- Pellet exports record sharper 56% drop than iron ore’s 33%

- Iron ore production falls despite rising crude steel output

- Exporters slash exports amid unviable prices, poor margins

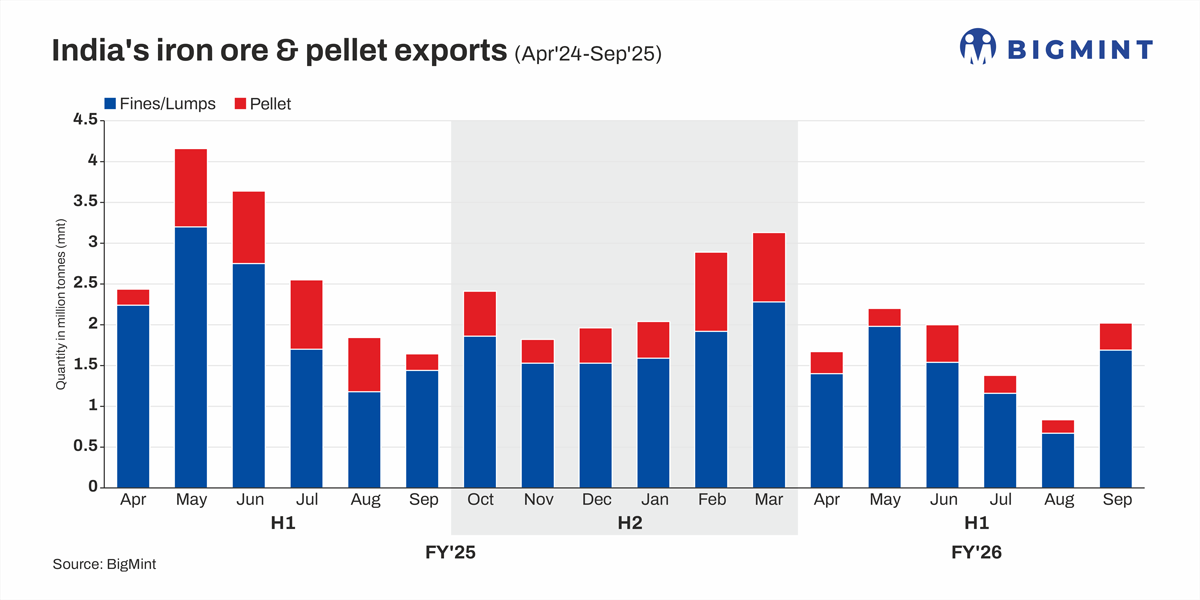

Morning Brief: Indian iron ore and pellet exports plunged by 38% y-o-y to 10.11 million tonnes (mnt) in the first half of FY’26, as per data available with BigMint. However, the y-o-y percentage decrease narrowed from the 45% recorded in 5MFY’26, driven by a sharp m-o-m rebound in September 2025.

September saw shipments of 2.02 mnt, a surge of 143% against a three-year low of 0.83 mnt seen in August. Volumes increased by a milder 22% y-o-y.

This recovery in export volumes was due to a hike in global iron ore prices in China (Fe 62% fines up $3.5/t m-o-m to $105.5/t CFR in September), speculation around the imposition of an export duty in India, and active restocking ahead of the Golden Week holidays. Expectations of a steel demand recovery after the military parade in early September also bolstered volumes.

The y-o-y decline in pellet exports in H1FY’26 has been sharper than that in iron ore. Notably, iron ore exports were down by 33% at 8.45 mnt, while pellet shipments fell 56% to 1.66 mnt.

Country-wise export destinations

China accounted for 86% of exports, with 8.71 mnt. The next two leading destinations — Malaysia and Indonesia — received minor volumes, at 0.50 mnt and 0.28 mnt, respectively.

Commodity-wise exporters

In the iron ore segment, major exporters in H1FY’26 were Rungta Mines (2.9 mnt), Vedanta (1.2 mnt), and OCL Iron and Steel (0.9 mnt). Meanwhile, the top pellet exporters were KIOCL (0.9 mnt) and AMNS (0.6 mnt).

