- Stainless flat steel prices drop w-o-w

- Chinese ferro chrome prices steady

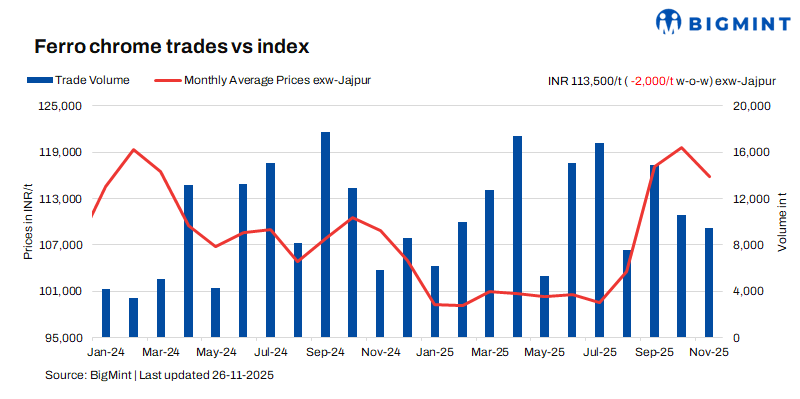

Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices witnessed a drop of INR 2,000/t ($22/t) as compared to the last assessment on 19 November 2025. Prices dropped as there was resistance from buyers to accept higher offers which limited market activity last week.

High-carbon ferro chrome (HC 60%, Si: 4%) prices in India were INR 113,500/t ($1,271/t) exw-Jajpur, as per BigMint’s assessment on 26 November. Around 1,000 t of deals were concluded last within a price bracket of INR 112,000-115,700/t ($1,254-1,296/t) exw.

A sharp drop was seen in low-silicon high-carbon ferro chrome prices as well, which edged down by INR 4,300/t ($48/t) w-o-w to INR 117,000/t ($1,310/t) exw-Jajpur. Low-carbon ferro chrome (C:0.1%) prices edged down slightly by INR 500/t ($6/t) w-o-w to INR 209,200/t ($2,343/t) exw-Durgapur. Around 250 t of deals were reported at INR 209,000/t ($2,341/t) exw.

Market recap (20-26 November)

Muted demand and lower bids: Ferro chrome prices slipped last week as market sentiment weakened following lower bids in this month’s chrome ore auction of OMC, where expectations of a price drop had already begun to build. The situation intensified after the OMC ferro chrome auction on 24 November fetched no bids, as sources informed, highlighting strong buyer resistance.

At the same time, demand from the stainless steel sector remained subdued, prompting buyers to place lower bids around INR 109,000-110,000/t ($1,221-1,232/t) exw, well below seller offers of INR 114,000-115,000/t ($1,277-1,288/t) exw. This wide bid-offer gap kept trading activity muted throughout the week, and with limited deal closures, ferro chrome prices eventually softened in response to the persistent market mismatch.

Persistent soft demand in stainless steel market: Stainless steel prices for 304 grade HRC inched down by INR 2,000/t ($22/t) w-o-w to INR 180,000/t ($2,016/t) exw-Mumbai. Prices softened on weak demand and high stockpiles across the value chain. Leading mills reportedly reduced offers and provided discounts to stimulate bookings. Import activity remained firm following the QCO extension till 31 March 2026, with Vietnam-origin 2-mm CRC at $1,950/t (wide) and $1,850/t (narrow) CFR India, adding competitive pressure.

Several producers also shifted from 304 to 316-grade production, supported by easing molybdenum prices and improved cost dynamics. Subdued domestic and export demand, muted trading, and import competition suggest continued price pressure in the near term.

Chinese prices remain steady: Ferro chrome (HC60%) prices in China were unchanged w-o-w at RMB 8,300/t ($1,172/t) exw-Inner Mongolia. Stability in prices was supported by steady stainless steel demand and firm raw material costs, though weak micro-carbon demand capped any major upside.

Chrome ore remained the key raw material driver, with limited supply growth due to South African production cuts and Turkiye’s export policy changes. Looking ahead, prices are expected to remain range-bound, with supply risks and policy uncertainties influencing short-term market direction.

Outlook

Considering existing market conditions and demand, ferro chrome prices are likely to fall further in the days ahead.

Leave a Reply