Indian cold rolled coil (CRC) export offers to Europe remained unchanged for the week at $725-730/tonne (t) CFR Antwerp ($675-680/t FOB east-coast India) due to soft summer demand and overflowing inventories. However, a deal of around 5,000 t was concluded at $800/t CFR Antwerp for late-August shipments.

The European market for CRCs experienced a seasonal slowdown, with prices under pressure due to sluggish demand. Weak consumption from key industries, particularly the automotive sector, contributed to low trading activity. European steel mills were reluctant to offer competitive prices for CRCs owing to high production costs and intense competition from imported material.

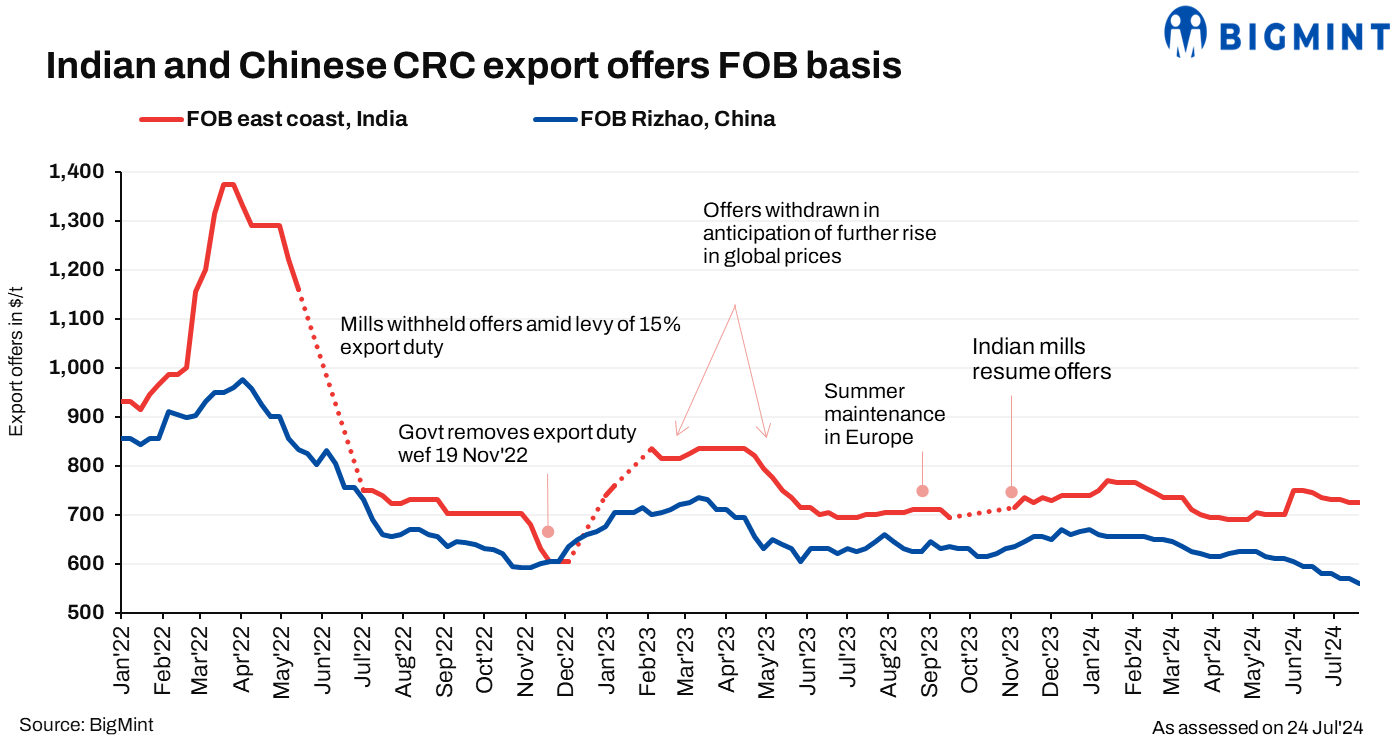

China’s CRC export offers went down by $10/t to $560/t FOB against $570/t FOB last week.

Chinese HRC offers on the Shanghai Futures Exchange (SHFE) dipped by RMB 32/t ($4/t) d-o-d to RMB 3,580/t ($492/t) as compared to RMB 3,612/t ($496/t) a day ago. Moreover, on a w-o-w basis, the same sharply fell by RMB 121/t ($17/t) against RMB 3,701/t ($509/t) in the previous week.

European HRC prices remained largely stagnant due to weak summer demand and ample supply. Stockholders are well-stocked, limiting immediate purchase needs. The market is sluggish, with concerns about real demand dampening expectations of a post-holiday price recovery. Insufficient end-user consumption has reduced buyer urgency to replenish inventories.

Outlook

The global CRC market is currently characterised by oversupply and weak demand, particularly in Europe. While a seasonal recovery is anticipated towards the end of the summer, the overall market sentiment remains cautious. However, sustained price recovery will depend on a robust revival in end-user industries and a reduction in global steel production.

Leave a Reply