Factors influencing India’s iron ore, pellet exports

- Export prices turn unviable: One of the primary reasons behind the sizeable decline in export volumes seems to be unfavourable pricing. Data shows that in January-March 2024, when Indian Fe 57% fines were at $93/t CNF Qingdao, export volumes averaged 4.03 mnt/month. As prices fell, export volumes also moderated, as Indian traders were unable to secure decent margins on their cargo.

Indian traders generally consider $78-82/t CNF as the threshold level for earning profits on exporting iron ore fines.

In H1FY’26, the monthly average export prices of Fe 57% fines hovered within the $70-79/t CNF range. April-June witnessed levels of around $70-71/t, and subsequently, prices increased each month, reaching $79/t in April. This rise in pricing, tracking global benchmarks, contributed to September’s higher volumes.

In comparison, in H1FY’25, monthly average prices reached a high of $81/t CNF Qingdao in May, following which, from June, tags hovered within the $68-72/t CNF range. April-June exports averaged 2.73 mnt/month, which almost halved in July-September to 1.44 mnt. In H1FY’26, exports averaged 1.41 mnt each month.

In H1FY’26, export prices approached this value only in September, which recorded a monthly average of $115/t. Additionally, realisations from domestic sales have consistently exceeded those from export trades. In August, domestic realisations were higher by INR 1,700-2,000/t, which narrowed to around INR 1,000-1,300/t in September, due to the increase in export prices.

- India’s iron ore production inches down in 5MFY’26: India’s iron ore production inched down by approximately 2% y-o-y in April-August 2025 (5MFY’26) to around 114 mnt. However, India’s crude steel output rose by 12% y-o-y during the same period to 68.3 mnt, suggesting that a demand-supply shortfall has emerged in the domestic market. This likely limited material allocation for exports.

India’s iron ore imports have also quadrupled to 6.17 mnt in H1FY’26 compared to 1.41 mnt in H1FY’25, though factors such as competitive pricing also played a significant role in boosting procurement of overseas-origin material.

To boost iron ore supply, the government has mulled implementing measures such as an export duty for curbing the outflow of material. However, no concrete announcement has been made, though certain importers have ramped up procurement as a knee-jerk reaction, as seen in September.

- China’s steel demand remains depressed: China, India’s largest iron ore buyer, continues to face declining steel consumption due to a prolonged debt crisis in the property market. Amid a persistent steel surplus and weakening prices, China has been considering reducing steel production, with volumes already down by 2.8% y-o-y in January-August 2025.

This steel market downtrend and declining production volumes have also weighed on the country’s demand for iron ore, with imports of the key feedstock down by 1.6% y-o-y in January-August 2025.

Notably, although the total volumes are down y-o-y, in recent months, iron ore imports have remained elevated, suggesting a divergence from steel production trends. Mills may be stocking up on iron ore, in anticipation of a rebound in steel consumption or to take advantage of attractive pricing.

As such, falling iron ore and pellet exports from India may be more due to internal factors rather than subdued steel market sentiment in China.

Outlook

The downtrend in export volumes is expected to continue. October will likely see an m-o-m fall due to the Golden Week holidays in China, which curbed trading activity during the first week. Additionally, the festive season in India may keep exporters’ attention away from the market for a while.

Moreover, it is uncertain whether the uptrend in global pricing will sustain amid an expected increase in supply, a typical occurrence during this period of the year. The rumoured dispute between the China Mineral Resources Group (CMRG) and BHP over pricing indicates that the country is keen to keep feedstock prices under check, probably to protect mill margins. This may further keep Indian exporters away from the market.

The primary determinant, however, will be the government’s decision on whether to impose duties on exports of low-grade iron ore. The committee is set to meet next week, and further clarity regarding the government’s decision may emerge in the subsequent days.

Leave a Reply