- BF-grade met coke prices increased w-o-w on firm coal costs and stronger imports

- Market stable with limited upside due to cautious steel demand

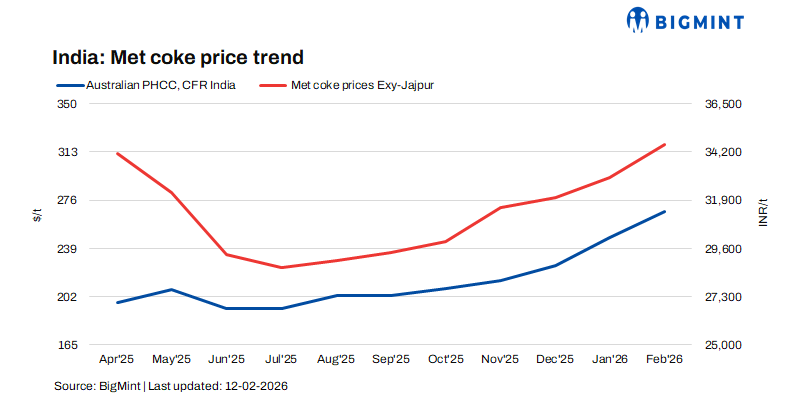

Indian blast furnace (BF) grade metallurgical coke prices recorded a week-on-week increase as of 11 February, supported by firm raw material costs and firmer imported met coke offers.

In eastern India, BF-grade coke (25–90 mm) prices rose by INR 500/t to INR 34,800/t ex-Jajpur, reflecting stronger cost pressures and improved trade sentiment. Fresh offers from a few players were even heard around INR 35,500-36,000/t exw Jajpur. In western India, prices increased by INR 100/t to INR 30,400/t ex-Gandhidham, while parallel assessments indicated levels around INR 30,300/t ex-Gandhidham.

The upward movement was largely attributed to higher coking coal procurement costs and strengthened import price indications, particularly from Indonesia, where BF coke (65/63) was heard at $270-275/t CFR India. There is still a gap between imported cost of Indo met coke and prevailing domestic met coke prices, with other import origins becoming less viable post anti dumping, domestic met coke continues to remain a preference.

The firmer import parity provided additional support to domestic suppliers in maintaining higher offer levels. Meanwhile, foundry-grade metallurgical coke (+90 mm) prices remained stable at INR 36,100/t ex-Rajkot, indicating balanced demand conditions in the casting segment.

Factors impacting Indian met coke prices

Australian premium hard coking coal prices declined w-o-w by $4/t to $249/t FOB, primarily due to subdued buying interest from key importing markets and cautious procurement.

On 11 February, China’s metallurgical coke markets remained broadly stable as supply-demand pressures eased. First-grade dry-quenched coke prices were unchanged at RMB 1,705/t in Tangshan, RMB 1,590/t in Changzhi, and RMB 1,480/t in Lüliang (cash, ex-factory).

Holiday-related mine suspensions temporarily tightened coal supply and curtailed spot trading activity; however, overall market fundamentals remained balanced. Coke production levels were steady, though slower procurement from steel mills contributed to a mild inventory build-up at coke plants. With winter restocking largely concluded and downstream steel demand relatively subdued, market participants expect limited volatility in the near term.

Domestic pig iron auction reflects improved domestic sentiment

BigMint’s assessment for Durgapur steel grade pig iron stood at INR 38,700/t exw, stable w-o-w. SAIL-Bhilai conducted an auction for 2,990 tonnes of steel-grade pig iron on 9 Feb’26, with the entire quantity successfully booked at an average price of INR 37,400/t ex-works. The realised price marked an increase of INR 550/t compared to the previous auction on 23 January 2026, where 4,940 tonnes were sold at an average of INR 36,850/t ex-works.

The higher bid levels suggest improved buying interest and firmer sentiment in the domestic steel value chain, potentially influenced by stable raw material trends and expectations of steady steel demand.

Market outlook

Indian BF-grade met coke prices are expected to remain firm, supported by high input costs and strong imports, though cautious buying may cap gains. Foundry-grade prices should stay stable. Overall, the market is likely to remain steady with a slight firm bias, dependent on steel demand and coal prices.

Leave a Reply