- Netherlands emerges as India’s top supplier

- Saves scrap remains dominant imported grade

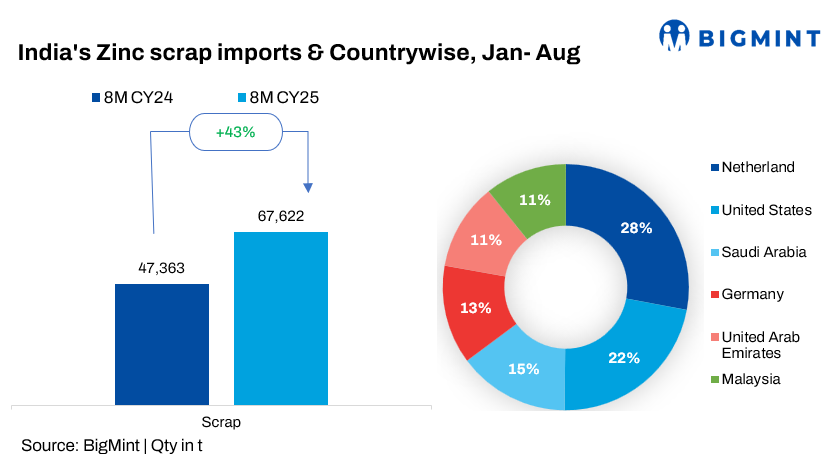

India’s zinc scrap imports climbed up sharply by 43% y-o-y in the first eight months of 2025 (January-August 2025) to 67,622 tonnes (t) compared with 47,365 t in the same period of 2024. This year’s inflows already account for nearly 90% of the full-year 2024 total of 75,180 t, underscoring stronger reliance on secondary zinc feed. July was the peak month at 9,810 t, while February was the softest at 5,761 t, reflecting a slow Q1 start followed by mid-year acceleration. August arrivals of 8,978 t kept the year-to-date monthly average near 8,450 t.

Grade-wise zinc scrap imports

India’s zinc scrap imports in the January-August 2025 (8MCY’25) showed a significant uptrend across most grades.

For the second straight year, Saves (old zinc die-cast scrap) and Score (zinc sheet scrap) led imports, with Saves totalling 44,276 t and Score at nearly 16,000 t for the period. Notably, monthly Saves arrivals remained above 5,000 t and peaked at 6,009 t in March. Scroll and Screen grades, though smaller, cumulatively contributed over 5,500 t, underscoring sustained demand for diverse inputs by alloy and galvanising manufacturers.

Top supplying nations

The Netherlands emerged as India’s top supplier in Jan-Aug 2025 with 9,917 t, overtaking the US (7,874 t). Other key origins included Saudi Arabia (5,203 t), Germany (4,610 t), and the UAE (4,042 t). Malaysia, Thailand, Belgium, Italy, and Nigeria rounded out the top ten. Together, the Netherlands and the US accounted for over a quarter of arrivals, while Europe and the Gulf also collectively provided a significant share, highlighting diversified sourcing.

Scrap vs ingot context

Semi-finished ingot imports reached 171,548 t in January-August 2025, up 38% y-o-y from 123,996 t last year. With scrap at 67,622 t, the scrap-to-ingot ratio stood near 39%, confirming that secondary feed complemented, rather than replaced, primary zinc imports during the period assessed.

Physical demand, policy impact

The data shows that end-user demand peaked in July-August 2025, aligned with surging orders from galvanising and alloy production units. Inventory restocking remained steady despite primary metal price volatility, supporting consistent procurement.

Policy support also played a key role. The 2025 Union Budget’s nil-duty policy on non-ferrous scrap imports reduced cost barriers, encouraging increased purchases, especially in the Saves and Score categories. Ongoing capacity expansion in India’s steel and alloy sectors further reinforced reliance on imported zinc feedstock.

Outlook

India’s zinc scrap imports are expected to cross 100,000 t by end-2025, supported by robust industrial demand and policy tailwinds. Buyers are likely to continue diversifying sourcing across the UK, EU, Middle East, and Asia to hedge against potential shortfalls in US-origin supplies.

Leave a Reply