that had been plaguing the market especially since the second half of last year. Secondly, pre-election restocking demand unleashed from March in particular, which helped to keep prices supported. Rising demand, especially for longs, helped to keep demand for scrap as a raw material for induction furnace mills, supported. Thirdly, there is a raw material cost push. The billet index, ex-Raipur, is averaging INR 43,000/t ($516/t) in April against March’s INR 40,000/t ($480/t). Sponge iron, exw-Rourkela, is up at INR 29,500/t ($354/t) in April against INR 26,600/t ($319/t) in March.

IF-route rebar prices, ex-Mumbai, thus, have shown a steady uptrend. From February’s INR 48,000/t ($576/t) these rose to INR 49,000/t ($588/t) in March and are crossing INR 50,000/t ($600/t) in April.

2) Gap between domestic, imported prices narrows: Prices of imported scrap may have bottomed out. HMS 80:20, imported from Europe, in April, are hovering at INR 35,500/t ($426/t) CFR Nhava Sheva. M-o-m, these have dipped 5%. In contrast, domestic HMS 80:20 upped to around INR 35,000/t ($420/t) so far in the current month. M-o-m, domestic prices have increased 6%. With the increase in domestic scrap prices, the gap with imported has increasingly bridged. In April it narrowed to INR 600/t ($7/t) from INR 900/t ($11/t) in March and INR 1,960/t ($24/t) in February.

Imported prices are falling because of the overall global drop in demand for steel amid increasing geo-political tensions, supply disruptions, rising currencies and inflation. Domestic prices are rising on the back of the pre-election restocking.

There is a mere gap of INR 500-600/t ($6-7/t) between imported and domestic and this can be further bridged as there is scope for increase in the latter’s prices in anticipation of post-election demand.

3) Post-election demand expectations run high: The market is very bullish that post-elections, demand would get a further fillip. This hope is fuelled by the fact that the country would return to political stability and the government would continue to give infrastructure sustained push to keep steel demand buoyant. This factor is also fuelling bulk scrap imports.

4) Sponge production hiccups: Induction furnace mills are seen restocking scrap ahead of monsoons on fears of sponge production disruptions. Production costs of sponge iron increase in the rainy season because of the higher level of moisture present in iron ore/pellets. Resultantly, sponge manufacturers reduce production in the monsoons.

Secondly, prices of South African coals are rising and this may reduce imports, which may further impact sponge production in the near future. This is another reason why IF mills are seen restocking on scrap heavily.

South African coals, mainly RB2 and RB3 which are particularly suited for sponge production in India, have picked up in the last 10 days owing to coal shortage at South Africa’s prime export terminal because of a few derailment issues. The ensuing disruptions in supply are causing price increases although things are smoothening out slowly.

Outlook

Bulk scrap imports are likely to sustain in the short-to-medium term, propped by post-election demand expectations.

Secondly, even if imported coal prices subside with the resolution in South African logistics issues, the impending rainy season will see sponge units undertaking production cuts which will keep scrap procurements supported.

Thirdly, domestic scrap prices have the potential to rise further, impelled by the increase in prices of competing raw materials like sponge and billets, as well as higher steel demand while bulk imported prices may remain competitive amid persisting lacklustre global steel demand.