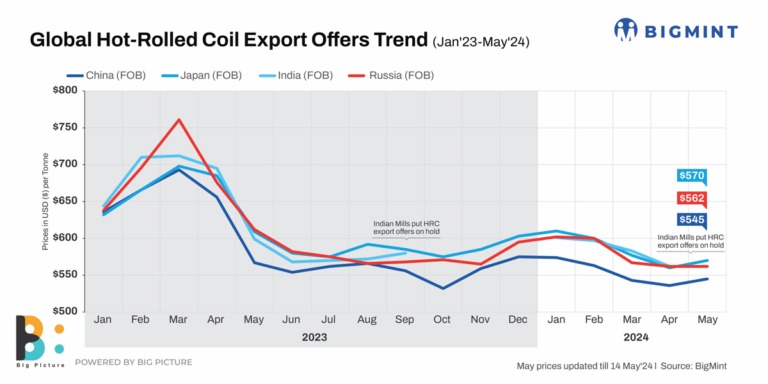

Indian hot-rolled coil (HRC) export offers to Southeast Asia and the Middle East (ME) continued to remain silent. Weak global market sentiment and competitive Chinese prices are keeping export activity muted for another week. While the ME market has seen participants return after Eid festivities, trading in the region remained subdued. Adding to the uncertainty, market players are anxiously awaiting the release of European Union’s (EU) fresh HRC import quotas for July 2024, which could significantly impact future export opportunities.

Market updates:

1. ME imported HRC offers fall w-o-w: Imported HRC offers to ME dropped post Eid-al-Adha festival holidays due to low trade activities, as buyers adopted wait-and-see approach. Chinese HRC export offers to the ME (grades S235 and S275) have decreased by $5/t w-o-w compared to the previous week, with offers ranging between $555-560/t CFR UAE. This is down from $560-$565/t a week ago. Additionally, Chinese mills have booked shipments of around 3,000-4,000 t at similar price levels with a tube maker. Notably, there haven’t been any offers from Japanese participants in the market.

2. Vietnam’s import offers decrease w-o-w: Imported offers of China-origin HRC (SAE1006) into Vietnam dropped by $5/t w-o-w to $540-545/t CFR HCMC against $545-550/t CFR HCMC a week ago, sources informed BigMint. A deal of around 40,000 t was heard concluded at similar price level for July, 2024 shipment. Furthermore, Vietnamese market participants are cautious amid drop in China’s HRC prices. Shanghai Futures Exchange (SHFE) HRC futures also saw a decline of RMB 72/t ($10/t) compared to the last week, settling at RMB 3,730/t ($514/t) against RMB 3,802/t ($524/t) a week ago.

3. Indian mills continue to hold HRC offers to EU: Indian steel mills continued to hold their HRC export offers (S275, 3mm) to the EU this week, market participants are awaiting fresh HRC import quotas. In the EU market, HRC market faces a supply-demand imbalance. Prices are flat despite slow demand, and mills may extend summer shutdowns to manage supply. Buyers are resisting any price hikes due to the weak offtake from crucial steel-using sectors like construction and automotive.

Outlook

Weak global demand and competitive Chinese pricing continue to dampen export activity. While the market participants in the ME have returned after Eid holiday, overall trading remained subdued. The release of the EU’s fresh import quotas for July will be a significant event, potentially influencing future export opportunities depending on the allocated volumes. Until then, Indian exporters might face challenges in reviving their export momentum.

Leave a Reply