- Ferro chrome exports plunge over 30% y-o-y in FY’25

- Domestic benchmark ferro chrome prices drop 6% y-o-y

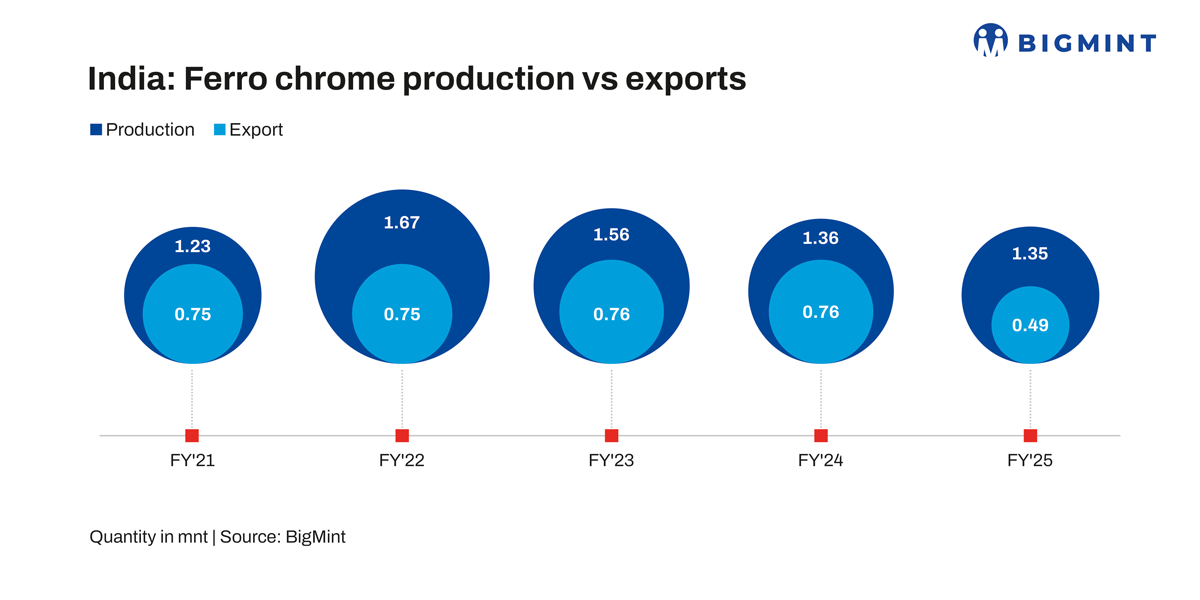

India’s ferro chrome production registered a slight decline of 1% in FY’25, reaching 1.35 mnt compared to 1.36 mnt in FY’24. The industry experienced a mixed performance during the fiscal, shaped by diverging trends in raw material prices, export dynamics, and stainless steel demand.

Key highlights

Diverging price trends: Ferro chrome vs chrome ore

BigMint’s benchmark high-carbon (HC 60%) ferro chrome prices fell by 6% y-o-y in FY’25 to INR 105,600/t ($1,235/t) exw-Jajpur from INR 113,100/t ($1,323/t) in FY’24.

In contrast, Odisha Mining Corporation’s (OMC) chrome ore prices increased as follows:

- 52–54% grade: up INR 1,000/t ($12/t) to INR 28,700/t ($335/t)

- 48–50% grade: up INR 500/t ($6/t) to INR 24,500/t ($286/t)

This rise in chrome ore costs pushed up production expenses. However, subdued demand and declining ferro chrome prices prompted some producers to divert furnaces to other alloys, including manganese alloys and low-silicon/low-carbon ferro chrome towards the fiscal end.

Stable chrome ore production

India’s chrome ore output remained steady at 3.14 mnt in FY’25, showing a marginal 1% increase from FY’24. OMC remained the largest supplier, contributing 1.35 mnt during the year.

Sharp drop in exports

Ferro chrome exports declined significantly by 36%, falling to 0.49 mnt in FY’25 from 0.76 mnt in FY’24. The drop was largely driven by reduced buying from China, India’s key export market, which increasingly relied on domestic supply.

Additionally, the continued decline in tender prices from Chinese stainless steel giants like Tsingshan (since July’24) and TISCO (Taiyuan Iron and Steel Corporation) made Indian export offers less competitive. High inventories, weak stainless steel demand, and elevated spot prices in China continued to put downward pressure on tender prices.

Stainless steel market

India’s stainless steel production grew by 14% y-o-y in FY’25 to 3.85 mnt from 3.38 mnt in FY’24. The increase was supported by higher arrivals of semi-finished products like SS 300 series slabs, billets, and nickel pig iron (NPI), which reduced reliance on scrap and ferro chrome.

However, increased imports of finished stainless steel products also impacted domestic raw material consumption, leading to lower capacity utilisation for ferro chrome producers.

Despite the uptick in stainless steel production, overall market demand remained weak, continuing to weigh on the ferro chrome market.

Outlook

Going forward, some ferro chrome producers are expected to maintain their focus on alternative alloys such as manganese alloys, given ongoing market challenges. Weak demand from the stainless steel sector is likely to keep ferro chrome prices under pressure in the near term.

However, with stainless steel production expected to maintain its growth trajectory, domestic ferro chrome production is likely to remain relatively stable in the coming fiscal.

Leave a Reply