- Weak demand, rising port inventories push US coal prices lower

- Buyers shift to cheaper domestic and alternative coals

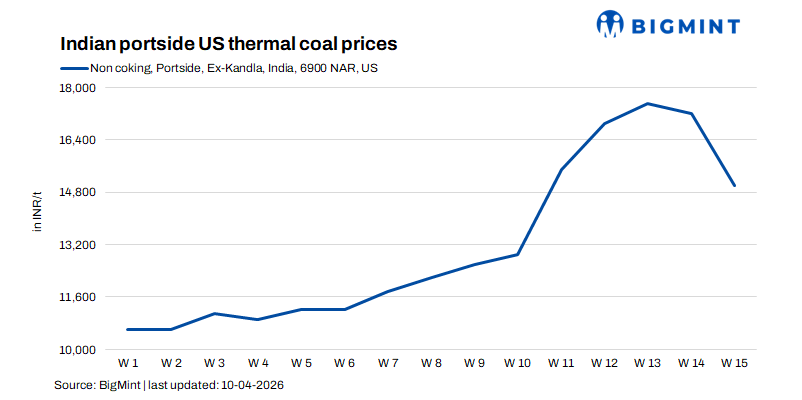

Rapid rise, faster fall

Barely two weeks ago, the market for US-origin high calorific value thermal coal in India was defined by scarcity and speculation. Prices at the west coast ports of Kandla and Tuna had climbed to levels that many buyers considered unsustainable. By late March, offers for NAPP (Northern Appalachian) coal were being quoted in the range of INR 17,000 to INR 18,500/t driven by supply disruptions in the Middle East and expectations of continued tightness.

That momentum has since reversed. By the first week of April, prices had begun a steady decline. On 1 April, offers at Tuna softened to INR 16,500-17,000/t. By 7 April, indicative prices had fallen further to INR 14,500-16,000/t. A day later, on 8 April, trades and indications were being reported at INR 14,500-15,500/t, with some participants noting that material was available at Tuna for around INR 15,000/t.

The cause of this correction was not a single event but a confluence of factors: the arrival of previously delayed vessels, a build-up of port inventories, and a decisive pullback in buying interest from both industrial and retail consumers.

Inventory build-up and weak lifting

Data from the week ending 6 April shows the scale of the supply overhang. Combined stocks of NAPP coal at Kandla and Tuna stood at nearly 307,000 t. Yet total lifting by retail and industrial buyers during that same week was only 74,000 t, indicating that offtake was significantly trailing supply.

Several vessels arrived in late March, including the Carouge at Tuna on 16 March with a price of $110/t, the Corona and Key Feature at Tuna in late February and early March with prices around $119.50/t, and the Tokyo Queen at Tuna on March 31 at $121.92/t. These cargoes, contracted weeks earlier during a period of rising prices, were now arriving into a market where buyer resistance had hardened considerably.

One trader noted that previous high price levels had been “completely hypothetical,” creating a market where few actual transactions were possible. Another observed that freight levels had risen sharply, making it difficult to take new positions, and that demand across the industry remained subdued.

Cement sector turns away from petcoke, expensive coal

The most significant shift has occurred in the cement industry, which has traditionally been a flexible consumer able to switch between petcoke and thermal coal depending on relative prices. Current market conditions have made that choice unavoidable.

By early April, CFR India East prices for US-origin 6.5% sulfur petcoke had reached $160/t, reflecting a sustained upward trend driven by tight global supply and elevated freight rates. Freight from the US Gulf to India’s east coast rose to $50.50/t, its highest level in over two years.

In contrast, thermal coal alternatives were available at substantially lower prices. CFR India West 5,500 NAR coal was assessed at $104.6/t on 9 April, while CFR India East 5,500 NAR coal was assessed at $103.35/t. An India-based buyer confirmed that his company had shifted entirely to coal and was no longer considering petcoke under current market conditions. Other cement producers, particularly smaller ones, have also moved away from petcoke for the time being.

Cement manufacturers are struggling to pass on higher fuel costs to their customers, which has squeezed margins and reinforced the incentive to seek cheaper alternatives. Several market participants noted that buyers were actively looking at Russian, South African, Australian, Indonesian, and domestic coal as replacements for both US-origin material and petcoke.

Retail and brick kilns switch to domestic coal and biofuels

The retail segment, which includes brick kilns and other small industrial users across Gujarat, Rajasthan and Punjab, has also responded to high prices by shifting away from imported US coal.

Multiple traders reported reduced loading activity at ports and subdued industrial demand. One market participant noted that brick kilns had started sourcing alternative domestic coal from Dhanbad, Varanasi, and Raniganj to replace high-CV US coal. Some users had even turned to bio-fuels such as agricultural waste rather than pay the elevated prices for US-origin material.

This shift in buyer behaviour has contributed directly to the inventory build-up at Kandla and Tuna, as retail offtake has failed to keep pace with fresh arrivals. One trader summarised the situation simply: there is no demand for portside offers.

Freight and geopolitical context

Freight rates have played an important role in the price correction. Richards Bay to India west coast Panamax freight was assessed at $19.35/t on 9 April while Supramax freight from Richards Bay to Port Qasim was $24.75/t. These levels, while elevated by historical standards, have not been sufficient to make US-origin coal competitive against Russian or South African alternatives.

The US-Iran ceasefire announced on 7-8 April has added further downward pressure on seaborne coal and petcoke prices globally, though freight and insurance uncertainties remain. Market participants are watching closely to see whether the ceasefire holds and what it will mean for vessel movements through the Strait of Hormuz.

Outlook

Looking ahead, the outlook for US high-CV coal in the Indian market depends on two main factors: the pace of price adjustment and the persistence of fuel switching in the cement and retail sectors.

For petcoke to regain share in the cement industry, its premium over thermal coal would need to shrink substantially from current levels. For US coal to attract buyers again, prices may need to fall further to compete with Russian, South African, and domestic alternatives.

What is clear from the past two weeks is that Indian industrial consumers are price-sensitive and technically capable of switching fuels when economics dictate. The speculative price spike of March has given way to a sober correction in April, and the market is still searching for a new equilibrium.

Leave a Reply