- EU demand muted amid quota-related uncertainty

- Middle East activity subdued on Eid-al-Adha holidays

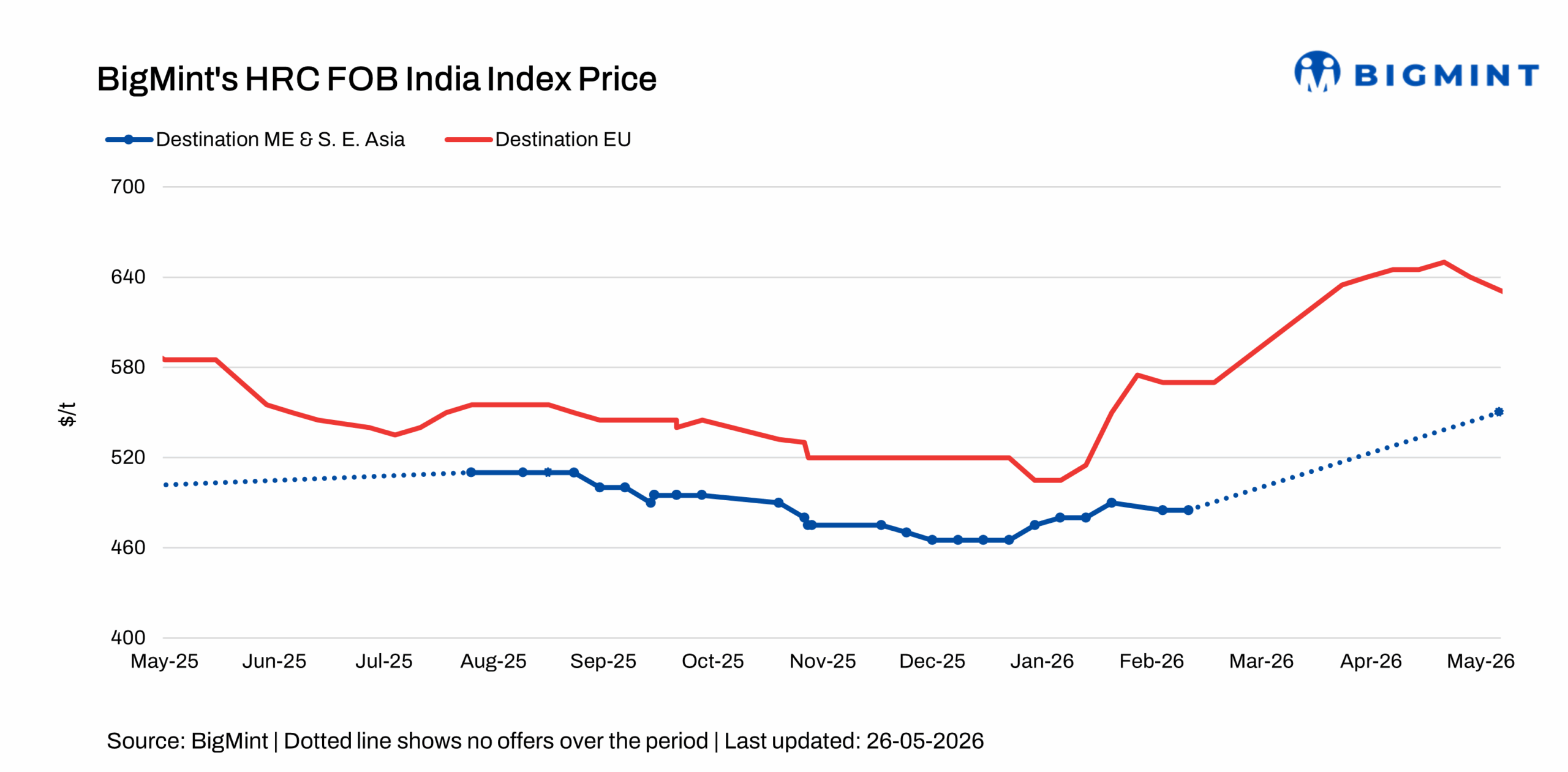

Indian HRC export activity remained subdued in the week ended 26 May, with shipments to Europe and the Middle East constrained by regulatory uncertainty, logistical disruptions and weak buying sentiment.

In the EU, although offers declined w-o-w, no fresh bookings were reported as buyers remained hesitant amid uncertainty surrounding country-wise quota allocations under the upcoming safeguard revisions, along with concerns over CBAM-related compliance costs.

In the Middle East, offers remained stable w-o-w; however, demand stayed subdued due to Eid al-Adha holidays, while logistical disruptions and elevated freight costs continued to weigh on trade activity, resulting in no fresh bookings.

Indian HRC export offers to the EU: Indian HRC export index to the EU declined by $15/t w-o-w to around $625/t FOB, compared with $640/t in the previous week. However, no fresh bookings were reported during the assessment period, as buyers continued to adopt a cautious stance amid regulatory and trade-related uncertainties.

The slowdown in import activity is largely driven by lack of clarity surrounding the EU’s revised safeguard regime, scheduled to take effect from 1 July 2026. Market participants are awaiting clarity on country-wise quota allocations before committing to fresh overseas purchases. Under the proposed structure, the annual tariff-rate quota (TRQ) is expected at around 18.3 million tonnes (mnt), while imports exceeding the quota may attract a higher 50% duty, up from the earlier 25%.

The proposed increase in out-of-quota tariffs has significantly raised risk exposure for importers. Buyers remain reluctant to book long-lead cargoes without clarity on quota availability and potential duty implications upon arrival, resulting in a broad wait-and-watch approach across the market.

In addition, uncertainty surrounding the EU’s Carbon Border Adjustment Mechanism (CBAM) continues to weigh on sentiment, as importers assess cost implications, reporting requirements, and compliance burdens. Proposed “melt and pour” requirements are also adding complexity to sourcing decisions for imported steel.

As a result, buyers are increasingly opting for domestic material over imports. The combined impact of safeguard-related uncertainty, potential tariff escalation, and evolving carbon regulations has dampened import appetite, keeping the EU imported HRC market muted.

HRC export offers to the Middle East: Indian HRC export index to the Middle East and South East Asia rose by $5/t w-o-w to around $555/t FOB, compared with $550/t in the previous week, with freight to Fujairah port estimated at approximately $45-50/t. Similarly, Chinese HRC export offers to the region also remained unchanged w-o-w at around $580-590/t CFR Jeddah, with only a limited number of mills currently active in the market.

A Middle East-based source noted that, “seaborne shipments, both inbound and outbound, continue to face logistical constraints, alongside a sharp rise in freight costs. Export activity has weakened notably due to ongoing shipping disruptions, elevated freight risks, and restricted cargo movement. As a result, overall market sentiment remains cautious, with market participants attempting to gradually resume activity.”

The source further added that, “domestic market conditions remains weak, with trading activity expected to stay subdued throughout the week due to the Eid-al-Adha holiday period.”

Outlook

Indian HRC export activity is expected to remain weak in the coming week amid subdued sentiment across key export destinations. In the EU, buying interest is likely to stay muted as market participants await clarity on the revised safeguard regime and country-wise quota allocations ahead of its 1 July 2026 implementation.

In the Middle East, trading activity is expected to remain muted over the week due to the Eid-al-Adha holidays, with logistical constraints and elevated freight costs continuing to weigh on seaborne trade flows. Overall, export sentiment is likely to remain cautious across regions, with any meaningful recovery dependent on regulatory clarity in the EU and normalisation of logistics and freight conditions in the Middle East.

Leave a Reply