- Cost pressure due to higher coking coal prices

- Tight foundry-grade supply supports prices

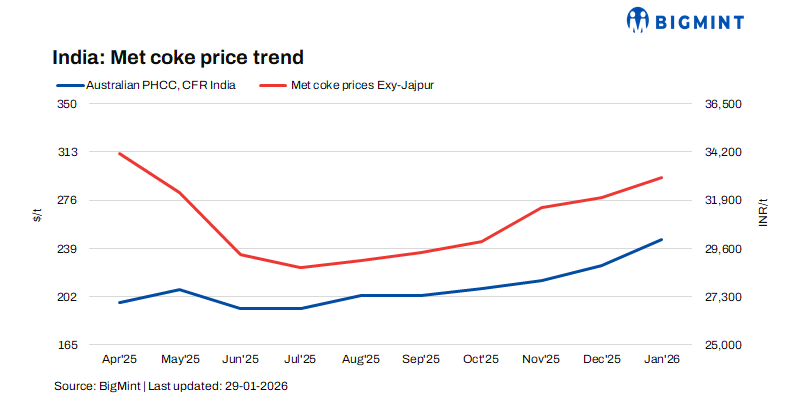

Indian blast furnace (BF) and foundry grade metallurgical coke prices registered a sharp w-o-w increase, as assessed on 28 January. The upward price movement was primarily driven by escalating raw material costs, particularly coking coal, coupled with firmer sentiment in upstream markets. Limited availability of foundry-grade material further reinforced bullish pricing trends.

Price movement across regions

In eastern India, BF-grade metallurgical coke (25-90 mm) prices increased by INR 500/t w-o-w to INR 34,000/t ex-Jajpur. This rise was largely due to higher coking coal prices and market expectations of increased production costs in the coming weeks.

Similarly, prices in western India witnessed a moderate increase. BF-grade coke prices rose by INR 200/t w-o-w to INR 30,300/t ex-Gandhidham, reflecting cost push pressures and improved sentiment despite relatively stable regional demand.

Foundry-grade metallurgical coke (+90 mm) recorded a sharper rise, with prices climbing by INR 900/t to INR 36,100/t ex-Rajkot. Market participants indicated that offers were heard at even higher levels, largely due to constrained supply availability and steady demand from downstream foundry units.

Coking coal price dynamics

Coking coal sentiment strengthened notably on a w-o-w basis, primarily due to supply-side disruptions in Australia caused by adverse weather conditions. These disruptions led to tighter availability of seaborne material, resulting in Australian premium hard coking coal (PHCC) prices rising by $14/t to $251/t FOB Australia.

In contrast, the Chinese domestic coking coal market remained stable on 27 January, with prices unchanged across major producing regions. Market activity remained subdued amid weak downstream demand, narrow operating margins, and cautious procurement strategies adopted by coking plants and steel mills. With limited support from both cost and demand fundamentals, the Chinese market continued to face a supply-demand stalemate, and prices are expected to remain range-bound in the near term.

Support from pig iron market

The domestic pig iron market provided indirect support to metallurgical coke prices during the assessment period. Steel-grade pig iron prices ex-Durgapur increased by INR 750/t w-o-w to INR 38,500/t, underpinned by stable demand conditions.

Further strengthening market sentiment, SAIL-Bhilai conducted an auction on 23 January for 4,940 t of steel-grade pig iron, with the entire quantity successfully booked at an average price of INR 36,850/t ex-works. This marked a significant increase of INR 2,950/t compared with the previous auction held on 27 December, where 910 t was booked at an average price of INR 33,900/t ex-works. The sharp rise in bids highlighted improved buyer confidence and reinforced upstream cost support for coke producers.

Market outlook

The Indian metallurgical coke market is expected to remain firm, supported by high coking coal prices, tight foundry-grade supply, and steady pig iron demand. Further upside will depend on global coal prices and steel demand, while any easing in coal supply or weak steel margins may limit gains. Overall, prices are likely to consolidate at elevated levels with a mild upside bias.

Leave a Reply