- EU safeguard uncertainty keeps HRC import sentiment subdued

- Middle East trade resumes, but buyers remain cautious

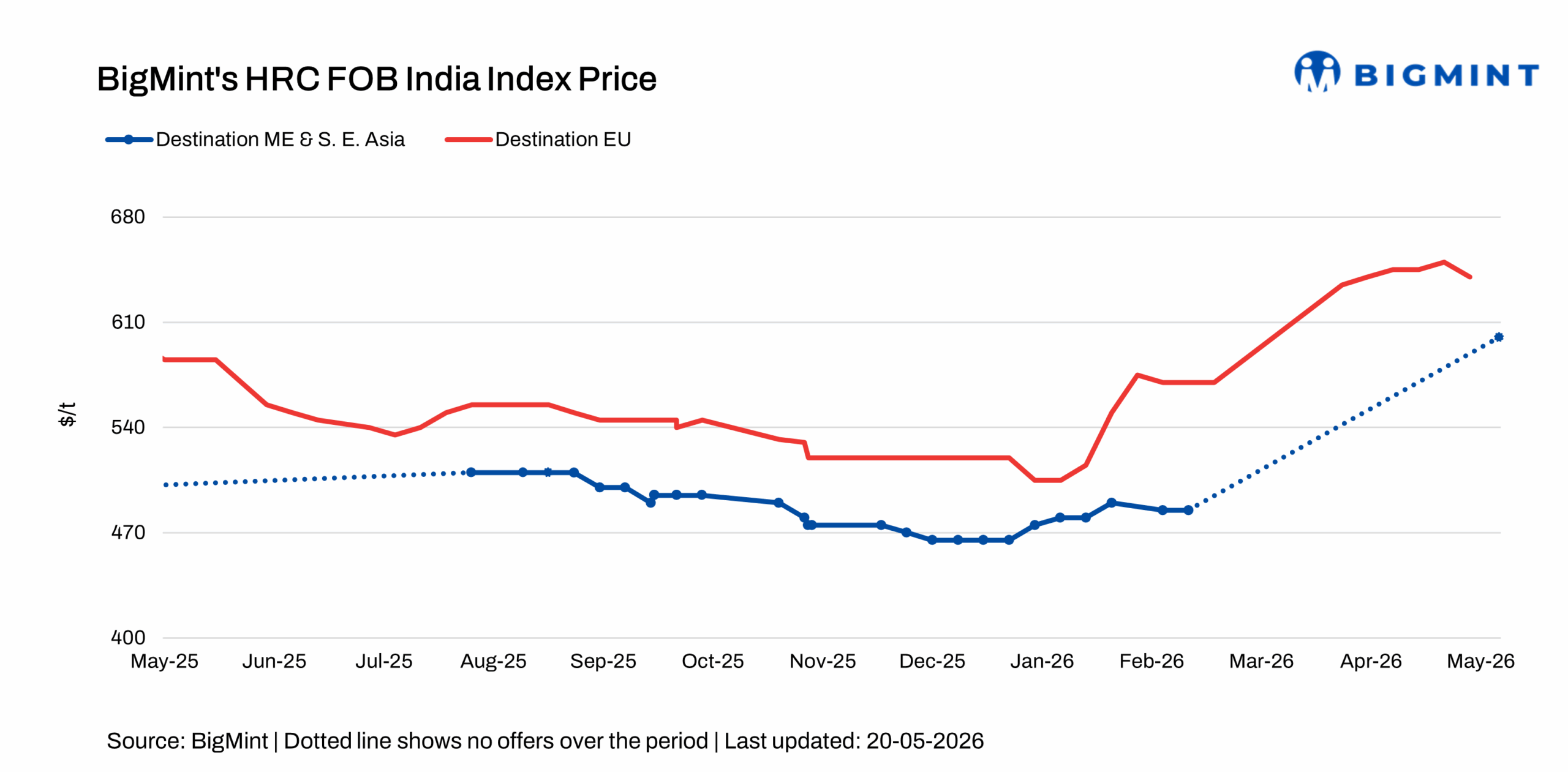

Indian HRC export markets showed a mixed regional trend in the week ended 20 May, with offers to the EU remaining absent w-o-w amid continued regulatory uncertainty and tighter safeguard expectations. At the same time, export activity to the Middle East has resumed after a prolonged period of subdued trading, marking a gradual revival in regional trade interest. Meanwhile, buying interest in Vietnam remained relatively steady, supporting overall export sentiment.

