- Rising coking coal costs support met coke price gains in India

- Chinese mills resist met coke price hikes

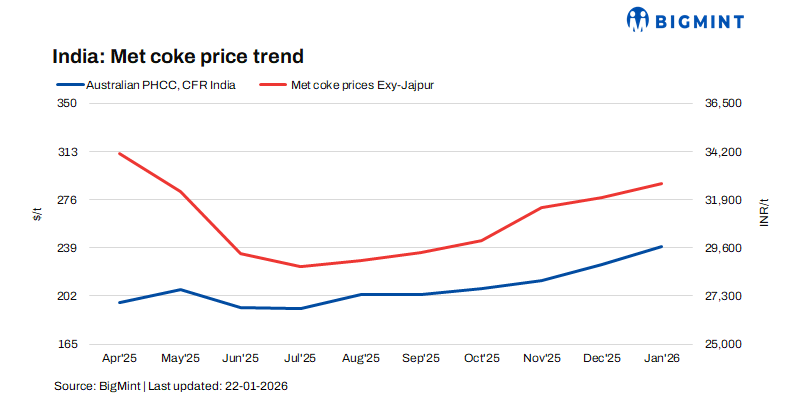

The Indian BF-grade metallurgical coke market recorded a sharp week-on-week increase during the week ended 21 January, primarily supported by rising raw material costs and firmer upstream sentiment. However, the price rise was region-specific and not accompanied by a meaningful improvement in spot trade activity.

Price movement

In eastern India, prices of BF-grade metallurgical coke (25-90 mm) increased by INR 1,200/t w-o-w to INR 33,500/t ex-Jajpur. The uptick was largely attributed to strengthening coking coal prices and expectations of higher production costs.

Conversely, prices in western India remained stable at INR 30,100/t ex-Gandhidham, reflecting relatively comfortable supply conditions and subdued buying interest.

Demand and trading activity

Market participation remained subdued during the assessment period, with no notable improvement in transaction volumes. End-users largely avoided fresh procurement, preferring to rely on existing inventories amid uncertain price direction. Additionally, Sankranti-related holidays disrupted industrial operations and logistics, further dampening near-term demand and trading activity.

Coking coal price dynamics

Coking coal sentiment strengthened significantly on a week-on-week basis, driven by supply-side disruptions in Australia caused by adverse weather conditions. As a result, Australian premium hard coking coal (PHCC) prices rose by $ 9/t to $ 237/t FOB Australia.

Market sources indicated that PHCC prices could increase further in the coming week. However, the rise in coking coal prices has not yet been fully reflected in metallurgical coke prices, as most producers are still operating on earlier coal contracts. The cost impact is expected to materialize in shipments arriving from late February to early March, suggesting a lagged pass-through to coke pricing. In the interim, the presence of older coke inventories procured at lower costs is restraining immediate price escalation.

Chinese metallurgical coke market

Chinese metallurgical coke prices remained stable during the week. As of 20 January, quasi-grade dry-quenched coke prices were unchanged, according to Lange Steel Network. Although steel mills resisted the first round of proposed price hikes, tightening supply, low inventory levels at coking plants, rising production costs, and sustained losses in the coking sector indicate the possibility of short-term price adjustments, pending further negotiations.

Support from the pig iron market

The Indian pig iron market continued to provide indirect support to the coke sector. Steel-grade pig iron prices ex-Durgapur increased by INR 1,050/t week-on-week to INR 37,750/t, reflecting stable demand fundamentals. Higher pig iron prices generally improve operating margins for blast furnace operators, thereby supporting metallurgical coke consumption and price sentiment.

Market outlook

Indian BF-grade metallurgical coke prices are likely to remain muted in the near term due to subdued demand, holiday disruptions, and lower-cost inventories. However, higher coking coal prices and tightening supply are expected to support price gains from late February to early March, with steel and pig iron demand acting as a key upside driver.

Leave a Reply