HRC export offers to the Middle East: Indian HRC export offers to the Middle East resumed this week after months of constrained market activity, with offers heard at around $550-560/t FOB. Freight to Fujairah port was estimated at approximately $45-50/t. Consequently, the Indian HRC export index to the Middle East and Southeast Asia increased by around $65/t to $550/t FOB, compared with approximately $485/t prior to the onset of geopolitical tensions in the region.

In addition, a booking for around 50,000 t was reportedly concluded at similar levels for June 2026 shipments, indicating a gradual revival in trading activity in the region.

Chinese HRC export offers to the region remained largely stable w-o-w at around $580-590/t CFR Jeddah, with only a limited number of mills currently active in the market.

Market participants noted that, “seaborne shipments, both inbound and outbound, continue to face severe restrictions, while freight costs have risen sharply in recent weeks. Although domestic steel demand across the GCC region has remained relatively steady, export activity has weakened notably due to logistical disruptions, elevated shipping risks, and limited cargo movement. As a result, market sentiment remains cautious. Many domestic producers are facing difficulties in exporting finished products, and the regional market is increasingly relying on domestic GCC demand for support.”

Another regional source stated that, “with Eid holidays approaching next week, trading activity is expected to remain quiet and largely subdued across the region. Any easing of geopolitical tensions around the Strait of Hormuz could bring some positive momentum to the market.”

HRC offers to Vietnam: Indian HRC export offers to Vietnam stood at around $580-585/t CFR, with a booking of around 30,000 t heard concluded at similar levels for June 2026 shipments. Regional demand for imported material remains relatively resilient, providing continued support to trade activity. Vietnam has emerged as the most active export destination for Indian HRC in recent weeks, largely driven by subdued domestic demand in India, while other export markets remain comparatively less viable.

Indian HRC export offers to the EU: Indian HRC export offers to the EU remained absent w o w, with no firm offers reported, as buyers continued to adopt a cautious stance amid policy-related uncertainty.

Overall import activity across the region remained subdued ahead of the revised EU safeguard measures scheduled to come into effect from 1 July 2026.

Under the revised regime, the annual tariff-rate quota (TRQ) is expected to stand at around 18.3 million tonnes (mnt), while imports exceeding the quota will attract a steeper 50% duty, compared with the earlier 25%. This has raised concerns over region-wise quota availability and potential additional duty liabilities, discouraging buyers from committing to fresh overseas cargoes.

At the same time, tightening regulatory requirements are adding further pressure on trade flows. The implementation of the Carbon Border Adjustment Mechanism (CBAM), along with proposed “melt and pour” norms, is increasing compliance complexities and cost obligations for importers, further weighing on procurement decisions.

Outlook

Indian HRC export activity is expected to show mixed regional trends w-o-w, with activity in the EU remaining subdued ahead of the revised safeguard regime and tighter CBAM-related compliance requirements. These factors continue to discourage fresh buying amid higher duty risks and quota uncertainty.

The Middle East market is expected to witness a gradual but uneven recovery in trade activity following the recent resumption of Indian offers. However, elevated freight costs, logistical constraints, and ongoing geopolitical tensions around the Strait of Hormuz are likely to keep sentiment cautious until the route becomes fully accessible. In contrast, the Vietnamese market is expected to remain relatively stable, supported by consistent buying interest and steady booking activity across the region.

Leave a Reply